Introduction

Women-owned businesses now account for 14 million firms — 39.1% of all U.S. businesses — employing nearly 12.2 million people and generating $2.7 trillion in revenue. That's not a niche. That's a cornerstone of the American economy.

Yet the financial planning challenges female entrepreneurs face don't match that scale of impact. Managing irregular business income, self-funding retirement without employer-sponsored plans, navigating unequal access to capital, and rebuilding personal savings after career breaks — these pressures compound in ways that standard financial advice rarely addresses.

A proactive, integrated approach is essential. This guide covers the specific financial moves female entrepreneurs should prioritize — from building a solid foundation to retirement planning, tax strategy, and knowing when to bring in professional support.

Key Takeaways

- Female entrepreneurs face compounding challenges: unequal startup capital, a 30% retirement savings gap versus men, and higher loan denial rates

- Separating personal and business finances from day one protects both credit profiles and personal assets

- Self-employed business owners must fund their own retirement accounts — no employer enrollment or matching exists to do it for them

- Tax strategy, business protection insurance, and capital access tend to get deprioritized — until a crisis forces the issue

Unique Financial Challenges Female Entrepreneurs Face

The Startup Capital Disadvantage

According to the National Women's Business Council, men start businesses with nearly twice as much capital as women. The Kauffman Foundation confirms that personal and family savings are the most common startup capital source for new businesses — which means the gender wealth gap doesn't stay in salaried employment. It follows women directly into entrepreneurship.

Less startup capital means thinner emergency cushions, weaker early-stage cash flow, and reduced negotiating leverage with lenders when growth capital is needed later.

The Career Break Penalty

Time away from business for caregiving or family responsibilities interrupts more than income. It interrupts retirement contributions, compounding investment growth, and business credit development — simultaneously.

The gap this creates doesn't stay flat. It widens. Because women statistically outlive men by 5.3 years (81.1 vs. 75.8 years, per 2023 CDC data), every year of missed retirement contributions carries more weight than it would for their male counterparts.

The Capital Access Gap

Even high-performing women-owned businesses face funding barriers that don't correlate with business quality. Federal Reserve Small Business Credit Survey data confirms that women-owned firms are significantly more likely to be denied financing when they apply. The NWBC notes that high-growth women-owned firms exceed growth expectations — yet still face capital access gaps that weaker-performing male-owned businesses don't encounter.

On the venture side, PitchBook's 2025 report shows female-founded companies captured 27.7% of U.S. VC deal value in 2025 — a record high, but still a minority share of a market where their performance consistently justifies more.

The Representation Gap in Financial Services

Only 23.8% of all CFP® professionals are women, according to CFP Board's 2025 year-end data. For female entrepreneurs seeking an advisor who genuinely understands their situation — business ownership, career interruptions, longevity planning — that's a limited pool. Finding a fee-based, client-first advisory team matters more than many entrepreneurs initially realize.

These four challenges rarely appear in isolation. More often, they compound each other — less startup capital leads to tighter cash flow, career breaks widen the retirement gap, and funding barriers slow the growth that would otherwise offset both. Understanding where the gaps exist is the first step toward building a financial plan that accounts for all of them.

Quick reference — the four core challenges:

- Capital shortfall at startup: Women launch with roughly half the capital men do, limiting early resilience

- Career break penalties: Time away from business interrupts retirement savings and credit development simultaneously

- Ongoing funding barriers: Strong business performance doesn't guarantee equal access to growth capital

- Thin advisor representation: Fewer than 1 in 4 CFP® professionals are women, narrowing the pool of advisors with relevant lived experience

Building a Strong Business and Personal Financial Foundation

Establish an Emergency Fund First

Entrepreneurs need a more robust cash cushion than salaried employees. Business income is irregular, especially in the first few years, and a slow quarter can turn into a cash crisis without adequate reserves.

The general recommendation: three to six months of personal essential expenses in a liquid, easily accessible account. If you're planning a family-related career break, aim for the higher end — or beyond it.

One critical distinction: your personal emergency fund and your business operating reserve are not the same account. Combining them creates accounting problems and masks cash flow issues in the business. Keep them separate from the start.

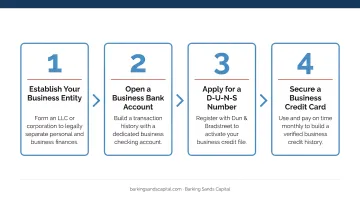

Separate Personal and Business Finances

The foundational steps here are straightforward:

- Open a dedicated business checking account under the business's EIN

- Obtain a business credit card used exclusively for business expenses

- Pay yourself a regular salary or owner's draw to create a clear, consistent boundary between personal and business funds

This separation accomplishes several things at once: cleaner expense tracking, simpler tax filing, and protection of personal assets from business liability. It also sets the stage for building two independent credit profiles — personal and business — which matters enormously when you need favorable lending terms later.

Build and Monitor Business Credit

Business credit builds independently of personal credit. The primary vehicles are vendor trade lines, business credit cards, and consistent on-time payments under the business's EIN.

Practical steps to build business credit:

- Register your business with major business credit bureaus (Dun & Bradstreet, Experian Business, Equifax Business)

- Establish vendor accounts that report payment history

- Pay all business obligations on time — even small ones register

- Monitor both your personal and business credit scores regularly

A well-maintained business credit profile directly improves your terms when you apply for a business loan, line of credit, or equipment financing. Starting before you need capital urgently gives you time to build a strong profile without pressure.

Credit building also pairs naturally with maintaining a living business plan that includes detailed financial projections — not just for funding applications, but as a working reference for quarterly decisions and tracking financial health over time.

Retirement Planning and the Gender Wealth Gap

The Structural Problem for Self-Employed Women

Transamerica research estimates women's retirement accounts are 30% lower than men's. Among self-employed workers specifically, the median household retirement savings sit at just $87,000, only 22% have a written retirement strategy, and 60% are actively saving.

The structural reason: workplace auto-enrollment plans don't exist for the self-employed. No employer contributes on your behalf or auto-enrolls you by default. Female entrepreneurs must build retirement savings entirely through their own deliberate action.

Retirement Account Options for Self-Employed Entrepreneurs

Three primary vehicles are available for self-employed business owners:

| Account Type | 2025 Contribution Limit | Best For |

|---|---|---|

| SEP-IRA | Up to $70,000 (25% of compensation) | Simple setup, high ceiling |

| Solo 401(k) | Up to $70,000 total ($23,500 elective deferral + employer portion) | Higher flexibility, catch-up eligible |

| SIMPLE IRA | Up to $16,500 salary reduction | Small businesses with employees |

Catch-up contributions apply to Solo 401(k) and SIMPLE IRA for those 50 and older ($7,500 and $3,500 respectively). All three offer pre-tax contributions that reduce your current taxable income — especially valuable in high-income years.

Barking Sands Capital also works with clients on cash-balance plans, which allow substantial annual contributions and can be particularly effective for established business owners seeking to accelerate retirement savings in higher-income years.

The Longevity Factor

Women outlive men by more than five years on average. That means a longer drawdown period — more years of retirement to fund. The practical implication: starting earlier matters more, not less.

The integrated planning approach Barking Sands Capital uses through its InteProcess™ — coordinating retirement analysis, tax planning, and investment management together — helps female business owners account for these variables holistically rather than treating retirement as a separate silo. That coordination — across contribution decisions, tax timing, and investment allocation — compounds meaningfully over a retirement horizon that may span three decades or more.

Tax Planning, Business Protection, and Accessing Capital

Tax Planning as a Business Owner Advantage

Female entrepreneurs have tax planning tools that salaried employees don't. Used deliberately, they can significantly reduce taxable income:

- Retirement contributions (SEP-IRA, Solo 401(k)) reduce gross income dollar-for-dollar

- Home office deduction — if you use part of your home exclusively for business, a portion of housing costs qualifies

- Business expense deductions — equipment, software, professional development, and more

- Entity structure — an LLC electing S-corporation status can reduce self-employment taxes by limiting FICA to a reasonable salary rather than total business income (this carries compliance requirements; a CPA review is advisable before making the switch)

The key isn't filing-time optimization. It's year-round coordination between your financial planner and tax advisor, so that retirement contribution timing, entity decisions, and income recognition all work together. Barking Sands Capital's InteProcess™ is built around exactly this kind of cross-discipline coordination, connecting tax strategy, retirement contributions, and entity decisions throughout the year.

Tax efficiency protects income on the way in. Insurance protects what you've already built.

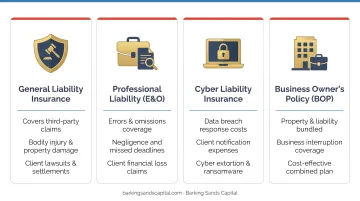

Business Protection Insurance

Insurance is the planning area female entrepreneurs most consistently deprioritize. A health event, disability, or business disruption can expose that gap fast — and at the worst possible time.

The coverage types worth evaluating:

- Personal disability insurance — replaces income if you're unable to work; for a business owner, there's no employer short-term disability to fall back on

- Life insurance — personal coverage to protect dependents and, if the business carries debt, business coverage to protect it

- Key person insurance — covers the business against financial loss if a critical person (including you) becomes unable to work

- Buy-sell agreement funded by life insurance — if you have business partners, this protects all parties if one exits unexpectedly

Barking Sands Capital's protection planning services cover disability and life insurance, evaluated in the context of your full financial picture — income needs, business obligations, and long-term goals together.

Insurance secures what you have. Knowing where to find capital helps you grow it.

Accessing Capital: Beyond the Bank

Traditional bank loans aren't the only path — and for many female entrepreneurs, they're not the most accessible one. Alternatives worth knowing:

- SBA 7(a) loans — up to $5 million with more flexible terms and lower down payments than conventional business loans

- Women's Business Centers — the SBA funded $30 million in WBC grants in 2024; these centers offer coaching, training, and connections to lenders

- NAWBO, SCORE, and WBENC — advocacy, mentorship, certification, and supplier diversity networks that open doors to corporate procurement and capital

- Women-specific grants — limited but real; research programs available in your state and industry

One consistent finding: approval odds improve significantly when you approach lenders with a strong business plan, established business credit, and an existing banking relationship. Building those foundations before capital becomes urgent is what separates funded businesses from ones that wait in line.

When to Work with a Financial Advisor

Signs It's Time to Bring in a Professional

Many female entrepreneurs wait too long. The warning signs that it's time to engage a financial advisor:

- Business is generating consistent revenue but personal finances haven't kept pace

- Personal and business finances are intersecting in complex ways (personal guarantees, owner loans, commingled cash)

- Retirement has been deprioritized for multiple years

- A major life event is approaching: business sale, partnership change, planned career break, or exit planning

The earlier you engage, the more options are available. A business sale, for example, has very different tax implications depending on how the transaction is structured. Those decisions can't be undone after the fact.

What to Look For in an Advisor

For female entrepreneurs specifically, the advisory structure matters as much as the individual advisor. Key criteria:

- Fee-based, independent RIA — this structure removes commission-based conflicts of interest. Barking Sands Capital operates as an RIA and cannot be paid commissions on managed accounts, which is a fundamental difference from product-driven firms

- Comprehensive planning capabilities — tax, retirement, insurance, estate, and investment management coordinated together, not referred out piecemeal

- Direct experience with business owners — understanding irregular income, business equity, and the intersection of personal and business planning

Barking Sands Capital's team includes co-founder Kelly L'Esperance, who grew up in a family-owned small business and brings direct entrepreneurial perspective to client work. CFP® Andrea Cervena's focus areas — tax planning, estate planning, retirement planning, and budgeting — cover the core disciplines female entrepreneurs most often need coordinated at once.

Frequently Asked Questions

What do female entrepreneurs struggle with most?

The most common challenges include unequal access to startup capital, a significant retirement savings gap from the lack of employer-sponsored plans, and irregular early-stage cash flow. These are compounded by historical pay inequity, career break penalties, and the difficulty of separating business growth from personal financial planning.

What are the 5 Ps of finance?

There's no universally agreed-upon framework called the "5 Ps of finance." A practical equivalent for entrepreneurs: the five core areas of personal finance are income, spending, savings, investing, and protection — all of which require deliberate management when you're both the employee and the employer.

How much should a female entrepreneur save for retirement?

Given women's longer average lifespan and the 30% retirement savings gap, the practical answer is: as much as possible, as early as possible. Maxing contributions to a SEP-IRA or Solo 401(k) during high-income years is the most reliable path to closing that gap.

How do I separate personal and business finances as an entrepreneur?

Open a dedicated business bank account under the business's EIN, obtain a business credit card used exclusively for business expenses, and pay yourself a regular salary or owner's draw. That consistent boundary between personal and business money is the foundation everything else builds on.

What types of insurance does a female entrepreneur need?

At minimum: personal disability insurance, life insurance, and general business liability coverage. If the business has partners or key employees, also add key person insurance or a buy-sell agreement funded by life insurance — often the last line of defense against financial collapse during a personal hardship.

How can female entrepreneurs access business funding?

Start with SBA 7(a) loans, women-specific grants, and organizations like NAWBO and SCORE for mentorship and capital connections. Build business credit early, maintain a strong business plan with financial projections, and establish a banking relationship before funding is urgently needed — those three steps significantly improve approval odds.