This guide focuses specifically on tax planning costs — the proactive, year-round strategy work that reduces what you owe — not tax preparation fees. You'll find pricing tiers, the key cost drivers, a full service breakdown, and a practical framework for choosing the right level of engagement.

Key Takeaways

- Basic annual tax planning sessions typically run $1,500–$5,000; quarterly ongoing engagements cost $2,500–$8,000/year

- Entity type is the strongest single cost driver — S-corps and C-corps require significantly more planning than sole proprietors

- Tax planning fees are generally deductible as ordinary and necessary business expenses under IRS Publication 334

- Year-round planning consistently reduces your tax bill more than a single annual conversation ever will

- When tax strategy connects to retirement and estate planning, integrated advisory services outperform standalone tax prep

How Much Does Small Business Tax Planning Cost in 2026?

Unlike tax preparation, which has a defined annual scope, tax planning costs vary widely because the service itself ranges from a single strategy session to a full year-round advisory engagement. Confusing the two leads to a predictable mistake: budgeting for a $400 tax return prep fee when what the business actually needs is a $3,000 quarterly planning engagement.

Three common budgeting errors to avoid:

- Assuming tax planning and tax preparation cost the same

- Budgeting only for filing season, then scrambling in December

- Choosing an advisor on price alone without evaluating the scope of what's included

Here's how the three main tiers break down.

Entry-Level / Basic Tax Planning

Typical cost: $1,500–$5,000 (one-time or annual)

According to SmartVault's 2025 CPA pricing guide, one-time strategic tax plans fall in this range, covering a tax-savings analysis and summary report.

What's typically included:

- Single annual strategy consultation

- Business entity structure review

- Identification of major deductions and credits

- Estimated tax payment guidance

What's not included: quarterly check-ins, bookkeeping support, multi-year projections, or ongoing advisory access.

Best for: Sole proprietors, freelancers, and single-member LLCs in their first few years with straightforward income and minimal complexity.

Mid-Range / Ongoing Tax Planning Engagement

Typical cost: $2,500–$8,000/year

This tier reflects what SmartVault's guide identifies as quarterly planning packages — recurring engagements that include projections, planning calls, and ongoing implementation throughout the year.

What's typically included:

- Quarterly strategy sessions

- Estimated tax calculations and mid-year adjustments

- Multi-year tax projections

- Retirement contribution optimization

- S-corp salary and distribution planning

- Some bookkeeping review

Best for: S-corps, multi-member LLCs, and growing businesses with $250K–$1M in revenue that need consistent guidance, not just reactive, year-end adjustments.

High-End / Fully Integrated Tax and Financial Planning

Typical cost: $6,000–$60,000+/year

This tier merges tax strategy with comprehensive financial advisory work. SmartVault's guide shows client accounting services (CAS) packages running $500–$5,000+ per month, with fractional CFO services ranging from $3,000–$12,000+ per month. HD Growth Partners lists fractional CFO engagements starting at $24,000 annually.

What's typically included:

- Year-round advisory access

- Multi-state tax compliance

- Entity restructuring analysis

- Coordination with estate and retirement planning

- Audit representation

- Integration with investment strategy

Best for: C-corps, high-revenue businesses, and owners whose tax strategy must connect to retirement, estate, and investment decisions in a coordinated way.

Key Factors That Affect Small Business Tax Planning Costs

Tax planning pricing depends on a mix of business-specific, advisor-specific, and engagement-specific variables. Understanding these helps you evaluate quotes accurately.

Business Entity Type and Structure

Entity type is the single strongest cost driver. A sole proprietor filing a Schedule C involves far less planning complexity than an S-corp requiring reasonable compensation analysis, K-1 distributions, and payroll coordination.

For context on preparation fees alone (which are lower than planning fees):

| Entity Type | Typical Prep Fee Range |

|---|---|

| Sole proprietor (Schedule C) | $400–$1,200 |

| S-corporation (Form 1120S) | $750–$1,500 |

| Partnership / Multi-member LLC (Form 1065) | $850–$1,800 |

| Multi-state returns | Often exceeds $2,000 |

Planning fees run higher than preparation fees — often 2–3x — because they involve strategy, not just compliance.

Revenue Size and Financial Complexity

Revenue scale multiplies the scope of work. A business with $100K in revenue has straightforward planning needs. One crossing $500K typically requires more documentation, multi-year projections, and cross-functional decisions.

That complexity deepens when the owner also has rental income, investment accounts, or business interests in multiple states. Multiple income streams create interconnected planning decisions: a rental property loss might interact with passive income rules; investment gains might affect QBI deduction eligibility. Each layer adds advisor time.

Scope of Services and Advisor Credentials

Not all tax advisors are the same, and pricing reflects it:

- Non-credentialed preparers — lower cost, focused on compliance with limited planning depth

- CPAs offering planning — mid-range cost, strong technical expertise, fluent in tax code

- Enrolled Agents (EAs) — IRS-credentialed, well-suited for compliance and IRS representation

- CFP® professionals — higher cost, but integrate tax planning with retirement, estate, and investment strategy

For business owners where tax decisions intersect with retirement funding, estate transfer, and investment management, working with a CFP® or an advisory firm that coordinates across these disciplines — like Barking Sands Capital, whose InteProcess™ integrates tax, legal, insurance, and retirement planning — often delivers broader value than working with a tax preparer alone.

Number of States and Special Situations

Multi-state operations significantly increase planning costs. Each state where a business has tax nexus creates separate filing obligations, different tax structures, and additional compliance requirements. Research from Avalara found that businesses with 20–499 employees spent an average of more than $17,000 per month on sales-tax compliance activities — a number that grows fast once nexus spans multiple jurisdictions.

Other common cost multipliers:

- Foreign income or international operations

- Cryptocurrency transactions

- Prior-year amendments

- Business transitions or ownership changes

What's Included in Tax Planning Costs: A Full Breakdown

The total cost of tax planning goes beyond a single strategy session. A realistic budget accounts for the type of engagement, how frequently you need access, and any add-ons that come up during the year.

Initial Tax Strategy Consultation

Cost: $500–$2,500 (one-time or annual)

This is the starting point for any planning engagement. It typically covers a business overview, entity structure review, identification of major planning opportunities, and estimated tax positioning for the year ahead. Some advisors charge this as a standalone fee; others fold it into a larger retainer.

Quarterly Tax Planning Check-Ins

Cost: Included in $2,500–$8,000/year retainers, or $500–$1,500 per session as an add-on

Quarterly sessions are where proactive planning actually happens. Each check-in typically covers:

- Reviewing income to date and adjusting estimated payments

- Flagging relevant legislative changes

- Making mid-year moves before the window closes

Skipping these and catching up in March is the most common reason business owners miss savings.

Bookkeeping Cleanup or Catch-Up

Cost: $300–$3,500+ depending on backlog

Many tax planners require clean financial records before planning can begin. Disorganized books trigger cleanup fees before any strategy work starts. According to the NSA's 2024 report, 67% of firms charge an additional $100–$200 for disorganized or incomplete client files. For more significant backlogs, SDO CPA's 2026 guide lists catch-up bookkeeping at $300–$500 for 1–3 months behind, climbing to $3,500+ for extensive backlogs.

Annual Retainer or Advisory Package

Cost: $2,500–$60,000+/year depending on scope

Retainers bundle the following into one predictable annual fee:

- Ongoing advisory access

- Return preparation

- Quarterly reviews

- Bookkeeping (in some packages)

This model pays off once a business needs consistent guidance — typically when quarterly estimated taxes, payroll, retirement contributions, and year-end strategy all need coordination. Paying per service at that point usually costs more.

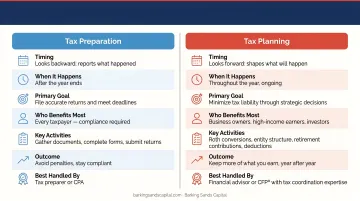

Tax Planning vs. Tax Preparation: Understanding the Cost Difference

Most business owners use these terms interchangeably — but they describe fundamentally different services with very different price tags.

| Tax Preparation | Tax Planning | |

|---|---|---|

| Purpose | Compliance — file an accurate return | Optimization — reduce what you owe |

| Timing | Annual, after the year ends | Year-round, before decisions are made |

| Typical cost | $400–$2,000+ depending on entity | $1,500–$60,000+/year depending on scope |

| Outcome | Correctly filed return | Legally minimized tax liability |

That table makes the distinction clear. Tax preparation is reactive — by the time your preparer sees your books in February, most of the year's tax decisions are already locked in. Tax planning is where the actual savings happen: the entity structure you chose, the retirement contributions you made, the equipment you purchased before December 31, and the distributions you timed correctly.

The permanent changes under the One Big Beautiful Bill Act create concrete planning advantages heading into 2026 — but only for business owners who act before the year ends:

- 100% bonus depreciation on qualifying property purchases

- Permanent 20% QBI deduction for pass-through business income

- Increased Section 179 limit of $2.5 million for equipment expensing

None of these benefits show up automatically on a tax return. They require decisions made during the year, not after it.

How to Get the Most Value from Your Tax Planning Investment

The right scope of service depends on where the business actually is — not where it might be in three years. Overpaying for a full CFO retainer when a solo freelancer needs one annual session wastes money. Underpaying for basic prep when an S-corp owner needs quarterly strategy leaves real savings on the table.

A practical budgeting framework:

- Entity type sets the baseline — sole proprietors and single-member LLCs can often start with an entry-level annual consultation; S-corps and multi-member LLCs typically need ongoing engagement

- Variable income demands more frequent check-ins — if your income fluctuates or you have payroll obligations, quarterly reviews aren't optional

- Integration matters when planning spans multiple disciplines — if tax decisions affect retirement contributions, estate planning, or investment strategy, work with an advisor who coordinates across all three

- Get your books current first — if your records aren't up to date, budget for cleanup before engaging a planner

For business owners whose tax strategy connects to retirement, estate, and investment planning, working with an independent, fee-based financial advisor makes coordination more practical. Barking Sands Capital's proprietary InteProcess™ coordinates tax strategy alongside legal, insurance, and retirement planning, so a decision in one area doesn't produce unintended consequences in another.

Three ways to reduce planning costs without sacrificing quality:

- Maintain clean, organized records year-round — this directly reduces advisor time

- Engage a planner early in the tax year, not at year-end when options are limited

- Ask about bundled pricing when combining tax planning with bookkeeping or financial planning services

What Small Business Owners Often Get Wrong About Tax Planning Costs

Focusing Only on the Upfront Fee

The cheapest option rarely delivers the most value. An advisor charging $400 for a return prep and a 20-minute "planning chat" isn't doing tax planning — they're doing tax preparation with a conversation attached. Missed deductions, wrong entity structure, and last-minute decisions each cost more in taxes than the fee saved.

Treating Tax Planning as a One-Time Annual Event

According to NFIB's 2024 Tax Survey, 88% of small business owners who use a tax professional cite tax-law complexity as the reason. That complexity doesn't resolve itself after one April conversation. Businesses with variable income, payroll obligations, or significant deductions need quarterly reviews — not because it's ideal, but because the decisions that affect taxes happen throughout the year.

Underestimating the Cost of No Planning

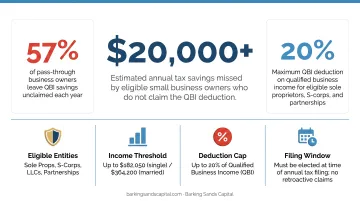

Tax planning gaps carry a measurable cost. NFIB's 2024 survey found that 51% of small business owners were not at all familiar with TCJA changes, and 52% were unfamiliar with the 20% Small Business Deduction — now a permanent deduction under the OBBBA.

On $400K in qualified business income, missing the QBI deduction alone could mean $16,000–$20,000 in avoidable taxes. A planning engagement that surfaces that deduction pays for itself many times over.

Three patterns tend to drive these oversights:

- Fee fixation — choosing the lowest-cost provider without evaluating what's actually included

- Annual-only reviews — skipping mid-year check-ins when income, payroll, or deductions shift

- Familiarity gaps — not knowing which deductions apply until after the tax year closes

Frequently Asked Questions

What is the $400 rule for self-employed people?

The IRS requires self-employed individuals to file a return if net self-employment income is $400 or more, because that threshold triggers self-employment tax obligations. This means even early-stage solo businesses have a tax filing requirement — and enough complexity to benefit from at least a basic planning consultation.

What is the difference between tax planning and tax preparation for small businesses?

Tax preparation is the process of filing an accurate return after the year ends. Tax planning involves proactive strategies implemented throughout the year to legally reduce tax liability before the return is ever filed. Planning costs more upfront, but for most businesses operating beyond the simplest structures, identified savings routinely outpace the fee by a meaningful margin.

How much does small business tax planning cost in 2026?

Basic annual planning sessions run roughly $1,500–$5,000. Quarterly ongoing engagements typically cost $2,500–$8,000/year. Fully integrated advisory retainers for complex businesses can range from $6,000 to $60,000+ annually, depending on scope, entity type, and whether the engagement includes CFO-level services.

Is the cost of tax planning deductible for a small business?

Yes. Under IRS Publication 334, legal and professional fees — including accountant and advisor fees — that are ordinary, necessary, and directly related to operating the business are deductible as business expenses. Fees clearly tied to business operations are deductible in full; fees covering personal tax matters, such as individual return preparation, are not — and mixed-purpose engagements should be allocated accordingly.

When should a small business owner move from tax prep to full tax planning?

Common triggers include crossing $100K–$250K in revenue, adding employees, changing entity structure, starting a retirement plan, or acquiring rental property. At that point, the combination of entity-level decisions, payroll tax exposure, and deduction timing creates enough opportunity that a proactive advisor typically finds more than their fee in a single planning review.

How do advisor credentials affect tax planning costs?

CPAs, Enrolled Agents, and CFP® professionals generally charge more than non-credentialed preparers, but bring greater expertise in identifying deductions, ensuring compliance, and — in the case of financial planners — integrating tax strategy with retirement and estate goals. For a small business owner juggling entity structure, retirement contributions, and estate considerations simultaneously, a credentialed advisor's ability to coordinate across all three typically justifies the higher fee.