Introduction

Nearly 35% of Americans age 65 and older are unmarried — widowed, divorced, or never married — per the 2023 Profile of Older Americans by the HHS Administration for Community Living. That's tens of millions of people navigating retirement without the financial backstop a spouse provides.

Every market downturn, health emergency, or major expense lands on one income. The U.S. tax code applies narrower brackets to single filers. And if illness or cognitive decline strikes, there's no default partner to step in.

This guide covers savings benchmarks, Social Security strategy, healthcare and long-term care planning, estate and legal protections, and tax considerations — built specifically for the single retiree's situation, not the standard two-income household model.

Key Takeaways

- Single retirees need to save more — T. Rowe Price benchmarks single filers at 10.5x salary at 65, versus 7.5x for married households

- Delaying Social Security to age 70 increases monthly benefits by 8% per year after full retirement age

- Estate planning documents (wills, powers of attorney, healthcare directives) are non-negotiable — there is no default legal surrogate when you're single

- Long-term care insurance is a priority; assisted living costs $74,400 annually at the 2025 national median

- Work with a fee-based fiduciary advisor — they're legally required to act in your interest, not earn commissions on product sales

The Unique Financial Challenges Single Retirees Face

The Single Income Problem

When a married retiree faces a $30,000 roof replacement or a year with poor market returns, a spouse's Social Security check or pension keeps the household running. Single retirees have no such buffer. Every financial shock absorbs entirely from one portfolio.

The real danger is sequence-of-returns risk. A large, unexpected expense in early retirement can permanently impair a portfolio that never gets the chance to recover.

The Tax Code Penalty

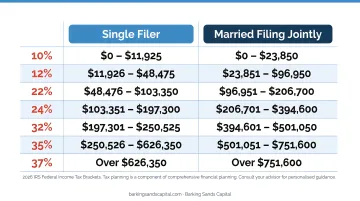

The U.S. tax system is structurally less favorable for single filers. Based on 2026 IRS inflation adjustments, the gap is significant:

| Tax Item | Single Filer | Married Filing Jointly |

|---|---|---|

| Standard deduction | $16,100 | $32,200 |

| 22% bracket threshold | $50,400 | $100,800 |

| 24% bracket threshold | $105,700 | $211,400 |

| Home sale gain exclusion | $250,000 | $500,000 |

Two people earning the same combined income often pay meaningfully different effective tax rates based solely on filing status.

Longevity Risk With a Solo Dimension

A woman who reaches age 65 can expect to live an additional 20.8 years, according to CDC/NCHS Data Brief No. 548 published in January 2026. That's a retirement potentially stretching into the mid-80s — or beyond for many.

For single women in particular, the numbers stack: 29% of all older women are widows (roughly 9 million people), and 33% of older women live alone. A portfolio needs to last two decades or more with no secondary income source in reserve.

Cost-of-Living Realities

Couples split housing costs, utilities, insurance premiums, and transportation. Single retirees pay all of it alone. T. Rowe Price's 2026 benchmarks capture this directly: a single person earning $100,000 needs to save 10.5x their salary by age 65 — compared to just 7.5x for a married sole earner at the same income level. That 3x gap reflects the real cost of living without economies of scale.

The Incapacity Gap

If a married retiree develops dementia or suffers a serious medical event, their spouse can pay bills, manage accounts, and make healthcare decisions. A single retiree with no legal documents in place has none of that. Courts may need to appoint a guardian — a process that is slow, expensive, and strips control from the retiree. Without those documents, there is no one legally authorized to step in.

Building Your Retirement Income Strategy

Knowing Your Savings Target

The commonly cited rule of thumb — save 10x your final salary — understates what single retirees actually need. Most retirement planning frameworks put the target at 10.5x to 13x final salary, depending on income level — higher than the standard benchmark because there's no spousal Social Security, no second pension, and no partner's RMDs to supplement withdrawals.

A useful quick estimate for income planning: the $1,000-a-month rule. For every $1,000 of monthly income desired beyond Social Security, you generally need approximately $240,000 saved:

- Assumed withdrawal rate: 5%

- $240,000 × 5% = $12,000/year = $1,000/month

This works as a ballpark. A single retiree targeting $3,000/month beyond Social Security would need roughly $720,000 saved. But this rule doesn't account for taxes, inflation, or healthcare costs — a personalized analysis with a financial planner will always produce a more accurate picture.

Maximizing Social Security as a Single Retiree

For single retirees, the Social Security timing decision is more consequential than for couples, because there's no spousal benefit to coordinate with or fall back on.

According to the Social Security Administration, delayed retirement credits increase monthly benefits by 8% for each year of delay past full retirement age for those born in 1943 or later. Delaying from 67 to 70 means roughly a 24% higher permanent monthly benefit — for life.

Two often-overlooked eligibility categories:

- Widows and widowers can receive up to 100% of a deceased spouse's benefit at survivor full retirement age, with reduced benefits available as early as age 60

- Divorced individuals married for 10+ years may claim up to 50% of an ex-spouse's primary insurance amount — even if the ex has remarried, and without affecting the ex's own benefit

These provisions are worth reviewing with an advisor before claiming, since the decision is permanent. That permanence makes the cash cushion you carry into retirement equally important — because once benefits are locked in, your emergency fund becomes your first line of defense against forced withdrawals.

Building the Right Emergency Fund and Withdrawal Plan

General guidance suggests 3 to 6 months of expenses in emergency savings. For retirees, AARP recommends 18 to 24 months, and specifically notes that single women should consider a larger fund due to longer life expectancy and higher potential emergency costs.

The logic is sound. Without a partner's income as a secondary cushion, an unplanned expense — a $15,000 HVAC replacement, a medical bill, a car — shouldn't force a retiree to sell investments at a market low. Keep this fund in a liquid, accessible account separate from investment accounts.

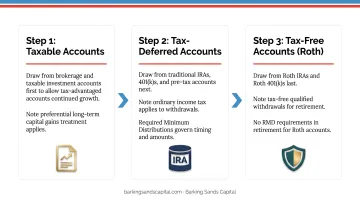

For withdrawal sequencing, the general framework:

- Taxable accounts first — capital gains rates are typically lower than ordinary income rates

- Tax-deferred accounts next — traditional IRA and 401(k) withdrawals are taxed as ordinary income

- Roth accounts last — tax-free growth preserved as long as possible

For single retirees, this sequencing matters more than it does for couples, because higher single-filer bracket thresholds mean even modest withdrawals from tax-deferred accounts can push income into a higher bracket faster.

Healthcare, Insurance, and Long-Term Care Planning

Medicare: Getting It Right the First Time

Medicare enrollment at 65 is consequential, and single retirees have no spouse's employer coverage to fall back on if they make a costly mistake.

Key penalties for missing enrollment windows:

- Part B: 10% premium increase for each year delayed, permanently

- Part D: 1% per month without creditable drug coverage

- Medigap: A one-time 6-month open enrollment window begins when you're 65 and enrolled in Part B — outside that window, insurers can deny coverage or charge more based on health history

Miss these windows and there's no reset — just years of higher premiums and larger out-of-pocket exposure.

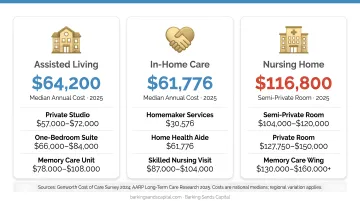

Long-Term Care: A Priority, Not an Option

Someone turning 65 has nearly a 70% chance of needing long-term care services at some point. For single retirees, this creates direct financial exposure. There's no partner to provide informal care at home, which couples often do for years before professional care becomes necessary.

The 2025 national median costs break down as follows:

- Assisted living: $6,200/month ($74,400 annually)

- In-home non-medical care: $35/hour ($80,080 annually at 44 hours/week)

- Semi-private nursing home room: $114,975 annually

Women average 3.7 years of care needs; about 20% of 65-year-olds will need care for more than 5 years. For a single person, that's a potential six-figure exposure with no informal caregiver option.

The coverage rules, cost structures, and enrollment timing across Medicare and long-term care products vary enough that the wrong choice can mean thousands in avoidable costs. Curtis Hewitt, an advisor at Barking Sands Capital who specializes in Medicare Planning and Long-Term Care, works with clients in Michigan, Minnesota, and beyond to evaluate these options — without the pressure of commission-based product sales.

Smart Investment Strategies for Solo Retirees

The Rule of 72 and Setting Realistic Expectations

A simple but useful tool: divide 72 by your expected annual return to estimate how many years it takes for money to double. At 6% annual growth, $300,000 doubles to $600,000 in roughly 12 years. At 4%, it takes 18 years.

Why this matters for single retirees: understanding growth timelines helps calibrate how much risk is needed to sustain a portfolio over a 20+ year retirement. Too conservative and inflation erodes purchasing power. Too aggressive early in retirement and a market downturn can permanently impair the portfolio.

Asset Allocation Without a Safety Net

Couples sometimes split roles — one partner takes more growth-oriented risk while the other holds more stable assets. Single retirees can't do that. The entire portfolio must balance two competing needs:

- Growth: enough equity exposure to outpace inflation over a long retirement

- Stability: enough income-generating assets to fund near-term expenses without forced selling

The general principle: maintain meaningful equity exposure through retirement rather than shifting entirely to bonds, while gradually increasing income-generating allocations as the years advance. Age, spending rate, and risk tolerance all shape the right mix — and for solo retirees, the absence of a second income stream makes getting that balance right more consequential than it is for couples.

Diversification Across Account Types

Single retirees face concentrated risk on multiple fronts. Diversification should cover:

- Account types: taxable, tax-deferred (IRA/401k), and Roth accounts — each with different tax treatment at withdrawal

- Asset classes: equities, fixed income, real estate investment trusts, cash equivalents

- Income sources: Social Security, portfolio withdrawals, potential annuity income

Holding everything in a traditional IRA concentrates all withdrawals in one tax bucket — and when required minimum distributions begin at age 73, that exposure compounds quickly. Building Roth assets alongside traditional accounts creates withdrawal flexibility that can reduce lifetime taxes in a concrete, plannable way.

Estate Planning and Legal Protections

For single retirees, estate planning isn't just about what happens when you die — it's about what happens if you become incapacitated.

The Core Documents

Without a spouse as default heir and legal surrogate, these documents are what direct outcomes:

- Will or revocable living trust: directs where assets go; a trust avoids probate and can simplify administration

- Beneficiary designations: on all retirement accounts, life insurance, and investment accounts — these supersede the will entirely, so outdated designations can redirect assets contrary to your wishes

- Financial durable power of attorney: authorizes a trusted person to manage financial affairs if you become incapacitated; without this, a court appoints a guardian

- Healthcare power of attorney and advance directive: designates who makes medical decisions and communicates your wishes; add HIPAA authorization so the agent can actually access your medical records

The document alone isn't enough. The person you designate needs a direct conversation about your intentions — specific wishes, financial priorities, and what matters most to you.

Estate planning documents also need to align with your investment accounts, tax strategy, and retirement distribution plan. Beneficiary designations must reflect your current intentions and work consistently with your overall estate plan. Barking Sands Capital's InteProcess™ coordinates estate planning alongside investment and retirement planning, so these protections fit into a single, coherent financial plan — not a stack of documents managed in isolation.

Navigating Taxes as a Single Retiree

Social Security Taxation: A Steeper Curve for Singles

Single filers hit Social Security taxation thresholds at lower income levels than married couples. Per IRS Publication 915:

| Threshold | Single Filer | Married Filing Jointly |

|---|---|---|

| Up to 50% of SS taxable above | $25,000 combined income | $32,000 combined income |

| Up to 85% of SS taxable above | $34,000 combined income | $44,000 combined income |

A single retiree with $35,000 in combined income has up to 85% of their Social Security benefit subject to tax. A married couple needs $44,001 before reaching that same threshold. That $9,000 gap can represent a meaningful annual tax difference.

Roth Conversions Before RMDs

Required minimum distributions begin at age 73. The years between retirement and RMD onset are often the lowest-income years a retiree will experience — and for single retirees with compressed tax brackets, this window is worth using strategically.

Converting traditional IRA funds to Roth during lower-income years means paying tax now at a potentially lower rate to eliminate future taxable RMD income. Sizing each year's conversion carefully matters — go too far and you risk:

- Pushing income into a higher tax bracket

- Triggering IRMAA surcharges on Medicare premiums

- Reducing eligibility for other income-based benefits

This analysis is individual. The right conversion amount depends on your current bracket, projected RMDs, Social Security timing, and healthcare costs. A fee-based financial planner can model each scenario year by year, so the strategy stays calibrated as your income picture shifts.

Frequently Asked Questions

What is the $1,000-a-month rule for single retirees?

For every $1,000 of monthly income desired beyond Social Security, you generally need approximately $240,000 saved, assuming a 5% withdrawal rate. A single retiree wanting $3,000/month beyond Social Security needs roughly $720,000 — though a personalized plan should also account for taxes, inflation, and healthcare costs.

What is the Rule of 72 and how does it apply to retirement planning?

Divide 72 by your expected annual return to estimate how many years your money takes to double. At 6%, money doubles in roughly 12 years. Retirees use this to set realistic growth expectations and assess whether their asset allocation supports their income needs over a 20+ year horizon.

What is a good retirement savings amount for a single retiree?

T. Rowe Price's 2026 benchmarks suggest single retirees target 10.5x to 13x final salary by retirement — notably higher than the 7.5x benchmark for married households. With no spouse's income or Social Security to supplement withdrawals, single retirees carry the full income load from their portfolio.

How should a single retiree handle estate planning without a spouse?

Explicitly designate beneficiaries on every account, establish a will or trust, and assign both a financial power of attorney and a healthcare power of attorney. Without a spouse as default heir and legal surrogate, these documents are the only way to ensure your assets and medical decisions follow your wishes.

What insurance coverage is most important for single retirees?

Long-term care insurance is the top priority — there's no partner to provide informal care, and assisted living costs $74,400 annually at the national median. Follow that with a robust Medicare Supplement plan to control out-of-pocket healthcare costs, and disability insurance if you're still pre-retirement.

When should a single retiree start working with a financial advisor?

Ideally 5 to 10 years before retirement, when there's still time to optimize savings rate, tax positioning, and Social Security strategy. Any single retiree without a current plan should consult a fee-based fiduciary advisor now — Social Security timing, Medicare enrollment, and withdrawal sequencing are decisions you can't undo.