IRMAA, or Income-Related Monthly Adjustment Amount, is an additional premium that higher-income Medicare beneficiaries pay on top of standard Part B and Part D costs each month. According to CMS, roughly 8% of Medicare Part B enrollees pay IRMAA surcharges — a smaller share than most people assume, but one with significant financial consequences for those it affects.

Understanding IRMAA matters whether you're already on Medicare or planning to enroll within the next several years. The surcharge is tied to income decisions you made two years ago, operates on steep bracket cliffs, and can add thousands of dollars annually to your healthcare costs.

This guide explains exactly how IRMAA works, what the 2026 brackets look like, and what you can do about it.

Key Takeaways

- IRMAA is a surcharge on Medicare Part B and Part D premiums — it does not apply to Part A.

- Your 2024 federal tax return determines your 2026 IRMAA surcharge (the two-year lookback rule).

- In 2026, surcharges begin when MAGI exceeds $109,000 (single) or $218,000 (married filing jointly).

- IRMAA uses cliff-style brackets: crossing a threshold by $1 triggers the full tier surcharge.

- You can appeal your IRMAA using Form SSA-44 if a qualifying life event reduced your income.

What Is IRMAA?

IRMAA is a dollar amount added to your monthly Medicare Part B and Part D premiums when your income exceeds certain thresholds set by the Social Security Administration. It is not a separate program or penalty — it's simply a higher premium tier.

Why IRMAA Exists

Standard Medicare premiums cover only a fraction of the actual cost of providing coverage. Congress introduced income-related Part B premiums in 2007 and extended the same structure to Part D in 2011, requiring higher-income beneficiaries to cover a larger share of program costs.

Which parts of Medicare IRMAA affects:

- Part B (medical insurance) — yes

- Part D (prescription drug coverage) — yes

- Part A (hospital insurance) — no, even for beneficiaries who pay a Part A premium

One Common Point of Confusion

The phrase "Medicare income limits" gets used in two completely unrelated ways:

- IRMAA brackets — upper-income thresholds above which you pay more

- Medicare Savings Programs — lower-income thresholds for people with limited resources who may pay less

These programs have nothing to do with each other. If you've seen "income limits" mentioned in Medicare research, check which program is being referenced — the difference matters significantly.

How IRMAA Is Calculated

The Two-Year Lookback Rule

The SSA determines your IRMAA based on your federal income tax return from two years prior. Your 2026 Medicare premiums are calculated using your 2024 return — because when 2026 premiums are set in late 2025, the 2024 return is the most recently filed data available.

This lag has real consequences. Income from a job you left three years ago or a one-time property sale could still be driving your current surcharge.

The MAGI Used for IRMAA

IRMAA uses a Medicare-specific version of Modified Adjusted Gross Income (MAGI): your AGI plus tax-exempt interest (Form 1040, lines 11 and 2a). This differs from MAGI calculations used elsewhere in the tax code.

Income sources that count toward IRMAA MAGI:

- Traditional IRA and 401(k) distributions, including Required Minimum Distributions (RMDs)

- Roth conversions (taxable amount)

- Taxable Social Security benefits

- Capital gains

- Pension and annuity income

- Net rental income

- Tax-exempt interest (added back even though it's tax-free for income tax purposes)

Income sources that do NOT count:

- Qualified Roth IRA distributions (when tax-free and excluded from AGI)

- HSA distributions for qualified medical expenses

- Return of principal or cost basis from investment account sales

Knowing which income sources count — and which don't — is what makes IRMAA planning actionable. Roth distributions, for example, can replace taxable withdrawals without adding a dollar to your MAGI.

How the SSA Notifies You

Once your MAGI triggers a surcharge, the SSA sends a written notice each fall with your new premium amount and the income data behind it. For Part B, the surcharge is automatically deducted from your Social Security check. Part D IRMAA works the same way — deducted directly from your benefit when possible.

2026 IRMAA Brackets: What You Could Owe

The standard 2026 Part B premium is $202.90/month. The following surcharges apply based on 2024 MAGI, per the CMS 2026 Medicare Parts A & B Premiums and Deductibles fact sheet.

2026 Part B IRMAA Brackets

| 2024 MAGI (Single) | 2024 MAGI (Married Filing Jointly) | Monthly Part B IRMAA | Total Monthly Part B Premium |

|---|---|---|---|

| ≤ $109,000 | ≤ $218,000 | $0.00 | $202.90 |

| $109,001–$137,000 | $218,001–$274,000 | $81.20 | $284.10 |

| $137,001–$171,000 | $274,001–$342,000 | $202.90 | $405.80 |

| $171,001–$205,000 | $342,001–$410,000 | $324.60 | $527.50 |

| $205,001–$499,999 | $410,001–$749,999 | $446.30 | $649.20 |

| ≥ $500,000 | ≥ $750,000 | $487.00 | $689.90 |

2026 Part D IRMAA Surcharges

Part B isn't the only place IRMAA shows up. Part D IRMAA is a separate surcharge added on top of your specific plan's premium.

| 2024 MAGI (Single) | 2024 MAGI (Married Filing Jointly) | Additional Monthly Part D IRMAA |

|---|---|---|

| ≤ $109,000 | ≤ $218,000 | $0.00 |

| $109,001–$137,000 | $218,001–$274,000 | $14.50 |

| $137,001–$171,000 | $274,001–$342,000 | $37.50 |

| $171,001–$205,000 | $342,001–$410,000 | $60.40 |

| $205,001–$499,999 | $410,001–$749,999 | $83.30 |

| ≥ $500,000 | ≥ $750,000 | $91.00 |

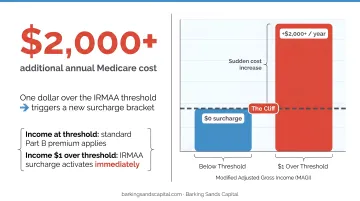

The Cliff Effect: Why $1 of Extra Income Can Cost Thousands

IRMAA brackets don't phase in gradually. Cross a tier boundary by a single dollar and you owe the full surcharge for that entire tier for the full year.

Here's a concrete example: A married couple with $218,000 MAGI pays zero IRMAA. If their MAGI reaches $218,001 — say, from a slightly larger RMD — both spouses immediately owe Tier 1 surcharges.

- Per spouse monthly: $81.20 (Part B) + $14.50 (Part D) = $95.70

- For both spouses, annualized: $2,296.80 in added premiums

One dollar over the threshold. Over $2,200 in annual consequences.

Married Filing Separately: A Costly Trap

Spouses who file separately but lived together at any point during the year face a severely compressed bracket structure — just two IRMAA tiers instead of six. The first surcharge tier kicks in at $109,001 in MAGI per person, at a steep $446.30/month for Part B alone.

Couples who file separately to manage one spouse's income often discover this approach backfires on Medicare costs.

How to Reduce or Appeal Your IRMAA

Appealing with Form SSA-44

If your income has dropped significantly since the lookback year, you don't have to wait for the SSA's records to catch up. You can file Form SSA-44 to request that the SSA use a more recent year's income instead.

Qualifying life-changing events include:

- Retirement or reduction in work hours

- Marriage or divorce/annulment

- Death of a spouse

- Loss of income-producing property

- Loss of pension income

- Employer settlement payment

Submit the form with documentation of your current income and the nature of the life-changing event. There is a formal 60-day window to request reconsideration after receiving an IRMAA determination notice — though SSA-44 life-event requests operate under a separate process.

Income Planning Strategies

When a qualifying life event isn't in the picture, proactive income planning is your most effective lever. These strategies can reduce or eliminate IRMAA exposure entirely:

- Manage RMD timing and size — large distributions in a lookback year can push MAGI over a bracket threshold two years later

- Sequence Roth conversions carefully — taxable conversion amounts count toward IRMAA MAGI, but the converted funds then grow and distribute tax-free, removing them from future MAGI calculations

- Avoid stacking one-time income events — selling a rental property and taking a large RMD in the same year compounds the effect

- Use Roth distributions strategically — qualified Roth IRA distributions don't count toward IRMAA MAGI, making them particularly useful for managing income in Medicare years

These strategies work best when built into a retirement income plan well before Medicare enrollment. Modeling projected MAGI across multiple years — rather than reacting to a single year's income — is what separates intentional bracket management from last-minute damage control.

IRMAA and Your Retirement Plan

IRMAA isn't a minor line item. For a married couple where both spouses are subject to Medicare premiums, the annual cost difference between tiers is substantial:

| Surcharge Tier | Couple's Annual Added Cost |

|---|---|

| Tier 1 | $2,296.80 |

| Tier 2 | $5,769.60 |

| Tier 3 | $9,240.00 |

| Tier 4 | $12,710.40 |

| Tier 5 | $13,872.00 |

Source: CMS 2026 fact sheet; assumes both spouses subject to Part B and Part D IRMAA.

Because IRMAA is based on income from two years prior and resets annually, it touches nearly every retirement income decision: RMD amounts, Roth conversion timing, asset sales, and even tax-exempt bond interest. A decision that looks clean from a tax standpoint may quietly create a Medicare premium problem two years later.

A comprehensive retirement plan treats IRMAA as part of an integrated picture — Medicare costs, income timing, tax brackets, and distribution strategy all affecting each other. Managing one lever without considering the others can shift a couple into a higher IRMAA tier unexpectedly.

At Barking Sands Capital, Curtis Hewitt specializes in Medicare Planning and Long-Term Care, working alongside the firm's retirement and tax planning advisors to identify IRMAA exposure before it materializes. Through the firm's proprietary InteProcess™, which coordinates planning across insurance, tax, and retirement disciplines, IRMAA bracket management is built into the retirement income plan from the start — not addressed as an afterthought when the first premium notice arrives.

For clients approaching Medicare enrollment, the window to act is typically two to three years before coverage begins — when income-shifting strategies like Roth conversions or deferred distributions can still move the needle on future bracket placement.

Frequently Asked Questions

What is the income-related monthly adjustment amount in IRMAA?

IRMAA (Income-Related Monthly Adjustment Amount) is a surcharge added to Medicare Part B and Part D premiums for beneficiaries whose MAGI exceeds annual thresholds set by the SSA. It's not a separate program — it's an add-on to your existing premium that increases based on your income tier.

What are the IRMAA brackets for 2026?

In 2026, surcharges begin when MAGI exceeds $109,000 for single filers or $218,000 for married filing jointly, with five income tiers rising to $500,000+ (single) or $750,000+ (MFJ). See the bracket tables earlier in this article for exact monthly amounts at each tier.

How do I stop IRMAA surcharges?

You can reduce or eliminate IRMAA through several approaches:

- Keep your MAGI below the applicable threshold through proactive income planning

- File Form SSA-44 if a qualifying life event reduced your income

- Work with a financial advisor on strategies like Roth conversions or managing RMD timing to lower your lookback-year MAGI

What time of year is IRMAA recalculated?

IRMAA is recalculated annually. The SSA typically sends determination notices in the fall, based on your most recently available federal tax return (from two years prior), before the new coverage year begins.

Does IRMAA apply to Medicare Advantage plans?

Yes. Medicare Advantage enrollees still owe the standard Part B premium plus any IRMAA surcharge, in addition to their plan's own premium. If the plan includes Part D drug coverage, the Part D IRMAA surcharge applies as well.

Can I appeal my IRMAA if my income has gone down since the lookback year?

Yes. If a qualifying life-changing event — such as retirement, divorce, or death of a spouse — reduced your income, you can file Form SSA-44 with supporting documentation, and the SSA may use a more recent year's income to recalculate your surcharge.