Those numbers dominate headlines. But they can also mislead. Healthcare costs in retirement aren't a single bill due on Day One — they're recurring, largely predictable expenses that accumulate over decades. Most retirees can manage them with the right structure in place.

The key distinction: some costs are fixed and foreseeable (premiums), while others are variable and timing-dependent (out-of-pocket). Strategic planning — not just saving more — is what separates retirees who manage healthcare costs well from those who don't. This article covers three angles: the decisions that shape your cost structure, the management habits that keep it under control, and the contextual factors most people overlook entirely.

Key Takeaways

- Healthcare costs in retirement are manageable when premiums (predictable) and out-of-pocket costs (variable) are planned for separately

- The biggest mistakes come from underestimating the pre-Medicare coverage gap, choosing the wrong Medicare plan at enrollment, and ignoring long-term care

- HSAs, Medicare plan selection, and income management to avoid IRMAA surcharges offer the highest-impact ways to reduce costs

- Budget annually, not by lifetime totals — healthcare costs in retirement arrive gradually, not all at once

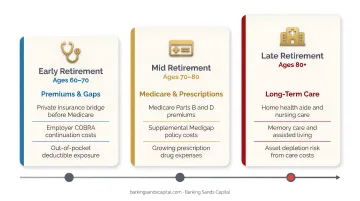

How Healthcare Costs Build Up in Retirement

Healthcare expenses don't arrive as a lump sum. They accumulate gradually — and unevenly — across a 20- to 30-year retirement.

The pattern typically looks like this:

- Early retirement (before 65): Often the most expensive years per capita, due to the gap before Medicare eligibility

- Mid-retirement (65–75): Costs stabilize around Medicare premiums and routine out-of-pocket spending

- Late retirement (75+): Costs spike sharply, particularly for those who require long-term care

Research confirms how steep that late-life escalation can be. According to a study published in PMC, mean U.S. elderly medical spending in the final 12 months of life averaged $59,100, with total spending in the last three years averaging $118,690. A separate analysis found that mean annual non-premium spending at age 90 reached $36,600 — with the 90th percentile hitting $79,900.

Why Healthcare Inflation Makes This Harder Over Time

Static annual averages understate the real risk because healthcare costs inflate faster than general prices. In 2025, the gap was significant:

- All-items CPI: 2.7%

- Medical care prices: 3.2%

- Hospital services: 6.7%

A cost that feels manageable at 65 grows substantially over a 25-year retirement — which means your withdrawal strategy needs to account for healthcare inflation as a distinct line item, not an afterthought tucked into general living expenses.

Key Cost Drivers for Retirement Healthcare

Medicare Plan Selection

The choice between Traditional Medicare with Medigap and Medicare Advantage is the single most controllable cost variable most retirees have. The tradeoff looks like this:

| Traditional Medicare + Medigap | Medicare Advantage | |

|---|---|---|

| Monthly premium | ~$217/month average (Plan G: ~$164/month) | ~$15/month average supplemental |

| Out-of-pocket exposure | Minimal with Medigap | Up to $5,421 in-network average limit |

| Network flexibility | Any Medicare-accepting provider | Network restrictions apply |

| Predictability | High | Variable |

Neither option is universally better. The right choice depends on your health status, preferred providers, and tolerance for out-of-pocket variability. Choosing incorrectly at initial enrollment can be difficult and costly to reverse.

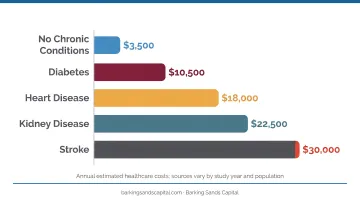

Health Status and Chronic Conditions

Chronic conditions compound retirement healthcare costs in ways that broad averages rarely capture. CDC data from 2023 shows that 93% of U.S. adults age 65+ had at least one chronic condition, and 78.8% had multiple.

The financial gap is stark:

- Adults with 4+ chronic conditions averaged $16,257 in annual healthcare expenditures

- Adults without multiple treated conditions averaged $2,367

People managing heart disease, diabetes, or other ongoing diagnoses face materially higher lifetime exposure — which makes plan selection and out-of-pocket reserves even more important.

Retirement Timing and the Pre-Medicare Gap

Retiring before 65 creates a coverage gap that can derail an otherwise solid retirement income plan. The three main options are COBRA, ACA marketplace plans, or a spouse's employer coverage.

COBRA is often the most expensive route — employer-sponsored family coverage averaged $26,993 annually in 2025, with employees paying an average of $6,850 of that. ACA marketplace premiums can run up to three times higher for older applicants than younger ones. Either way, gap-year healthcare costs need to be modeled explicitly in any early retirement income plan.

Cost-Reduction Strategies for Retirement Healthcare

Strategies differ depending on when they're applied — some depend on decisions made before retirement, others on how retirement is actively managed, and some on broader contextual factors like geography and income structure.

Strategies That Change the Decisions

Choose Medicare coverage intentionally, not by default. The initial enrollment decision carries long-term consequences. The tradeoff between Traditional Medicare + Medigap and Medicare Advantage isn't about which is cheaper on paper — it's about which fits your health status, provider preferences, and risk tolerance. Getting this wrong at 65 can mean years of higher costs or disrupted provider access. Curtis Hewitt, an advisor at Barking Sands Capital who specializes in Medicare Planning and Long-Term Care, works with clients to navigate these enrollment decisions before they become locked in.

Maximize HSA contributions before Medicare enrollment. HSAs offer a rare triple tax advantage: pre-tax contributions, tax-deferred growth, and tax-free withdrawals for qualified medical expenses. The optimal strategy is to contribute the maximum during working years and invest — rather than spend — the balance for long-term growth.

2025 contribution limits:

- Self-only coverage: $4,300

- Family coverage: $8,550

- Age 55+ catch-up: $1,000 additional

In retirement, HSA funds can be used tax-free to pay Medicare Part B premiums, deductibles, and most out-of-pocket costs. (Note: Medigap premiums are not qualified HSA expenses.)

Purchase long-term care insurance during the optimal window. According to HHS research, 70% of adults who survive to age 65 will develop severe long-term services and support needs before death. A private nursing home room now costs a national median of $116,800 per year, with assisted living averaging around $6,200 per month.

The 55–65 window generally offers the best balance between affordability and insurability. AARP estimates that a 55-year-old man pays roughly $2,075 annually for a policy with a 3% inflation rider — that figure rises to $3,135 at age 65.

Those with substantial assets may evaluate self-insuring. For most people, a standalone LTC policy or hybrid life/LTC product deserves serious analysis before that window closes.

Strategies That Change How Retirement Is Managed

Separate your premium budget from your out-of-pocket reserve. Premiums — Medicare Parts B and D, plus any supplemental coverage — are stable enough to include as a line item in monthly income planning. Out-of-pocket costs should be funded from a separate liquid reserve or HSA balance. Combining both into a single "healthcare bucket" makes it harder to see which costs are manageable and which require a buffer.

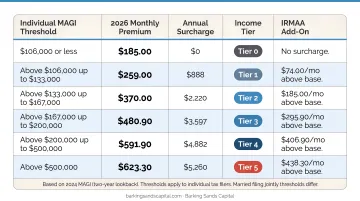

Manage income to avoid IRMAA surcharges. Medicare Part B and Part D premiums increase significantly for higher-income beneficiaries through IRMAA (Income-Related Monthly Adjustment Amount), calculated from income two years prior. In 2026, surcharges begin above $109,000 in individual MAGI or $218,000 for couples. The jumps are steep:

| 2026 Individual MAGI | Part B Surcharge | Total Part B Premium |

|---|---|---|

| ≤ $109,000 | $0 | $202.90 |

| $109,001–$137,000 | $81.20 | $284.10 |

| $137,001–$171,000 | $202.90 | $405.80 |

| $171,001–$205,000 | $324.60 | $527.50 |

| $205,001–$499,999 | $406.70 | $609.60 |

| ≥ $500,000 | $487.00 | $689.90 |

Strategic timing of Roth conversions, IRA distributions, and capital gains realizations can keep income below IRMAA thresholds — avoiding surcharges that add hundreds of dollars per month. Barking Sands Capital's InteProcess™ integrates IRMAA planning directly with tax and retirement income coordination.

Re-evaluate Medicare coverage annually during open enrollment. Medicare plan costs, formularies, and networks change every year. Staying in the same plan by default can mean paying more or losing access to preferred providers or prescriptions. Despite this, KFF found that 69% of Medicare beneficiaries did not compare plans during open enrollment. Open enrollment runs October 15 through December 7 — a brief window worth using every year.

Strategies That Change the Context Around Retirement Healthcare

Time Social Security to protect income and coverage continuity. Many pre-retirees claim Social Security at 62 to help bridge healthcare costs before Medicare. But delaying to age 70 increases monthly benefits permanently — and those higher future benefits can fund healthcare costs for decades. Funding the gap years through other means often pays off substantially over a long retirement.

Social Security timing also interacts with IRMAA. Income from Social Security affects MAGI calculations, which means claiming decisions and Medicare premium levels should be modeled together.

Use Roth conversions to create tax-efficient healthcare funding. Qualified Roth IRA and Roth 401(k) withdrawals are excluded from gross income and don't count toward IRMAA thresholds or ACA subsidy phase-outs. Converting portions of traditional retirement accounts to Roth during lower-income years — typically the early retirement window before Required Minimum Distributions begin — creates a tax-free pool of assets that can pay healthcare costs without inflating taxable income.

The timing matters: conversions done in the wrong year can push income into a higher IRMAA bracket, costing more in premiums than the tax savings are worth. Barking Sands Capital's InteProcess™ aligns conversion timing with Medicare premium planning to avoid that tradeoff.

Factor geography into the retirement healthcare equation. Where you retire affects healthcare costs beyond just premiums. Plan availability varies dramatically: beneficiaries in Oakland County, Michigan had access to 75 Medicare Advantage plans in 2025. In Minnesota, plan availability actually declined in 2026 — the state is among 13 where some counties have no Medicare Advantage plans available at all, and UCare exited most of the market.

Retirees evaluating relocation should analyze healthcare cost differences by geography — including Medigap rating rules, plan availability, and provider network access — alongside broader cost-of-living factors. Barking Sands Capital serves clients across both Michigan and Minnesota, with direct familiarity with how plan landscapes differ between the two states built into their planning approach.

Conclusion

Managing healthcare costs in retirement comes down to three things: understanding where costs originate — premiums versus out-of-pocket, routine versus late-life catastrophic — making informed decisions early, and structuring income to avoid unnecessary surcharges.

The retirees who handle this best treat healthcare as a planning exercise. That means integrating Medicare decisions with tax strategy, Social Security timing, HSA management, and long-term care planning together — each decision reinforcing the others rather than working in isolation.

That kind of coordination is central to how Barking Sands Capital works. Through the proprietary InteProcess™, the team connects Medicare decisions, IRMAA planning, Roth conversions, and long-term care strategies into a unified retirement income plan — with Curtis Hewitt providing specialized Medicare and long-term care guidance alongside the broader advisory team. If you're ready to get ahead of healthcare costs in retirement, reach out to schedule a consultation.

Frequently Asked Questions

How much should I have saved for healthcare in retirement?

Fidelity's 2025 estimate puts the figure at $172,500 for an individual retiring at 65. EBRI's higher-sensitivity scenario reaches $469,000 for couples with high prescription drug costs. Your health status, Medicare plan choice, retirement age, and whether long-term care is included all shift that number — individual modeling matters more than any single benchmark.

What is the biggest expense in retirement?

Healthcare typically ranks among the top two or three retirement expenses alongside housing. Its share of the budget tends to grow over time as other spending (travel, clothing) decreases, while medical costs increase with age.

When should I enroll in Medicare?

The Initial Enrollment Period opens three months before you turn 65 and closes three months after — a seven-month window total. Missing it triggers a permanent 10% Part B penalty for each full 12-month period you could have enrolled but didn't. If you're still on employer coverage at 65, a Special Enrollment Period applies.

Does Medicare cover all my healthcare costs in retirement?

No. Medicare does not cover most dental, vision, hearing, or long-term care. Out-of-pocket costs from deductibles, coinsurance, and uncovered services can still be substantial, which is why Medigap or Medicare Advantage supplemental coverage warrants careful evaluation.

What is long-term care insurance and do I need it?

LTC insurance covers nursing home, assisted living, and in-home care costs that Medicare doesn't — expenses that can exceed $116,800 per year for a private nursing home room. Whether you need it depends on your assets, health, family support, and risk tolerance. Evaluating the decision between ages 55 and 65 gives you the most options before premiums climb.

How does a Health Savings Account (HSA) help with retirement healthcare costs?

HSAs offer triple tax advantages — pre-tax contributions, tax-deferred growth, and tax-free withdrawals for qualified medical expenses, including Medicare Part B premiums. Investing (rather than spending) HSA funds during your working years builds a dedicated, tax-free reserve for retirement healthcare costs. This benefit is available only to those enrolled in an eligible high-deductible health plan.