A qualified charitable distribution (QCD) eliminates that gap entirely. By directing IRA funds straight to a charity — before the money ever lands in your account — the distribution never enters your taxable income in the first place. For retirees already near a Medicare IRMAA threshold, the savings can exceed the amount donated.

This article covers how QCDs and RMDs differ mechanically, why that difference matters for taxes, Medicare premiums, and Social Security, and exactly how to execute a QCD without disqualifying it.

Key Takeaways

- A QCD transfers IRA funds directly to charity and is excluded from taxable income — an RMD is taxed first, then donated

- QCDs count toward your RMD requirement, up to $108,000 per person in 2025 and $111,000 in 2026

- Because QCDs are excluded from MAGI, they can reduce or eliminate costly IRMAA Medicare surcharges

- Retirees who take the standard deduction get zero federal tax benefit from cash donations — but full benefit from a QCD

- The funds must go directly from your IRA custodian to the charity — receiving them personally first disqualifies the QCD

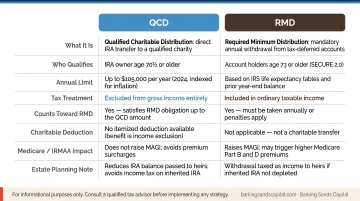

QCD vs RMD: Quick Comparison

Here's how the two strategies stack up across the factors that matter most for tax planning.

| Feature | RMD (then donate) | QCD |

|---|---|---|

| Who it applies to | IRA owners at RMD age (73 or 75) | IRA owners age 70½ or older |

| Tax treatment | Fully taxable as ordinary income | Excluded from gross income |

| Effect on MAGI | Increases MAGI | No effect on MAGI |

| Satisfies RMD? | Yes | Yes, up to annual limit |

| Annual dollar limit | None (RMD amount is fixed) | $108,000/person (2025); $111,000 (2026) |

| Eligible accounts | Traditional IRA, 401(k), others | Traditional IRA only (not ongoing SEP/SIMPLE) |

| Eligible recipients | Any qualified charity | Direct 501(c)(3) charities only — no donor-advised funds |

What Are RMDs and QCDs?

The RMD: Required, Taxable, and Cascading

Under SECURE 2.0, the RMD starting age is 73 for those born 1951–1959 and 75 for those born 1960 or later. Each year, IRS Publication 590-B requires you to divide your prior year-end IRA balance by a life-expectancy divisor from IRS tables — and distribute at least that amount.

The full RMD lands in your gross income as ordinary income. That income triggers a cascade of downstream effects:

- MAGI increases, which the Social Security Administration uses (with a two-year lookback) to calculate IRMAA surcharges

- Social Security benefits become more taxable — up to 85% of benefits are taxable above $34,000 (single) or $44,000 (joint) in combined income

- Effective tax bracket can rise even if the RMD itself falls in a "lower" bracket

Writing a charity check afterward doesn't undo any of this. The RMD already raised your MAGI — the damage is done before the donation clears.

That's exactly the problem a QCD solves.

The QCD: Excluded Before It Starts

A QCD is a direct transfer from a traditional IRA to a qualifying 501(c)(3) charity, available to IRA owners aged 70½ or older — measured at the time of distribution, not just by year-end.

Under 26 USC §408(d)(8), the distributed amount is not includible in gross income. It never appears as income. No deduction needed, because there's no income to deduct against.

Not every account qualifies. Here's how the common account types break down:

- Traditional IRAs: Eligible

- Ongoing SEP or SIMPLE IRAs: Not eligible

- Roth IRAs: Can make QCDs, but since Roth distributions are already tax-free, there's generally no benefit

- 401(k)s: Not directly eligible — though rolling one into a traditional IRA first opens the door

The MAGI and Medicare Connection

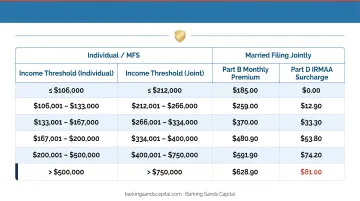

IRMAA — the Income-Related Monthly Adjustment Amount — is the surcharge Medicare adds to Part B and Part D premiums for higher-income retirees. SSA calculates it using MAGI from two years prior, meaning your 2023 income determines your 2025 premiums.

2025 IRMAA Thresholds (Based on 2023 Income)

| 2023 MAGI (Single) | 2023 MAGI (Married Filing Jointly) | 2025 Part B Premium | Part D IRMAA |

|---|---|---|---|

| ≤ $106,000 | ≤ $212,000 | $185.00/mo | $0 |

| $106,001–$133,000 | $212,001–$266,000 | $259.00/mo | $13.70/mo |

| $133,001–$167,000 | $266,001–$334,000 | $370.00/mo | $35.30/mo |

| $167,001–$200,000 | $334,001–$400,000 | $480.90/mo | $57.00/mo |

| $200,001–$499,999 | $400,001–$749,999 | $591.90/mo | $78.60/mo |

Source: CMS 2025 Medicare Parts A & B Premiums

Those thresholds can be deceptively easy to cross. A married couple sitting just under the $212,000 threshold who takes a $20,000 RMD moves into the first IRMAA tier — adding $74/month per person to Part B premiums, or roughly $1,776/year per couple, plus Part D surcharges. A QCD of the same amount keeps MAGI unchanged, and that premium increase never triggers.

QCD vs RMD: Which Strategy Saves You More?

The Standard Deduction Reality

Only about 9.5% of all tax returns itemize deductions, according to IRS Tax Year 2022 data. For 2025, the standard deduction is $31,500 for married filing jointly (plus $1,600 per spouse aged 65 or older, bringing it to $34,700 for a couple where both spouses are 65+).

Most retirees never itemize. A cash charitable contribution in that situation produces zero federal tax benefit. The donation is made with after-tax dollars — period.

A QCD of the same amount fully excludes the distribution from income, regardless of whether you itemize. That's the core advantage for the majority of retirees.

The Illustrative Math

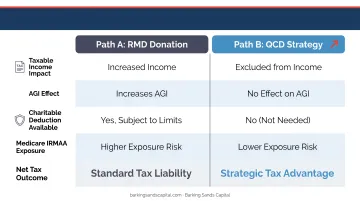

Consider a married couple where one spouse has a $40,000 RMD and plans to donate $20,000 of it to charity. Their MAGI before the RMD sits at $195,000.

Path A — Take RMD, donate cash:

- $40,000 RMD added to income → MAGI rises to $235,000

- Crosses the third IRMAA tier for 2025 premiums (based on 2023 income)

- Cash donation: no deduction if they take the standard deduction

- Net effect: full $40,000 taxed, MAGI elevated

Path B — Direct $20,000 as a QCD, take $20,000 as taxable RMD:

- Only $20,000 added to MAGI → MAGI rises to $215,000

- Stays in the first IRMAA tier instead of the third

- The $20,000 charitable gift costs nothing in taxes

The QCD saves on the charitable amount and keeps the couple's overall MAGI lower, which has downstream effects on Medicare premiums and Social Security taxability.

Who Benefits Most

- Retirees whose pre-RMD MAGI sits near an IRMAA bracket threshold

- Those with larger IRAs generating RMDs above their spending needs

- Retirees who take the standard deduction (the majority)

- Anyone whose RMD would push Social Security benefits into higher taxable territory

When the RMD-Then-Donate Approach Is Comparable

If a retiree already itemizes — due to substantial mortgage interest or high state income taxes — an itemized charitable deduction partially offsets the RMD income. Even in that case, the QCD still holds an edge, because it reduces MAGI directly rather than just trimming taxable income after the fact.

How to Execute a QCD the Right Way

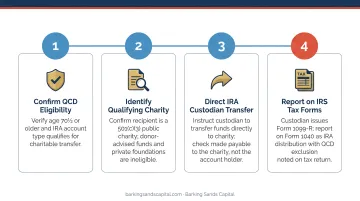

Step 1 — Confirm Eligibility

Three conditions must all be true:

- You are at least 70½ at the time of distribution (not just by year-end)

- The account is a traditional IRA (not a 401(k), Roth IRA, or ongoing SEP/SIMPLE)

- The receiving organization is a direct 501(c)(3) public charity — donor-advised funds and private foundations do not qualify

Step 2 — Request the Direct Transfer

Contact your IRA custodian and request a QCD. The check must be made payable to the charity, not to you. Many custodians can also wire funds directly to the charity.

If you receive the funds personally and then donate — even the same day — the distribution is taxable. There are no exceptions to this rule.

Step 3 — Time It With Your RMD

QCDs done early in the year can satisfy the RMD before the custodian processes an automatic year-end distribution. The IRS confirms a QCD counts toward the RMD requirement. All QCDs must be completed by December 31 to count for that tax year.

If you take both a QCD and a regular distribution in the same year, plan carefully with your advisor to ensure the amounts are coordinated correctly.

Step 4 — Handle Reporting Correctly

Your IRA custodian will issue a Form 1099-R showing the full distribution amount — including the QCD portion. The 1099-R does not automatically separate the QCD.

On your Form 1040:

- Enter the total distribution on Line 4a

- If the entire amount was a QCD, enter $0 on Line 4b

- If only part was a QCD, enter the taxable portion on Line 4b and write "QCD" next to it

Retain the charity's written acknowledgment — the same documentation required for a charitable deduction. Starting with 2025 Forms 1099-R, the IRS added Code Y specifically for QCDs, though custodian reporting practices vary.

Getting the execution and reporting right matters as much as the strategy itself. Barking Sands Capital coordinates tax and retirement planning together, so QCD distributions are properly structured and fit within your broader retirement income plan.

Conclusion

For retirees who are already donating to charity, the QCD is almost always the more tax-efficient path than taking an RMD and writing a check. The gap widens considerably for anyone approaching an IRMAA threshold — where a single $10,000–$20,000 QCD can prevent a Medicare surcharge that costs more annually than the donation itself.

The right approach depends on your specific income picture: your MAGI before RMDs, whether you itemize, and how close you sit to an IRMAA bracket. That coordination is worth getting right before December 31 — the window to act closes with the tax year.

If working through those variables feels like a lot to untangle, that's where professional guidance earns its keep. The advisors at Barking Sands Capital work with retirees across Minnesota and Michigan on exactly this kind of coordination — aligning RMD strategy, IRMAA planning, and charitable giving into a cohesive retirement income plan. Reach out at 952-500-8854 or jb@barkingsandscapital.com to discuss whether a QCD makes sense for your situation this year.

Frequently Asked Questions

Do QCDs count toward MAGI or IRMAA?

No. A properly executed QCD is excluded from gross income under federal law, which means it is not included in the AGI component SSA uses to calculate IRMAA.

What are common QCD mistakes to avoid?

The most frequent errors: receiving funds personally before donating (automatically disqualifies the QCD), sending the gift to a donor-advised fund or private foundation, making the QCD from an ineligible account like a Roth IRA or 401(k), and failing to obtain written acknowledgment from the charity.

What is the QCD limit per person in 2026?

The IRS has confirmed the per-person QCD limit is $111,000 for 2026, up from $108,000 in 2025. The limit is now indexed for inflation. Married couples can each contribute up to the individual limit from their respective IRAs — not a combined limit.

Can a QCD satisfy my entire RMD?

Yes, a QCD can satisfy all or part of your RMD up to the annual limit. If your RMD exceeds the QCD limit, the remaining balance must still be taken as a taxable distribution.

Can I make a QCD from a 401(k) or Roth IRA?

QCDs are only available from traditional IRAs. A 401(k) isn't directly eligible, but rolling it into a traditional IRA first enables the strategy. Roth distributions are already tax-free, so a QCD from a Roth provides no tax benefit.

What charities qualify to receive a QCD?

Eligible recipients must be qualified 501(c)(3) public charities. Donor-advised funds, supporting organizations, and private foundations do not qualify. The transfer must go directly to an operating charity — not to a fund that then distributes on your behalf.