Many high earners also start the serious savings work later than they realize — after years in graduate school, residency, or building a business. By the time income peaks, the compounding window is shorter than it should be.

This guide walks through a practical framework for moving beyond the basics: how to maximize every tax-advantaged account available to you, unlock advanced Roth strategies, use an HSA as a stealth retirement account, and manage taxes and lifestyle inflation so the money you earn actually stays working for you.

Key Takeaways

- High earners should target at least 25% of gross income saved for retirement — the standard 15% guideline falls short given limited Social Security replacement and higher income needs

- Maxing a 401(k) covers only a small fraction of a high earner's salary, so additional accounts are essential

- Backdoor Roth IRAs and mega backdoor Roth strategies let high earners bypass income restrictions to build tax-free growth

- Asset location and Roth conversion timing matter just as much as which accounts you choose

- Tax and lifestyle decisions erode or protect wealth just as much as investment returns

Why High Earners Face a Unique Retirement Savings Gap

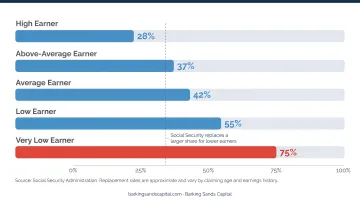

The Social Security Problem

Social Security was built with a progressive benefit structure — it's designed to replace a higher share of income for lower earners than for higher ones. SSA actuarial data from June 2025 shows exactly how steep that drop-off is:

| Earner Type | Career-Average Earnings | Replacement Rate |

|---|---|---|

| Very low earner | $18,064 | 76.5% |

| Low earner | $32,515 | 55.6% |

| Medium earner | $72,256 | 41.7% |

| High earner | $115,609 | 34.1% |

| Steady maximum earner | $176,100 | 27.4% |

For someone earning $300,000 or more, the gap is even wider. The higher your income, the more retirement funding falls entirely on your own savings — and that math gets more demanding the longer you wait to start.

The Late-Start Paradox

Physicians, attorneys, and executives often don't reach peak earnings until their mid-30s or later. According to the AAMC, residency training alone lasts 3 to 7 years after medical school, with many residents beginning around age 28. Add fellowship training for specialists, and a doctor might not see attending-level income until their mid-30s.

That timeline compresses the compounding window considerably. Someone who starts saving aggressively at 35 instead of 25 doesn't just miss 10 years of contributions — they miss 10 years of growth on those contributions.

The Math Problem With Standard Advice

Fidelity's baseline savings guideline is 15% of pre-tax income, but that figure assumes an early start. For someone beginning at 35 with no savings, Fidelity raises that target to 23%. T. Rowe Price puts the number at 28% for a 45-year-old starting from zero.

For high earners, 25%+ is a reasonable minimum savings target. Social Security will replace such a small share of pre-retirement income that the shortfall falls entirely on personal savings. Closing that gap requires combining multiple savings vehicles — not relying on a single 401(k).

Max Out Tax-Advantaged Accounts: The Non-Negotiable First Step

Tax-advantaged accounts are where the government works in your favor — either cutting your tax bill today or shielding your growth from taxes later. Maxing these out every year is the baseline, not the finish line.

Employer-Sponsored Plans: 401(k), 403(b), and 457 Plans

Per IRS Notice 2025-67, the 2026 contribution limits are:

- Under age 50: $24,500 employee elective deferral

- Ages 50–59 and 64+: $32,500 total (standard deferral + $8,000 catch-up)

- Ages 60–63: $35,750 total (enhanced SECURE 2.0 catch-up of $11,250)

- Total plan limit (employer + employee): $72,000

Always contribute at least enough to capture the full employer match first — that's an immediate guaranteed return that no other investment can match.

Important SECURE 2.0 change for 2026: High earners with prior-year W-2 wages of $145,000 or more from the same employer must make catch-up contributions as Roth contributions, not pre-tax. If your employer doesn't offer a Roth 401(k) option, this rule could inadvertently eliminate your catch-up contributions entirely. Confirm your plan's Roth option status with HR if you're near or above that threshold.

Self-Employed and Business Owner Options

Self-employed high earners have access to much higher contribution ceilings:

- SEP-IRA: Employer contributions up to 25% of compensation, with a 2026 maximum of $72,000

- Solo 401(k): Combines employee and employer contributions, also capped at $72,000 — but allows after-tax contributions in some plans

- Cash balance pension plan paired with a 401(k): Can shelter far more than either plan alone — sometimes $100,000+ annually for high earners in their peak years — making it especially valuable for partners in law, medicine, and accounting firms

If you own a business and want to explore whether a cash balance plan makes sense for your situation, Barking Sands Capital evaluates these options as part of a coordinated tax and retirement planning review — not in isolation — using their InteProcess™ methodology.

Advanced Roth Strategies for High Earners

Most high earners can't contribute directly to a Roth IRA. For 2026, the phase-out begins at $242,000 for married filing jointly ($153,000 for single filers), with full ineligibility above $252,000 and $168,000 respectively. Two legal strategies exist to work around this.

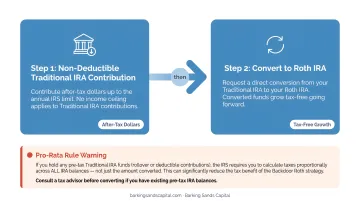

The Backdoor Roth IRA

The backdoor Roth IRA is a two-step process:

- Make a non-deductible contribution to a traditional IRA — up to $7,500 (under 50) or $8,600 (50+) for 2026

- Convert the traditional IRA to a Roth IRA promptly, before any significant earnings accumulate

The conversion is generally a taxable event only on earnings that accumulated between contribution and conversion, so timing matters.

The pro-rata rule warning: If you hold pre-tax dollars in a traditional, SEP, or SIMPLE IRA, the IRS calculates taxes on your conversion proportionally across all your IRA balances — not just the after-tax amount you just contributed. This can create an unexpected tax bill.

IRS Form 8606 tracks non-deductible contributions and calculates the taxable portion. Work with a tax professional before executing if you have existing pre-tax IRA balances.

The Mega Backdoor Roth

The mega backdoor Roth operates on a much larger scale. After maximizing regular 401(k) contributions, some employer plans allow additional after-tax contributions up to the overall 415(c) limit ($72,000 in 2026). Those after-tax dollars can then be converted to Roth, either through an in-plan Roth conversion or a rollover to a Roth IRA.

Not every 401(k) plan supports this strategy. Before attempting it, confirm your plan allows:

- After-tax contributions beyond the standard elective deferral limit

- In-service withdrawals or in-plan Roth conversions

Fidelity outlines the mechanics, but execution requires careful coordination to avoid triggering unexpected tax consequences.

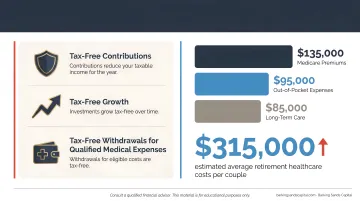

The HSA: A Triple Tax-Free Retirement Account

For high earners enrolled in a high-deductible health plan (HDHP), the HSA is one of the most underutilized tools in retirement planning. The triple tax advantage is rare:

- Contributions are tax-deductible

- Growth is tax-free

- Withdrawals are tax-free for qualified medical expenses

Per IRS Rev. Proc. 2025-19, 2026 contribution limits are:

- Self-only coverage: $4,400

- Family coverage: $8,750

- Age 55+ catch-up: Additional $1,000

The Advanced HSA Strategy

Most people treat the HSA as a medical spending account. The smarter approach: pay current medical expenses out of pocket, and let the HSA grow invested over years or decades. After age 65, you can reimburse yourself for any qualified medical expenses you've paid throughout your life — tax-free, with no time limit on receipts.

HealthView Services' 2026 report projects that a healthy 65-year-old couple retiring in 2026 will face $688,996 in lifetime Medicare premiums alone — rising to $955,411 when adding deductibles, copays, and dental. An HSA that's been growing for 20–30 years can offset a substantial portion of that cost tax-free, making it one of the few accounts specifically sized for what retirement healthcare actually costs.

That said, the strategy has boundaries worth planning around. Once enrolled in Medicare, you can no longer contribute to an HSA. And after age 65, non-medical withdrawals are taxed as ordinary income — similar to a traditional IRA. That makes it worth preserving HSA funds specifically for healthcare, where the tax-free withdrawal benefit is irreplaceable.

Beyond Retirement Accounts: Additional Wealth-Building Strategies

Once all tax-advantaged accounts are maximized, taxable brokerage accounts become the natural next layer. Key advantages:

- No contribution limits

- No early withdrawal penalties

- Flexible access to capital

While there's no upfront tax deduction, disciplined use of index funds, ETFs, and tax-loss harvesting reduces the tax drag considerably. Vanguard research estimates that optimal tax-loss harvesting programs can generate 0.47%–1.27% annual after-tax alpha, depending on the investor's profile. For a high earner managing a seven-figure portfolio, that difference compounds into real money.

Asset location is just as important as account type. High-growth assets — equities, growth ETFs — belong in Roth accounts where gains are never taxed. Income-generating assets like bonds and dividend stocks fit better in traditional tax-deferred accounts.

Tax-efficient index ETFs are the right fit for taxable accounts. Placing assets in the wrong account type can cost thousands in unnecessary taxes each year.

Beyond asset location, two vehicles can extend a high earner's tax strategy further:

- Real estate: Either direct rental property or REITs offer diversification, inflation hedging, and passive income. REITs provide a more accessible entry point without the management demands of direct ownership.

- Non-qualified deferred compensation (NQDC) plans: Available at some larger employers, these allow executives to defer salary or bonuses to a future tax year — potentially retirement, when income may be lower. The critical caveat: NQDC plans are not ERISA-protected. Assets remain subject to employer credit risk and strict Section 409A timing rules. They're most appropriate at financially stable companies.

Managing Taxes and Lifestyle to Maximize What You Keep

Lifestyle Inflation Is a Silent Savings Killer

When income rises, expenses tend to rise with it — often proportionally. The result is a savings rate that stays flat or declines even as earnings climb. The fix is simple but takes deliberate effort: set savings targets before committing to lifestyle upgrades, and automate contributions to retirement and investment accounts so the savings decision never competes with monthly discretionary spending.

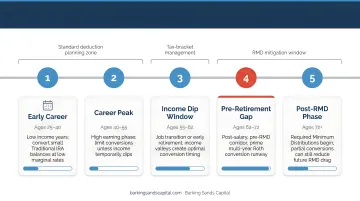

Roth Conversion Windows

Strategic Roth conversions during lower-income years — a gap year, sabbatical, early semi-retirement, or the pre-RMD window before age 73 (or 75 for those born after 1959) — can permanently reduce future required minimum distributions and overall retirement tax exposure.

The core logic:

- Convert traditional IRA or 401(k) balances to Roth when your marginal rate is lower than it will be during peak earning years

- Act before RMDs would otherwise push you into a higher bracket

- Manage bracket thresholds carefully to avoid overshooting into a higher tier — a tax advisor is essential here

Integrated Planning as the Foundation

Retirement, tax, investment, and estate planning are deeply interconnected for high earners. Decisions in one area cascade into the others — Roth conversions affect Medicare surcharges (IRMAA), business owner tax strategies affect retirement plan eligibility, and withdrawal sequencing affects estate outcomes.

At Barking Sands Capital, advisors coordinate these disciplines through their proprietary InteProcess™ — aligning legal, insurance, tax, retirement, and investment planning across accounts and life stages. The goal is a single, coherent strategy rather than siloed decisions pulling in different directions.

Frequently Asked Questions

What is the 50/30/20 rule for high earners?

The 50/30/20 rule allocates 50% of income to needs, 30% to wants, and 20% to savings. For high earners, the savings percentage typically needs to increase — many planners recommend 25% or more toward retirement, adjusted for higher marginal tax rates that compress each bucket's usable share.

What retirement account is best for high income earners?

No single account type is best. High earners typically benefit from a combination: a 401(k) or 403(b), an HSA (if enrolled in an HDHP), a backdoor Roth IRA, and a taxable brokerage account — with self-employed earners adding a SEP-IRA, Solo 401(k), or cash balance plan depending on business structure.

What is Dave Ramsey's 8% rule?

Dave Ramsey's 8% rule refers to his suggested annual withdrawal rate in retirement, based on an assumed average market return of around 11–12%. Most mainstream financial planners consider this aggressive — Morningstar's 2025 research identified 3.9% as the highest safe starting withdrawal rate for a 30-year horizon — making it essential to model your own needs based on projected expenses and longevity.

Can high earners contribute to a Roth IRA?

High earners above the income phase-out thresholds ($242,000–$252,000 married filing jointly in 2026) cannot contribute directly to a Roth IRA. However, they can still access Roth benefits through the backdoor Roth IRA — contributing to a traditional IRA on a non-deductible basis and then converting it to Roth. Pro-rata rules apply if other pre-tax IRA funds exist.

How much should high earners save for retirement?

The general 15% baseline suits average earners with longer timelines and meaningful Social Security support. High earners are typically advised to target at least 25% of gross income, since Social Security replaces a smaller share of their income and standard contribution limits represent a fraction of their salary.

What is a mega backdoor Roth?

A mega backdoor Roth allows high earners to contribute after-tax dollars to a 401(k) beyond the standard pre-tax limit, then convert those funds to Roth — either within the plan or via rollover to a Roth IRA. The total 2026 plan limit is $72,000, but the strategy requires the employer's plan to permit after-tax contributions and in-service withdrawals or in-plan conversions — confirm eligibility with your plan administrator first.