What makes retirement at 55 genuinely complex is that two people with identical portfolio balances can end up in completely different financial positions depending on their withdrawal sequence, healthcare strategy, and whether they've built bridge income sources. According to EBRI's 2026 Retirement Confidence Survey, 29% of retirees actually retired before age 60 — yet only 12% of workers expected to do so. Planning for this outcome matters more than most people realize.

This guide walks through exactly what you need: the required savings targets, account access rules, healthcare bridge strategies, tax sequencing, and common mistakes that derail early retirement plans.

Key Takeaways

- Retiring at 55 typically requires 25–33x your annual expenses — bridge income from rentals or part-time work can lower that target

- The Rule of 55 allows penalty-free 401(k) withdrawals from your current employer's plan if you separate at 55 or older

- Healthcare is your largest gap — Medicare doesn't start until 65, requiring a decade of private coverage

- Delaying Social Security past 62 permanently increases lifetime benefits — a key advantage if you have other income sources

- Tax diversification across traditional, Roth, and taxable accounts is essential for funding a 30+ year retirement

How to Plan for Retirement at 55: Step-by-Step

Step 1: Assess Your Current Financial Position

Start with a complete inventory of every asset:

- 401(k)s and IRAs (note which employer plans are tied to your current job)

- Taxable brokerage accounts

- Real estate equity and rental income potential

- Pension benefits and any deferred compensation

- HSA balances

Pay close attention to account accessibility. The Rule of 55 only applies to your current employer's 401(k) if you separate from service at 55 or older. Previous employer 401(k)s and IRAs remain subject to the 10% early withdrawal penalty until age 59½, unless you use a 72(t) substantially equal periodic payment arrangement.

Next, build a realistic retirement spending estimate. Some costs drop when you stop working — commuting, professional clothing, payroll taxes. Healthcare and discretionary spending typically rise, especially early on. Research consistently shows a "retirement spending smile": real spending dips in the middle years, then climbs again due to health costs. Plan for a 30-year horizon, not 20.

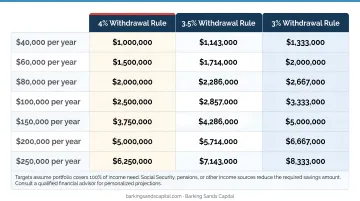

Step 2: Calculate Your Retirement Number

Two methods dominate retirement planning:

| Annual Spending | 4% Rule (25x) | 3.5% Rule (29x) | 3% Rule (33x) |

|---|---|---|---|

| $60,000 | $1,500,000 | $1,740,000 | $2,000,000 |

| $80,000 | $2,000,000 | $2,320,000 | $2,667,000 |

| $100,000 | $2,500,000 | $2,900,000 | $3,333,000 |

| $120,000 | $3,000,000 | $3,480,000 | $4,000,000 |

These figures assume no bridge income.

The 4% rule was built for roughly 30-year retirements. Morningstar's 2025 research found a 3.9% starting rate for 30-year horizons and just 3.3% for 40-year horizons. At 55, you're likely planning for 35–40 years — which means the conservative end of that range is the more appropriate starting point.

Bridge income changes the math substantially. If part-time consulting, rental income, or a pension covers $40,000 per year of your $100,000 spending target, your portfolio only needs to replace $60,000 — reducing the required nest egg by roughly $800,000 to $1,000,000 depending on your withdrawal rate.

Step 3: Maximize Savings and Catch-Up Contributions Before Retirement

The years immediately before retirement are your highest-leverage savings window. Current 2025 IRS limits:

| Account | Standard Limit | Catch-Up (Age 50+) | Total |

|---|---|---|---|

| 401(k) | $23,500 | $7,500 | $31,000 |

| IRA (Traditional or Roth) | $7,000 | $1,000 | $8,000 |

| HSA (Self-Only) | $4,300 | $1,000 (age 55+) | $5,300 |

| HSA (Family) | $8,550 | $1,000 (age 55+) | $9,550 |

The HSA deserves special attention for anyone planning an early exit. It's triple-tax-advantaged: contributions are pre-tax, growth is tax-free, and qualified medical withdrawals are tax-free. For a 55-year-old facing a decade without Medicare, a well-funded HSA is one of the most valuable assets in the retirement toolkit.

Worth noting: the HSA catch-up kicks in at 55 — not 50 like 401(k) and IRA catch-ups.

Step 4: Choose Your Account Withdrawal Sequence

The general tax-smart sequence runs:

- Taxable brokerage accounts first — taxed at capital gains rates (often 0–15%), no RMDs, most flexible

- Traditional tax-deferred accounts (401k/IRA) — ordinary income rates; delay to manage brackets

- Roth accounts last — tax-free growth, no RMDs, preserve as long as possible

The Rule of 55 is your most important early access tool. Per IRS guidance, if you separate from your employer in or after the calendar year you turn 55, you can take penalty-free withdrawals from that employer's 401(k). This does not apply to:

- Previous employers' 401(k) plans

- IRAs of any type

- Plans where you separated before the year you turned 55

For those accounts, you'll need to wait until 59½ or set up a 72(t) distribution plan — a more complex arrangement requiring substantially equal periodic payments that must continue for the longer of 5 years or until age 59½.

Step 5: Build a Comprehensive Written Retirement Plan

Retiring at 55 means coordinating more moving parts than a standard retirement plan. That plan needs to cover:

- Investment management — asset allocation across account types

- Income sequencing — which accounts to draw from, in what order, in what amounts

- Healthcare coverage — year-by-year coverage plan from 55 to 65

- Tax strategy — Roth conversions, bracket management, ACA subsidy preservation

- Social Security timing — claim at 62, FRA, or 70 based on health and cash flow

- Estate planning — beneficiary designations, trust structures, asset protection

Each of these areas affects the others in ways that aren't always obvious. A Roth conversion that pushes your MAGI above 400% of the federal poverty level eliminates ACA premium subsidies. Social Security timing affects how long your portfolio must sustain withdrawals. An estate plan that ignores RMDs on inherited IRAs can create unexpected tax exposure for heirs.

This is where an independent, fee-based financial planner earns their value. Barking Sands Capital's InteProcess™ was built specifically for this kind of integrated planning — coordinating legal, insurance, tax, retirement, and investment decisions so a move that helps in one area doesn't quietly undercut another.

How Much Money Do You Actually Need to Retire at 55?

The Inflation Problem Early Retirees Can't Ignore

Static spending budgets don't survive a 30-year retirement. Using historical CPI data from the Minneapolis Federal Reserve, prices roughly doubled over the 30-year period from 1995 to 2025 — approximately 2.5% annualized.

What that means in practical terms:

| Monthly Budget Today | After 20 Years at 3% | After 25 Years at 3% |

|---|---|---|

| $5,000 | $9,030 | $10,470 |

| $8,000 | $14,449 | $16,751 |

| $10,000 | $18,061 | $20,938 |

Someone retiring at 55 with an $8,000 monthly budget needs to plan for a spending level approaching $17,000/month in today's dollars by their late 70s. That's not a worst case — it's what consistent 3% inflation looks like over time.

Sequence-of-Returns Risk

Inflation erodes purchasing power gradually — but poor market timing can crater a portfolio in a matter of months. Early retirement amplifies this threat in a specific way: withdrawals during a downturn lock in losses before the portfolio can recover. A 30% drop in year two of retirement is far more destructive than the same drop in year 20.

The practical defense comes down to two habits:

- Keep 1–3 years of living expenses in cash or near-cash reserves at retirement, so you're never forced to sell equities at a loss

- Avoid resuming equity draws during a down market — let the portfolio recover first, then rebalance

Bridging the Gap: Income and Healthcare Before Traditional Benefits Begin

Healthcare Coverage Before Medicare at 65

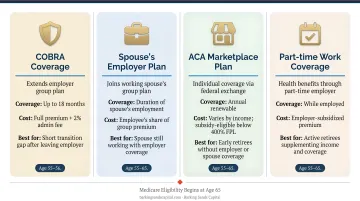

This is the planning gap most people underestimate. Your main options:

- COBRA — extends your prior employer's plan for up to 18 months, but you pay the full premium (up to 102% of plan cost). The 2025 average annual employer-sponsored premium was $9,325 for single coverage and $26,993 for family coverage — and COBRA means paying that yourself.

- ACA Marketplace plans — average 2026 premiums run $741/month before subsidies, but income-based premium tax credits can reduce that to around $96/month for eligible enrollees. Managing your MAGI carefully (avoiding unnecessary Roth conversions that spike income) preserves these subsidies.

- Spouse's employer plan — often the most cost-effective option if available

- Part-time work with benefits — some retirees take limited consulting roles specifically to maintain group coverage

Long-term care insurance is worth serious consideration at 55. HHS estimates that 70% of adults who survive to age 65 will develop significant long-term care needs, and the 2025 national median cost reached $6,200/month ($74,400 annually). Premiums are generally lower at 55 than at 65 — though total lifetime premium cost depends on the policy structure and how long you hold it. Curtis Hewitt, an advisor at Barking Sands Capital who specializes in Medicare and long-term care planning, works with clients navigating exactly this coverage gap.

Sorting out coverage is only half the equation. The other half is deciding when to turn on guaranteed income — and that decision carries real dollar consequences.

Social Security Timing Decisions

The maximum 2026 monthly Social Security benefit illustrates the stakes:

- Claim at 62: $2,969/month (a permanent 30% reduction from FRA for those born in 1960 or later)

- Claim at FRA (67): $4,152/month

- Claim at 70: $5,108/month

For an early retiree with sufficient bridge income, delaying Social Security while drawing down taxable accounts often produces better lifetime income — especially for those in good health with above-average life expectancy. The break-even analysis is personal: it depends on health, discount rate assumptions, and what other income you're drawing. A financial planner can model different claiming scenarios based on your specific health and income picture.

Income Bridge Strategies

If delaying Social Security makes sense for you, you'll need reliable income to cover the years before benefits begin. Common tools for funding the 55-to-62 gap:

- Taxable brokerage withdrawals — flexible, capital gains rates, no age restrictions

- Roth IRA contributions (not earnings) — accessible any time without penalty

- Fixed-index annuities — provide guaranteed income, can be structured for specific time periods

- Part-time or consulting work — generates income and can help manage ACA subsidy eligibility

Mixing sources is usually better than relying on one. It gives you flexibility to control taxable income year-to-year, which directly affects your ACA premium subsidies during the pre-Medicare years.

Tax-Smart Strategies for Retiring at 55

The Roth Conversion Window

The years between 55 and 62 are often the lowest-income period of a retiree's financial life — before Social Security starts and before Required Minimum Distributions (RMDs) force taxable withdrawals. This window is prime for Roth conversions: moving money from traditional IRA or 401(k) accounts into a Roth at a lower tax rate.

Two important caveats:

- The 5-year rule applies separately to each conversion for purposes of avoiding the 10% penalty before 59½ — get this timing right

- MAGI management matters — conversions that push income above ACA subsidy thresholds can cost thousands in lost premium tax credits

Tax Bracket Management

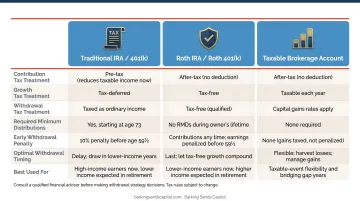

Having assets across three account types gives you income control year-to-year:

| Account Type | Tax Treatment | Best Used When |

|---|---|---|

| Taxable brokerage | Capital gains rates | Early retirement, low-income years |

| Traditional IRA/401(k) | Ordinary income | Spread withdrawals to fill lower brackets |

| Roth IRA | Tax-free | Later retirement, high-income years |

Drawing from taxable accounts first in years with low income preserves tax-deferred and Roth balances for when you need them most.

The RMD Problem

If you retire at 55 with a large traditional IRA or 401(k) and don't take any withdrawals, RMDs beginning at age 73 can force large taxable distributions into higher brackets — potentially pushing $50,000+ per year of income you didn't need or want.

Strategic conversions between 55 and 72 can reduce this future liability. Effective mitigation typically involves:

- Converting enough each year to fill the top of your current bracket without crossing into the next

- Targeting years when income is lowest (before Social Security, before part-time work ends)

- Modeling projected RMD amounts at 73 to size conversions against your future bracket exposure

Common Mistakes to Avoid When Planning Retirement at 55

Most retirement planning errors at 55 aren't about missing deadlines — they're about assumptions that looked reasonable at the time. These four patterns show up repeatedly and are worth checking against your own plan.

- Many retirees budget based on current health, ignoring rising premiums, chronic conditions, and long-term care. The 55–65 gap before Medicare is where healthcare costs hit hardest.

- $6,000/month today requires substantially more purchasing power in 15–20 years. Every plan needs an annual inflation assumption built in — treating current spending as fixed is a quiet budget killer.

- Pulling from an IRA before 59½ without a qualifying exception triggers a 10% penalty plus ordinary income tax. The Rule of 55 only covers your current employer's plan, so don't assume it applies to every account you hold.

- Assuming markets deliver a consistent return — or that one withdrawal strategy works in all conditions — leaves the plan fragile. Spreading income across multiple sources builds real resilience against sequence-of-returns risk and policy changes.

Conclusion

A retirement at 55 that actually works comes down to three integrated factors: a portfolio large enough — or supplemented by bridge income — to sustain 35+ years of withdrawals; a withdrawal sequence that avoids unnecessary penalties and stays within your target tax brackets; and a healthcare plan that closes the gap before Medicare kicks in.

The challenge is that these factors interact in non-obvious ways. For example:

- Roth conversions affect your ACA subsidy eligibility

- Social Security timing determines how long your portfolio must carry the full load

- Estate decisions shape your heirs' tax exposure decades down the line

Anyone in Minnesota, Michigan, or the broader Midwest working toward retirement at 55 can reach out to Barking Sands Capital for a personalized retirement analysis. As an independent, fee-based RIA, the firm's proprietary InteProcess™ coordinates retirement, tax, healthcare, and estate planning in one integrated strategy — so each decision reinforces the others rather than working against them.

Frequently Asked Questions

What is a good amount of money to retire with at 55?

The general guideline is 25–33x your expected annual expenses, depending on your withdrawal rate assumption. A 40-year retirement warrants the conservative end of that range. Bridge income sources like part-time work, rental properties, or a pension can reduce the required portfolio size by several hundred thousand dollars.

What is the best retirement plan for a 55-year-old?

The most effective approach combines three priorities: maxing out remaining contributions (including 401(k) and IRA catch-up amounts), building a tax-diversified account structure, and establishing a clear income bridge for the years before Social Security and Medicare begin.

Can I withdraw from my 401(k) at 55 without penalty?

Yes, under the Rule of 55 — if you separate from your employer in or after the calendar year you turn 55, you can take penalty-free withdrawals from that employer's 401(k). This does not cover previous employers' plans or IRAs, which still require age 59½ or a 72(t) arrangement to avoid the 10% penalty.

How do I get health insurance if I retire at 55 before Medicare?

Your main options are COBRA (up to 18 months), ACA Marketplace plans with income-based subsidies, a spouse's employer plan, or coverage through part-time work. Healthcare costs during this gap are substantial — manage your income carefully to preserve ACA subsidy eligibility.

Should I claim Social Security early if I retire at 55?

Claiming at 62 permanently reduces your benefit by up to 30% versus waiting until full retirement age (67 for most people). If your bridge income can cover the gap, delaying claiming usually delivers a meaningful lifetime income advantage — though your health and cash flow needs determine the right call.

How does retiring at 55 affect my retirement account access?

Most tax-advantaged accounts carry a 10% early withdrawal penalty until age 59½. The main exception is the Rule of 55, which applies only to your current employer's 401(k). Getting the draw-down sequence right — taxable accounts first, then retirement accounts — is one of the most consequential decisions in an early retirement plan.