Introduction

Recessions aren't surprises. They're predictable features of economic cycles — the question is never if one arrives, but whether your business is ready when it does.

Small businesses bear the brunt of that timing problem. According to the SBA's 2024 FAQ, small businesses contribute 43.5% of U.S. GDP and employ nearly half of all private-sector workers. The stakes are enormous — and the vulnerability is real. During the 2007–2009 recession, employment at establishments with fewer than 50 employees fell 10.4%, compared to 7.5% at larger firms.

The businesses that come through downturns intact don't survive by accident. They built plans before warning signs appeared — not scrambling responses after the fact.

Here, we cover six concrete steps small business owners can take now to build a recession-resilient plan: stress testing cash flow, making smart cost cuts, retaining customers, diversifying revenue, staying adaptable, and continuing to invest strategically.

Key Takeaways:

- The median small business holds just 27 days of cash reserves — stress testing shows exactly where you stand

- Cutting marketing and key staff early is one of the most damaging recession mistakes

- Retaining existing customers costs far less than acquiring new ones during a downturn

- Businesses that maintain strategic investment during recessions recover faster than those that go dark

- Working across tax, insurance, retirement, and operations together shows you exactly where your vulnerabilities are

Step 1: Run 12–18 Month Cash-Flow Stress Tests

What Stress Testing Actually Means

A cash-flow stress test isn't a single worst-case prediction. It's a range of "what if" models — typically projecting how your finances look under 10%, 20%, and 30% revenue decline scenarios across a 12–18 month window.

The goal: know your minimum monthly cash requirement to stay operational before you ever need it.

The urgency is real. JPMorgan Chase Institute research on 600,000 small businesses found the median small business holds just 27 cash-buffer days in reserve. Restaurants average 16 days. That's not a runway — it's a ledge.

What to Include in Your Model

Run projections across each of these categories:

- Payroll obligations — your largest fixed cost and the last thing you want to discover you can't cover

- Rent and lease commitments — often non-negotiable in the short term

- Debt service — loan payments don't pause because revenue drops

- Operating expenses — utilities, insurance, software, supplies

- Owner compensation — many owners skip this; don't

Don't Forget Receivables

Most stress-test models focus on the expense side. That's only half the picture. During downturns, customers pay slower. The Federal Reserve's 2024 payments report found roughly 4 out of 5 small firms face customer payment challenges. A 2025 QuickBooks survey found 56% of small businesses were owed money from unpaid invoices, averaging $17,500 per business.

Factor this into your projections now by:

- Tightening invoice payment terms (net-15 instead of net-30)

- Setting up automatic follow-ups on overdue accounts

- Building delayed payment assumptions directly into your cash-flow models

This is where working with a financial advisor pays off. The team at Barking Sands Capital specializes in small business planning and can translate raw cash-flow data into scenario models that reflect how your specific business actually behaves — not just generic projections. That context matters when every decision carries real consequences.

Step 2: Make Smart Cuts Without Sacrificing Growth

Strategic Optimization vs. Reactive Slashing

Reactive cuts feel decisive but often eliminate the things that generate revenue and maintain morale. Strategic optimization is different — it examines every line item against one question: is this generating a return?

Start your audit here:

- Vendor and supplier contracts — renegotiate; many vendors will offer better terms rather than lose a client

- Software subscriptions — you're likely paying for tools your team stopped using months ago

- Redundant systems — consolidate where one platform can replace two

- Insurance coverage — review for appropriate fit, not just lowest premium

What Not to Cut

Knowing what to cut is only half the equation. Knowing what to protect is where most businesses go wrong.

Nationwide's 2022 small-business survey found 58% of owners explored expense cuts during economic stress, and 23% planned furloughs or hour reductions. Many made cuts that cost them more later.

The three areas most commonly cut too early — and most damaging to cut:

- Marketing — pulling back advertising when competitors do the same hands market share to whoever stays visible

- Training and development — skills atrophy quickly; rebuilding is expensive

- Key personnel — employee turnover costs an average of 40% of annual salary to replace, according to research from Equitable Growth

Smart cuts protect the cash that funds growth. Looking lean on a spreadsheet while gutting your marketing and team will cost far more to repair than you saved.

Step 3: Build a Customer Retention Playbook

Why Existing Customers Are Your Most Valuable Asset in a Downturn

Acquiring new customers during a downturn is expensive — Harvard Business Review reports it costs 5 to 25 times more to acquire a new customer than to retain an existing one. Meanwhile, research by Reichheld and Sasser found that reducing customer defections by just 5% can increase profits by 25% to 85%.

Loyal customers who see consistent value from your business are more likely to maintain spending even when their budgets tighten. Your retention strategy should be built before a downturn — not assembled in the middle of one.

Core Components of a Retention Playbook

A strong playbook covers three areas:

- Regular email touchpoints with genuinely useful content (not just promotions)

- Personal outreach to top clients to understand how their needs are shifting

- Payment plans or extended terms for long-standing customers facing cash pressure

- Tiered service options so clients can stay engaged at a lower spend level

- Proactive offers before customers start shopping alternatives

- Membership programs or exclusive access that reward continued business

- Consistent recognition — clients remember how you treated them when things were hard

McKinsey's 2025 consumer research found 79% of consumers globally were actively trading down during periods of economic uncertainty. The businesses that retained the most customers weren't necessarily the cheapest — they were the ones that had already built a track record of delivering clear, consistent value before the pressure hit.

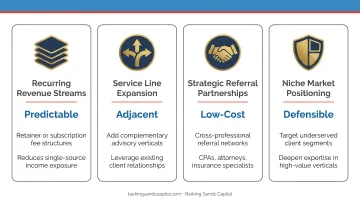

Step 4: Diversify Your Revenue Streams

Concentration Risk Is a Recession Multiplier

A business that depends on one product, one service line, or one major customer segment has a single point of failure. When that segment contracts — and in a recession, something always contracts — there's no buffer.

Diversification builds that buffer. It doesn't mean adding unrelated businesses. It means adding complementary revenue that serves your existing capabilities.

Practical diversification strategies:

- Tiered pricing — offer a lower-cost version of your core service for budget-constrained customers rather than losing them entirely

- Recurring or subscription income — a McKinsey analysis of subscription businesses found these models hold up well during economic downturns, outperforming transactional revenue

- B2B partnerships — serving businesses in less-affected sectors can offset declines in consumer-facing revenue

- Identify adjacent customer segments — who else benefits from what you already do well, without requiring new infrastructure

A Caution on Overextension

Diversification should solve a real need in a market you understand. Spreading into unfamiliar territory during a lean period strains resources and dilutes focus — often without producing new revenue or protecting the core business you already have.

A useful test: Can we serve this new segment well with our current team and capabilities? If the honest answer is no, the timing is wrong.

HBR's research on small business resilience points to Dunsters Farm as a clear example: the company pivoted from B2B foodservice to B2C online delivery during COVID-19 lockdowns by drawing on its existing logistics, product knowledge, and supplier relationships — not by starting from scratch.

Step 5: Stay Flexible and Adaptable

Businesses that survive recessions tend to share one trait: they monitor economic signals closely and adjust before conditions force their hand. Rigidity — clinging to strategies that worked in a growth environment — is one of the most common causes of recession-era failure.

Operational flexibility in practice:

- Convert fixed expenses to variable ones where possible: fractional staffing instead of full-time headcount for non-core functions gives you room to maneuver when revenue dips

- Cross-train employees so key roles can flex without adding headcount

- Shift to quarterly planning cycles during uncertainty — annual reviews work in stable conditions, but 90-day cadences let you course-correct before small problems become structural

- Build a continuity plan: the U.S. Chamber of Commerce Foundation recommends identifying business priorities, training staff on emergency preparedness, and reviewing insurance coverage as baseline readiness steps

The SBA's recovery guidance is direct: look for opportunities created by changed customer behavior, pivot where necessary, and streamline operations continuously. Businesses that act on these shifts early — rather than reacting once revenue is already falling — consistently recover faster and emerge in stronger competitive positions.

Step 6: Keep Investing in Your Business and Team

The Counterintuitive Move That Works

The instinct during a recession is to stop spending. It's understandable — and often wrong.

HBR's study of companies across multiple recessions found that only 9% emerged stronger than before. What distinguished them: they combined selective cost reductions with continued investment in marketing, people, and operations. Pure cost-cutters consistently underperformed.

The Marketing Case

When competitors pull back advertising spend, share of voice gets cheaper and more impactful. Nielsen research confirms that reducing media spend may improve channel ROI by only 4% while directly reducing sales volume. WARC's analysis found that cutting advertising during recessions often causes long-term brand damage that outlasts the downturn itself.

Maintaining even a targeted, reduced marketing presence while rivals go quiet is one of the clearest competitive advantages available to small businesses during a recession.

The People Case

Transparent communication with employees about business challenges builds loyalty when it's most needed. SHRM's guidance is clear: open, compassionate communication before, during, and after difficult periods mitigates cultural damage and helps teams move forward.

Losing key employees during a downturn is particularly costly — both the direct replacement cost (averaging 40% of annual salary) and the institutional knowledge that walks out the door with them. Cross-training and skills development reduce that risk while increasing operational flexibility.

Connecting to Long-Term Financial Planning

Knowing which investments to protect and which to deprioritize is difficult without a clear picture of your full financial position. A financial advisor who coordinates across tax, insurance, retirement, and business planning can make those calls more confidently.

Barking Sands Capital's InteProcess™ integrates these disciplines into a unified strategy for small business owners, identifying cross-functional opportunities — like timing Roth conversions when income is lower, or restructuring for tax efficiency during a downturn — that a fragmented approach would overlook. Principal J.B. L'Esperance (ChFC) and CFP® Andrea Cervena specialize in coordinated plans that address the full complexity of a business owner's financial picture.

Frequently Asked Questions

How do I prepare for a recession as a small business owner?

Start before the warning signs arrive. Build cash reserves, stress test your finances under multiple revenue-decline scenarios, reduce unnecessary debt, and create a written scenario plan so you respond decisively when conditions tighten.

What should a small business do during a recession?

Protect cash flow first, then double down on existing customer relationships. Make targeted cost cuts rather than blanket reductions, and continue strategic investments in marketing and people to stay positioned for recovery when conditions improve.

What small businesses do well during a recession?

Essential services — healthcare, auto repair, accounting, childcare, home repair — are historically more resilient during downturns. Even non-essential businesses can outperform by delivering clear, consistent value to loyal customers and maintaining strong communication throughout.

How much cash reserve should a small business have?

SCORE recommends 3 to 6 months of operating expenses in liquid reserves, with 10% of monthly revenue directed to an emergency fund. That target may need to be higher depending on your fixed cost structure, revenue concentration, and industry volatility.

Should I cut my marketing budget during a recession?

Cutting marketing is one of the most common — and costly — mistakes small businesses make during downturns. Even a reduced, targeted spend typically yields a competitive advantage when rivals go quiet, and the brand damage from going dark can outlast the recession itself.

How can a financial advisor help my small business during a recession?

A financial advisor with small business expertise can model cash-flow scenarios, identify risks across your full financial picture, and coordinate tax, insurance, investment, and retirement planning into a single, coordinated strategy. That integrated view goes beyond what a banker or accountant typically provides on their own.