This isn't just a personal finance gap. It's a business continuity risk. According to Gallup, 74% of employer-business owners nearing retirement plan to sell or transfer ownership — yet most lack a funded succession plan to execute that transition.

Life insurance for business owners serves two distinct purposes: protecting the owner's family from lost income, and protecting the business itself from operational collapse, debt default, or forced dissolution. This guide covers both dimensions — the coverage types that apply, how to structure ownership correctly, what the 2024 Connelly ruling changed, and how to calculate how much coverage you actually need.

Key Takeaways

- Life insurance serves four distinct roles for business owners: continuity protection, ownership transitions, key person coverage, and family income replacement

- Most business owners need a combination of coverage types — not a single policy

- Policy ownership structure significantly affects tax treatment and estate outcomes

- The 2024 Connelly v. United States Supreme Court ruling changed how entity-owned buy-sell policies are treated for estate tax purposes

- Regular policy reviews tied to business milestones are essential — coverage needs change as the business grows

Why Every Business Owner Needs Life Insurance

Business Continuity and Debt Exposure

When a sole proprietor or central owner dies, the business doesn't automatically continue. Client relationships, operational knowledge, vendor agreements, and revenue streams can collapse quickly — particularly in service-based businesses where the owner is the product.

The debt exposure alone is significant. The SBA Office of Advocacy reports over $1.3 trillion in small-business loan balances as of 2023. Those obligations don't disappear when an owner dies. Creditors can pursue the business estate, and in many cases, personal guarantees mean they can pursue personal assets too.

Lenders are aware of this risk. Under SBA guidelines (SOP 50 10), when a business's viability depends on specific individuals, life insurance may be required as collateral — with the lender named as beneficiary to ensure the loan can be repaid. The requirement exists because lenders have a real financial stake in whether the business survives without its key person.

The Succession Planning Gap

Most business owners have no funded mechanism to transfer ownership if they die. Without life insurance providing cash for a buyout or business transition, partners face a forced sale at distressed prices, heirs inherit an entity they may not be able to run, and employees face uncertainty about whether the business continues.

The exposure touches every part of an owner's financial life:

- For most small business owners, the business is their primary income source — and family financial security depends on it continuing

- Outstanding business debt doesn't pause for grieving

- Without a funded buy-sell agreement, remaining partners may lack the cash to purchase the deceased owner's stake

- Replacing critical knowledge and client relationships takes time and money the business may not have

Types of Life Insurance for Business Owners

Business owners typically need to consider multiple coverage types. Some protect the business directly; others protect personal and family finances. The right combination depends on business structure, ownership arrangement, and planning objectives.

Key Person Life Insurance

Key person insurance is not a distinct regulated product — it's a business planning strategy using standard life or disability insurance. The business owns the policy on a critical owner or employee, and the business is the beneficiary.

When that person dies, the death benefit gives the company financial runway to:

- Cover lost revenue during the transition period

- Recruit and train a qualified replacement

- Stabilize operations and maintain client relationships

- Repay any debt the key person personally guaranteed

According to SHRM, employee replacement costs range from 50% to 200% of annual salary. For a high-revenue partner or founder, the disruption cost is considerably higher when you factor in lost sales and client attrition.

A commonly used starting benchmark: take the key person's salary plus their direct contribution to revenue, then multiply by at least five. Treat that figure as a minimum, not a target — coverage needs often run higher once client attrition risk is factored in.

One critical compliance note: Employer-owned life insurance must satisfy IRS Section 101(j) notice and consent requirements before the policy is issued. Employees must receive written notice of the intent to insure and provide written consent. Policies that don't meet these requirements lose most of the death benefit income-tax exclusion. Annual reporting on Form 8925 is also required.

Buy-Sell Agreement Life Insurance

A buy-sell agreement is a legally binding contract between co-owners specifying how ownership transfers if one owner dies, becomes disabled, or exits the business. Life insurance is the standard funding mechanism.

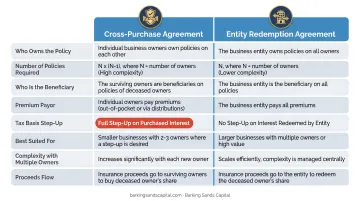

Two primary structures exist:

| Structure | How It Works | Key Consideration |

|---|---|---|

| Cross-purchase | Each owner holds a policy on the other; surviving owner uses proceeds to buy the deceased's interest | More complex with multiple owners; survivors may receive a stepped-up cost basis |

| Entity redemption | The business owns and is beneficiary of policies on each owner; the company redeems the deceased's shares | Simpler to administer, but now carries significant estate tax risk under Connelly |

The 2024 Connelly v. United States ruling matters here. On June 6, 2024, the Supreme Court held that a corporation's contractual obligation to redeem shares does not offset life insurance proceeds when valuing the company for federal estate tax purposes. In practice, entity-owned buy-sell insurance can increase the value of the deceased owner's estate, resulting in a larger estate tax bill than the business anticipated.

Any business with an entity-owned buy-sell arrangement should review that structure with legal and tax advisors immediately. Cross-purchase structures or trusteed alternatives may warrant consideration depending on the specific facts.

Individual Life Insurance

For sole proprietors and single-owner businesses (where personal and business finances are tightly intertwined), individual life insurance covers both dimensions at once. The death benefit can replace the owner's personal income for the family while also providing liquidity to cover business obligations during wind-down or transition.

This matters most for owners who have personally guaranteed business debts or whose household income depends entirely on business distributions. Common uses include:

- Replacing lost personal income for surviving family members

- Covering business rent, payroll, and vendor obligations during transition

- Repaying personally guaranteed loans

- Funding a structured wind-down if no successor is in place

Group Life Insurance

Business owners can offer group life insurance as an employee benefit, providing coverage to employees regardless of individual health status. The competitive advantage for smaller employers is real: BLS data from March 2025 shows only 42% of private-industry workers at establishments with fewer than 100 employees had access to life insurance, compared to 87% at companies with 500 or more.

Offering group coverage helps close that gap — and the tax treatment supports it. The tax structure makes it especially attractive for small employers:

- Employees pay no income tax on the first $50,000 of employer-paid group-term coverage (per IRS Publication 15-B and IRC Section 79)

- Employers can generally deduct premiums paid within that threshold as a business expense

- Coverage is guaranteed issue, meaning employees typically don't need to pass medical underwriting to qualify

Term vs. Permanent Life Insurance: What Business Owners Need to Know

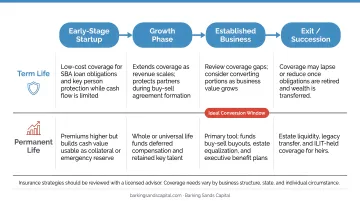

Choosing between term and permanent coverage comes down to one question: is the business risk you're protecting against temporary or ongoing? The answer shapes everything — from premium costs to how the policy fits into your broader financial plan.

Term life insurance provides coverage for a defined period — typically 10 to 30 years — at lower premiums than permanent coverage. It fits finite business risks well:

- Covering a specific SBA loan or business line of credit during repayment

- Funding a buy-sell agreement during the business's growth phase

- Key person protection while a successor is being groomed

- Early-stage businesses that need meaningful coverage while reinvesting revenue

Permanent life insurance (whole life and universal life) provides lifelong coverage with a cash value component that grows tax-deferred. For business owners, the applications extend beyond simple protection:

- Cash value can be borrowed against for business investments or operating needs

- Supports long-term succession and estate planning strategies

- Used in executive bonus arrangements to attract and retain key employees

- Better fit when coverage needs are permanent rather than time-limited

How these differences translate into real decisions depends on where your business stands today:

- Early-stage business with tight cash flow → Term, focused on specific debt obligations and income replacement

- Established business with succession planning goals → Permanent, for tax-advantaged cash accumulation and long-term buy-sell funding

- Complex ownership structure or estate planning needs → Often a combination, structured in coordination with legal and tax advisors

The ACLI notes that whole life insurance is commonly used in key person and buy-sell contexts for established businesses. That said, the right structure depends on your specific situation — age, health, business stage, and financial goals all factor in. A fee-based advisor can model both options side by side before you commit.

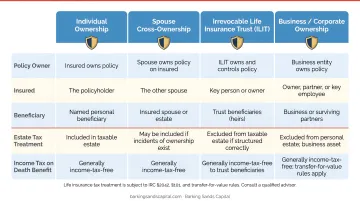

Tax Implications and Policy Ownership Considerations

Who owns a life insurance policy determines how the death benefit is taxed and how it affects the owner's estate — and getting it wrong can be costly.

General income tax treatment: Under IRC Section 101(a)(1), life insurance death benefits are generally excluded from the beneficiary's gross income. But several exceptions apply:

- Employer-owned policies must meet IRC Section 101(j) notice and consent requirements, or the income-tax exclusion is limited to premiums paid — not the full death benefit

- Entity-owned buy-sell policies post-Connelly can inflate the company's fair market value for estate tax purposes, increasing estate tax liability for the deceased owner's heirs

- Transfer-for-value rules can also convert a previously tax-free benefit into taxable income in certain circumstances

Premium deductibility: In most cases, life insurance premiums are not tax-deductible when the business or business owner is the beneficiary — this is governed by IRC Section 264. Exceptions include employer-paid group term life premiums within the Section 79 threshold and certain executive compensation arrangements.

How you own the policy shapes those tax outcomes directly. The four common structures each carry distinct tradeoffs:

- Individual ownership keeps things simple, but death proceeds may be pulled into the taxable estate if the insured retains any control over the policy

- Business entity ownership works cleanly for key person and buy-sell coverage, but post-Connelly it introduces estate-tax risk in redemption structures

- Irrevocable Life Insurance Trust (ILIT) removes proceeds from the taxable estate entirely — at the cost of surrendering direct policy control and requiring advance planning

- Cross-purchase arrangements keep proceeds out of corporate hands by having each owner hold policies directly on co-owners

Each of these structures has different estate, income, and entity-level tax consequences. Ownership and beneficiary decisions should be made alongside a qualified tax advisor and estate planning attorney — ideally as part of a coordinated financial plan rather than in isolation.

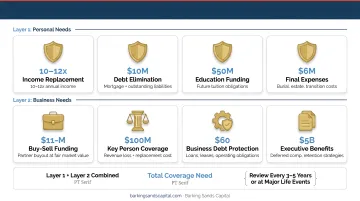

How to Calculate How Much Life Insurance Your Business Needs

There's no universal formula that works for every business owner. Coverage needs must be layered across two distinct categories: the business itself and the owner's personal finances.

Business Layer

Identify every cost the business would need to continue — or responsibly wind down — without the owner:

- Monthly payroll obligations

- Rent, leases, and fixed operating expenses

- Outstanding business loans and lines of credit

- Vendor contracts with cancellation penalties

- Cost to recruit, hire, and train a replacement (50%–200% of annual salary as a benchmark)

- Any personally guaranteed business debt

Personal and Family Layer

Calculate what the owner's family would need to maintain financial stability:

- Annual income replacement — commonly cited as 5 to 10 times annual salary, though business owners with significant business debt or dependents often need more

- Mortgage and consumer debt payoff

- Education funding for children

- Ongoing household expenses during transition

When to Revisit Your Coverage

A policy sized at business founding is almost certainly inadequate five years later. Business valuations grow, loans are added, and ownership structures change. Policy reviews should be triggered by:

- Taking on a new business loan

- Adding or losing a business partner

- Significant revenue growth or business acquisition

- Changes in personal net worth or family situation

This is where working with an advisor who sees the full financial picture matters. Barking Sands Capital's proprietary InteProcess™ integrates insurance, estate planning, tax, and retirement strategies into a single coordinated plan.

JB L'Esperance (ChFC) and Andrea Cervena (CFP®) work with business owner clients across Minnesota, Michigan, and the broader Midwest to keep coverage aligned with both business growth and personal financial goals as circumstances change.

Frequently Asked Questions

Should a business owner have life insurance?

No law requires it, but business owners carry compounding risks — debt obligations, successor funding gaps, partner buyout commitments, and personal income replacement — that can permanently damage both the business and the owner's family if left unaddressed.

Can an LLC get a life insurance policy?

Yes. An LLC can own policies on its members or key employees, pay premiums, and be named as beneficiary. However, entity ownership has significant tax and legal implications — including Connelly-related estate tax risk for redemption arrangements — so legal and tax counsel is strongly recommended before structuring ownership.

Can I get life insurance if I have cirrhosis?

Cirrhosis is a significant underwriting risk factor. Some insurers will decline coverage depending on severity and treatment history; others may offer coverage at higher premiums. Working with an experienced advisor who can access multiple carriers gives you the best chance of finding a workable option.

What is the difference between key person insurance and a buy-sell agreement?

Key person insurance pays the business when a critical individual dies, providing funds to offset lost revenue and cover replacement costs. A buy-sell agreement uses life insurance proceeds to fund the purchase of a deceased owner's equity stake, enabling a smooth ownership transition between surviving partners or heirs.

Are life insurance premiums tax-deductible for business owners?

In most cases, no — premiums are not deductible when the business or owner is the beneficiary under IRC Section 264. Exceptions include employer-paid group term life premiums within IRS limits and certain executive bonus arrangements — consult a tax advisor to confirm what applies to your structure.

How much life insurance does a business owner need?

Coverage depends on your business debt, valuation, payroll obligations, and personal income needs. The common 5–10x salary guideline ignores business-specific liabilities, so a layered needs analysis covering both dimensions — conducted with a qualified financial advisor — gives you a more accurate target.