That uncertainty is more common than most people admit. Retirement doesn't just end your working years; it starts an entirely different financial challenge. Drawing down assets strategically, minimizing taxes, coordinating Social Security with Medicare, making sure your money lasts 20 to 30 years — none of that works like the accumulation phase did.

Not everyone needs a financial planner. Some people have straightforward finances and strong planning instincts. But certain situations make professional guidance not just helpful — potentially essential. Here are five signs you may be in that category.

Key Takeaways

- Retirement's distribution phase is fundamentally harder than the accumulation phase — mistakes are costly and difficult to reverse.

- Only 27% of Baby Boomer workers have a written retirement financial strategy.

- The 5 signs you need a planner: no withdrawal strategy, financial complexity, emotional decisions, tax uncertainty, and fragmented planning.

- Look for fiduciary, fee-based advisors with CFP® or ChFC credentials who specialize in retirement.

- A qualified planner coordinates taxes, income, Medicare, long-term care, and estate planning together — not investments alone.

Why Retirement Planning Is More Complex Than You Think

The Shift From Saving to Spending

During your working years, the strategy was relatively linear: save consistently, diversify, stay invested. If you made a mistake — selling too early, missing a contribution window — you had time to recover.

Retirement flips this completely. Now you're drawing from accounts instead of filling them, and the consequences of a poorly timed decision can compound in ways that aren't reversible. Common missteps include:

- A tax error in year one that triggers a higher bracket for years after

- A large withdrawal during a market downturn that locks in losses

- Missing a Roth conversion window before required minimum distributions begin

Each of these shrinks the portfolio you'll depend on for decades — and none of them are easy to undo.

Coordinating Multiple Income Streams

Retirees rarely draw from a single source. According to Federal Reserve data on household economic well-being, most retirees draw from several sources at once:

- 77% receive Social Security

- 57% have a tax-preferred retirement account

- 56% have pension income

- 48% have interest, dividends, or rental income

Each source carries different tax treatment, withdrawal rules, and timing considerations.

Coordinating those streams efficiently requires a plan. Without one, you're likely leaving money on the table or creating unnecessary tax exposure.

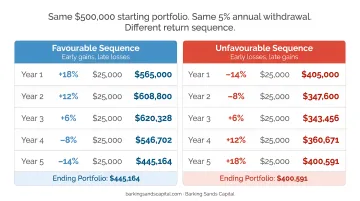

Sequence of Returns Risk

That income coordination problem gets more dangerous when markets move against you. Sequence of returns risk describes what happens when the market drops significantly in your first few retirement years — while you're actively withdrawing. You sell assets at a loss to fund living expenses, which permanently impairs your portfolio's ability to recover, even if the market eventually rebounds.

Morningstar found that nearly 70% of retirement plan failures involved portfolios that had lost value by the end of the fifth retirement year. The math in distribution simply doesn't work the same way as in accumulation — which is exactly why having a withdrawal strategy in place before you retire matters more than most people realize.

5 Signs You Need a Financial Planner for Retirement

Sign #1: You're Within 5-10 Years of Retirement and Still Don't Have a Written Withdrawal Strategy

A withdrawal strategy isn't just "when to retire." It covers:

- Which accounts to draw from first (and in what sequence)

- When to claim Social Security to maximize lifetime benefits

- How to balance short-term income needs against long-term portfolio survival

- How to stay in lower tax brackets during the early retirement window

According to Transamerica Institute's 2025 retirement research, only 27% of Baby Boomer workers have a written financial strategy for retirement — and 24% have no strategy at all. Among Generation X, it's even worse: 29% have no plan.

These are people approaching retirement, not 30-year-olds with decades to adjust. If you've been focused entirely on accumulating and haven't thought through the decumulation side, that gap matters — and it's more common than most people realize.

Sign #2: Your Financial Picture Is More Complex Than a Single Savings Account

"Financial complexity" in retirement planning includes:

- Multiple 401(k)s from former employers that have never been consolidated

- A small business with cash-balance plans or a pending sale

- Rental properties generating income with their own tax treatment

- Stock options, an employer pension, or an inherited IRA

- A spouse with a completely different income and account structure

The more moving parts, the harder it is to optimize without coordination. This complexity often surfaces at tax time — but by then, the decisions for that year are already made and baked in.

A financial planner maps every account, income stream, and asset into a single picture and builds a strategy around the interactions between them. Firms like Barking Sands Capital are specifically structured for this: their proprietary InteProcess™ coordinates legal, insurance, tax, retirement, and financial planning into one unified strategy rather than treating each discipline separately.

For clients with complicated financial pictures, that kind of cross-functional coordination prevents the costly blind spots that come from working with disconnected advisors.

Sign #3: You've Made Emotional Decisions With Your Investments — and Paid for It

Most investors know they shouldn't panic-sell during a downturn or chase hot sectors after a rally. Most do it anyway.

DALBAR's ongoing research tracking actual investor returns versus market returns puts a number on this gap. Over the 20-year period from 2006–2025, the average equity investor earned 9.48% annualized versus 10.23% for the S&P 500 — a seemingly small difference that compounds into a substantial shortfall over a multi-decade retirement.

For retirees actively drawing down assets, emotional selling is especially destructive. When you sell during a downturn to fund living expenses, you lock in losses and permanently remove shares that would have recovered. There's no "wait it out" option when you need income next month.

A financial planner functions as a behavioral counterweight — someone who holds you to the plan when markets get uncomfortable. That's not a soft benefit. Vanguard's Advisor's Alpha research estimates behavioral coaching alone can add 200 or more basis points in net returns, which is often more valuable than any specific investment selection.

Sign #4: You're Uncertain How Taxes Will Work in Retirement

Most retirees underestimate tax complexity in retirement. Here's what's actually in play:

- Required Minimum Distributions (RMDs): Begin at age 73 under current law, increasing to age 75 in 2033 per SECURE Act 2.0. Once they start, they force taxable withdrawals whether you need the money or not.

- Social Security taxation: Up to 50% of benefits become taxable when combined income exceeds $25,000 (single) or $32,000 (married). Up to 85% becomes taxable above $34,000 or $44,000, respectively.

- Medicare IRMAA surcharges: Higher income in retirement triggers surcharges on Medicare premiums. A married couple with income above $212,000 pays $259/month per person for Part B instead of $185 — and the surcharges escalate from there.

- Roth conversion windows: The years between retirement and when RMDs begin often represent a lower-income window ideal for converting pre-tax dollars to Roth accounts at reduced tax rates.

Without a coordinated withdrawal strategy, many retirees end up in higher tax brackets than necessary — or miss Roth conversion opportunities that could have meaningfully reduced their lifetime tax burden. A financial planner designs a strategy that pulls from pre-tax, after-tax, and tax-free accounts in the right proportion each year to manage bracket exposure and avoid triggering unnecessary surcharges.

Sign #5: You Don't Have an Integrated Plan for Social Security, Healthcare, and Estate Planning

Many retirees treat these as separate decisions — Social Security over here, Medicare enrollment over there, a will they haven't updated in a decade. In practice, these decisions are deeply interconnected.

Your Social Security claim date shapes your income, which determines your Medicare costs, which triggers or avoids IRMAA surcharges, which feeds directly into your tax situation and estate planning assumptions. Optimize one piece in isolation and you can create a problem somewhere else without realizing it.

Long-term care adds another layer. The 2025 CareScout/Genworth Cost of Care Survey puts the national median annual cost of a private nursing home room at $129,575. Even a two-year care need can devastate a retirement portfolio that looks adequate on paper when only investment expenses are considered.

People who have savings but no coordinated plan across these domains are especially exposed to blind spots that only become visible when it's too late to easily course-correct. A retirement plan that doesn't connect these pieces isn't really a plan — it's a collection of accounts waiting for something to go wrong.

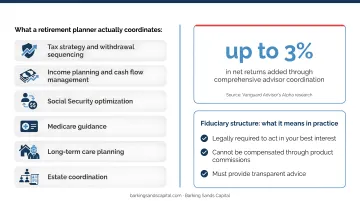

What a Retirement Financial Planner Actually Does

Most people picture a retirement financial planner as someone who manages their portfolio. That's only part of the job. A comprehensive retirement planner coordinates investment management with a full set of interconnected disciplines:

- Tax strategy and withdrawal sequencing

- Income planning and cash flow management

- Social Security optimization

- Medicare guidance

- Long-term care planning

- Estate coordination

Vanguard's Advisor's Alpha research estimates that working with a qualified advisor can add up to 3% in net returns through this kind of comprehensive coordination — with behavioral coaching and tax-efficient withdrawal strategies accounting for the largest share of that value.

The other critical factor is fiduciary structure. A fiduciary financial planner is legally required to act in your best interest, cannot be compensated through product commissions, and must provide transparent advice. For retirees — who are particularly vulnerable to being steered into high-fee or unnecessary products — this distinction has real financial consequences.

Barking Sands Capital operates as a fee-based Registered Investment Advisor. As an RIA, the firm cannot accept commissions on managed accounts, which eliminates the conflicts of interest inherent in commission-based advisory models.

How to Choose the Right Financial Planner for Retirement

Credentials That Matter

Two designations stand out for retirement planning:

- CFP® (Certified Financial Planner): Requires completing a CFP Board-registered education program, a 170-question exam across two three-hour sessions, 6,000 hours of related professional experience, and ongoing ethics requirements. The credential emphasizes holistic financial planning.

- ChFC (Chartered Financial Consultant): Requires eight courses and exams, at least three years of financial planning experience, and adherence to The American College's ethics code. The ChFC specializes in advanced retirement and distribution planning.

Barking Sands Capital's team includes both — JB L'Esperance holds the ChFC designation with deep expertise in retirement analysis and estate planning, and Andrea Cervena holds the CFP® with a focus on tax planning, retirement planning, and estate coordination.

Questions to Ask in Your First Meeting

Before committing to any advisor, ask these directly:

- "Are you a fiduciary at all times?" This means every interaction, not just when recommending products.

- "How are you compensated — fee-only, fee-based, or commission?" Fee-only means no commissions ever; fee-based means primarily fees but may include some commissions. Know the difference before you sign anything.

- "Can you show me a sample retirement income plan?" A qualified planner will walk you through how they integrate income, taxes, Social Security, and estate planning into one cohesive strategy.

Come prepared with more than account balances. Know your spending goals, healthcare expectations, and legacy priorities — and if a planner doesn't ask about those things, that's a signal worth paying attention to.

Frequently Asked Questions

Do I need a financial planner for retirement?

Not everyone does. But if you have multiple income sources, uncertainty about taxes, or no clear withdrawal strategy, the benefit of professional guidance usually outweighs the cost — especially as you shift from saving to drawing down assets over 20 to 30 years.

What is the biggest mistake most people make regarding retirement?

Failing to plan for the distribution phase. Most people focus on accumulating savings, then enter retirement without a strategy for withdrawing money tax-efficiently, claiming Social Security optimally, or making those savings last.

How much do I need to retire on $80,000 a year at 60?

Using Morningstar's current safe withdrawal rate estimate of roughly 3.9% for a 30-year retirement, you'd need approximately $2 million in investable assets. The actual number depends heavily on Social Security income, taxes, healthcare costs, and longevity — variables no single rule of thumb can account for.

What is the $1,000 a month rule for retirees?

It's a simplified guideline: for every $1,000 of monthly income desired, have approximately $240,000 saved (based on a 5% withdrawal rate). It's a useful starting point, but it ignores taxes, inflation, and spending changes that significantly affect how long savings actually last.

What is the difference between a financial planner and a financial advisor for retirement?

"Financial advisor" covers a wide range of professionals with varying scopes. A financial planner — particularly a CFP® — coordinates across your full financial picture: investments, income timing, tax exposure, and estate goals. For retirement specifically, the focus extends beyond investments to income strategy, tax planning, Medicare, and estate coordination.

How do I know if a financial planner is worth the cost?

Measure value through tax savings identified, behavioral mistakes avoided, and planning optimizations — not just investment returns. Vanguard's Advisor's Alpha research estimates comprehensive advice can add up to 3% in annual net returns, with behavioral coaching and tax-efficient withdrawal strategies accounting for the largest portions of that value.