The financial advisory industry operates under two distinct legal standards, and only one requires your advisor to put your interests first. The other simply requires that recommendations be "suitable." At modest asset levels, that gap is uncomfortable. At $1 million or more in investable assets heading into a 20–30 year retirement, it compounds into real, measurable financial damage.

This article breaks down what the fiduciary standard actually means, why it matters specifically for HNW retirees, and what you stand to lose without it.

Key Takeaways

- A fiduciary advisor is legally required to act in your best interest, not merely recommend what's "suitable"

- Fee drag on a $1M portfolio can cost $493,000+ over 20 years depending on advisor compensation structure

- RMDs, Roth conversions, and estate exposure create layered complexity that non-fiduciary advisors can't address without conflicts of interest

- 70%+ of heirs leave their parents' advisor after inheriting wealth — a direct result of disconnected legacy planning

- Verifying fiduciary status via the SEC's IAPD database and requesting written confirmation is the concrete first step

What Is a Fiduciary Advisor?

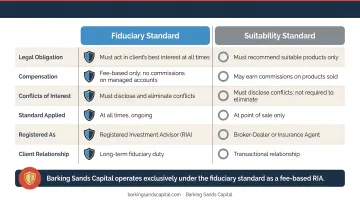

A fiduciary advisor is legally obligated to act in your best interest — always, not just at the moment of a transaction. This isn't a marketing claim; it's a federal legal standard enforced by the SEC under the Investment Advisers Act.

The Two Standards That Divide the Industry

| Standard | Who It Applies To | Legal Requirement |

|---|---|---|

| Fiduciary | Registered Investment Advisors (RIAs) | Must act in client's best interest; disclose all conflicts |

| Suitability | Broker-dealers (FINRA-regulated) | Must recommend something "suitable" based on client profile |

The SEC's 2019 fiduciary interpretation makes clear that an RIA's fiduciary duty covers the entire advisory relationship — not just individual transactions. It includes a duty of care (recommending what's genuinely best) and a duty of loyalty (eliminating or fully disclosing conflicts of interest).

"Suitable" and "best" are not the same thing. A product can be suitable for your situation while simultaneously generating a commission for the advisor and costing you significantly more than an alternative. That gap is legal under the suitability standard — under the fiduciary standard, it isn't. For a retiree with $2 million in assets, the difference between a 1% expense-ratio fund and a 0.10% ETF compounds to more than $300,000 over 20 years.

Key Advantages of a Fiduciary Advisor for High-Net-Worth Retirees

The advantages below aren't abstract principles — they're concrete outcomes that affect portfolio longevity, tax liability, and what you leave behind.

Legally Binding Loyalty With No Hidden Conflicts

An independent RIA is legally prohibited from prioritizing commissions or third-party incentives over client outcomes. They cannot be paid commissions on managed accounts. Every conflict of interest must be disclosed in writing through their Form ADV. Their accountability runs to the SEC or state regulators — not just FINRA's suitability bar.

In practice, this means an RIA must recommend the lowest-cost or highest-benefit option available to you — not the option that generates the best payout for them.

The dollar cost of the suitability gap is not abstract. Consider a $1 million portfolio earning 6% annually:

| Time Horizon | 0.10% Fee | 1.00% Fee | Cost of the Gap |

|---|---|---|---|

| 10 years | ~$1.77M | ~$1.63M | ~$145,000 |

| 20 years | ~$3.15M | ~$2.65M | ~$494,000 |

(Fee-compounding data based on SEC investor bulletin methodology)

Both funds — one at 0.10%, one at 1.00% — might be perfectly "suitable." Only one is in your best interest. A fiduciary is legally required to recommend the better option. A suitability-standard advisor is not.

This risk is highest during high-stakes, one-time decisions: rolling a 401(k) into an IRA, selecting annuity products, or evaluating proprietary fund recommendations. FINRA has explicitly warned that rollovers create economic incentives for advisors whose compensation depends on assets moving into managed accounts. The TIAA enforcement case — which resulted in a $97 million settlement — arose from exactly this type of conflict in retirement rollover recommendations.

Tax-Efficient, Integrated Retirement Income Planning

HNW retirees rarely have a single income stream. They're managing RMDs, Social Security, dividends, rental income, and potentially business distributions — all simultaneously. Without coordinated strategy, that complexity creates unnecessary tax exposure.

A fiduciary advisor — because their compensation isn't tied to specific products — can recommend tax-efficient strategies purely on merit:

- Strategic Roth conversions during lower-income years before RMDs begin, which research published in the Journal of Financial Planning shows can add significant value for higher-income households

- Asset location — placing tax-inefficient assets in tax-deferred accounts and tax-efficient assets in taxable accounts

- Withdrawal sequencing that preserves tax-advantaged growth while managing bracket exposure

- Charitable vehicles like donor-advised funds that reduce both taxable income and estate size

Medicare IRMAA is one underappreciated consequence of uncoordinated income planning. In 2025, Part B IRMAA surcharges begin above $106,000 MAGI for individuals — adding up to $443.90 per month in additional premiums. Poor RMD timing or an unplanned Roth conversion can push retirees across these thresholds unnecessarily.

A non-fiduciary advisor has no legal obligation to recommend the more tax-efficient option — only the suitable one. That distinction can quietly cost retirees tens of thousands in avoidable taxes.

Coordinated Estate and Legacy Planning Across Generations

HNW retirees aren't only planning for their own income. They're protecting wealth for heirs, charitable goals, and in many cases, generational trusts. The challenge is that estate planning involves multiple professionals — CPAs, estate attorneys, insurance specialists — who typically work in silos.

A fiduciary advisor bridges those silos. In practice, that means:

- Ensuring the estate attorney's documents reflect the current tax situation

- Confirming the CPA's strategy doesn't inadvertently undermine the trust structure

- Aligning insurance decisions with both the legacy plan and the investment portfolio

Barking Sands Capital's proprietary InteProcess™ is built around exactly this kind of integration — coordinating legal, insurance, tax, retirement, and financial planning professionals as a unified team rather than independent advisors working without awareness of each other.

Why does this matter? Cerulli Associates found that more than 70% of heirs are likely to leave or change their parents' financial advisor after inheriting wealth. That statistic reflects a failure of relationship continuity, and it signals what happens when legacy planning isn't coordinated around the family's values and goals from the start.

That coordination gap has a measurable foundation: Bank of America Private Bank's 2024 Study of Wealthy Americans found that 52% of wealthy Americans lack all three basic estate-plan elements: a will, an advance healthcare directive, and a durable power of attorney. Among HNW families with estates approaching the current federal exemption of $13.99 million, those gaps can trigger avoidable estate tax exposure.

What Happens When HNW Retirees Work Without a Fiduciary Advisor

The suitability standard doesn't prohibit bad advice. It prohibits unsuitable advice — which is a much lower bar.

An advisor operating under suitability can legally recommend a higher-fee mutual fund, a commission-generating annuity, or a proprietary product — and none of it constitutes a breach of duty. At the $1 million+ level, the dollar cost of that latitude is substantial.

Common real-world consequences for HNW retirees without fiduciary oversight:

- CPA, estate attorney, and broker each advising independently, with no single professional accountable for the integrated picture

- Roth conversion windows missed between retirement and RMD onset — an opportunity that closes permanently once mandatory distributions begin

- Estate documents that don't reflect current tax law, asset structures, or family circumstances, discovered only after it's too late to correct

- Whole life insurance, high-fee annuities, and proprietary funds eroding long-term portfolio value without the client realizing it

Those consequences have a price tag. The fee structure alone — independent of market performance — determines how much wealth actually transfers to you and your heirs. On a $1.5 million portfolio earning 6% annually over 20 years:

- At a 0.10% fee: grows to approximately $4.72 million

- At a 1.00% fee: grows to approximately $3.98 million

- Difference: ~$741,000

That $741,000 is purely the cost of a higher fee structure — the kind a suitability-standard advisor has no legal obligation to minimize.

How to Get the Most From Your Fiduciary Advisor Relationship

Working with a fiduciary is where the work begins. The real value comes when the relationship extends beyond investment management to address your full financial picture.

Verify Fiduciary Status Before Signing Anything

- Search the SEC's IAPD database at adviserinfo.sec.gov to confirm RIA registration

- Request Form ADV Part 2 — this plain-English document discloses services, fee structures, and any conflicts of interest

- Ask directly: "Are you a fiduciary?" and get the answer in your advisory agreement in writing

- Clarify compensation: "Do you receive any compensation other than what I pay you directly?" Fee-based advisors can still earn commissions on certain products — fee-only advisors cannot

Ask the Questions That Reveal Real Alignment

- How are you compensated if I stay in my current 401(k) plan versus rolling over to an IRA?

- Do you recommend any products where you receive third-party compensation?

- Who holds my assets, and how can I verify that independently?

That last question matters more than most retirees realize. Barking Sands Capital holds client assets with independent third-party custodians (Altruist, Pershing, Schwab, and TD Ameritrade), creating a clear separation between advisory decisions and asset custody. That structure adds a concrete layer of protection beyond the fiduciary standard itself.

Expect Proactive, Annual Reviews

The most valuable fiduciary relationships are ongoing. Tax laws shift, family dynamics evolve, and RMD rules get updated. An advisor who reviewed your strategy in year one and hasn't revisited it since isn't delivering fiduciary value — that's a one-time plan in a dynamic environment.

HNW retirees should demand annual reviews that revisit:

- Withdrawal sequencing given current tax brackets

- Roth conversion opportunities or RMD adjustments

- Estate document alignment with current law and family circumstances

- Insurance coverage relative to current estate size and longevity projections

Conclusion

For HNW retirees, "suitable" is not good enough. The fiduciary standard gives you a legally binding guarantee that your advisor's financial interests and yours are aligned — and that alignment has measurable value in reduced fees, tax savings, estate outcomes, and portfolio longevity across a decades-long retirement.

The first step is simple: ask "Are you a fiduciary?" and get the answer in writing.

If you're in Michigan, Minnesota, or anywhere across the Midwest managing serious wealth, Barking Sands Capital is an independent, fee-based RIA built for exactly this kind of work. No commissions on managed accounts, full conflict disclosure, and a proprietary InteProcess™ that coordinates your full financial picture — investment, tax, estate, and insurance — under one integrated plan. Reach the Minnesota office at 952-500-8854 or the Michigan office at 248-687-1040.

Frequently Asked Questions

What is considered high-net-worth for a financial advisor?

The financial services industry generally defines high-net-worth as $1 million or more in investable assets, excluding primary residence. Very High Net Worth starts at $5 million and Ultra High Net Worth at $30 million. These thresholds affect which planning strategies, account minimums, and specialized services are available to you.

What did Warren Buffett say about financial advisors?

Buffett has been consistently skeptical of high-fee active management. In his 2016 shareholder letter, he wrote: "When trillions of dollars are managed by Wall Streeters charging high fees, it will usually be the managers who reap outsized profits, not the clients." His own advice to his wife's trustee was to use a very low-cost index fund.

What is the difference between a fiduciary and a non-fiduciary financial advisor?

A fiduciary is legally required to act in the client's best interest at all times and must disclose all conflicts of interest. A non-fiduciary (typically a broker-dealer) only needs to recommend something "suitable" — a lower bar that permits commission-driven recommendations even when better options exist for the client.

How can I verify if my financial advisor is a fiduciary?

Check the SEC's IAPD database at adviserinfo.sec.gov for RIA registration, then review their Form ADV Part 2 for fee disclosures and conflict-of-interest statements. Ask the advisor directly for written fiduciary confirmation in the advisory agreement before signing.

Is a fee-only advisor the same as a fiduciary advisor?

Not exactly. Fiduciary is a legal standard; fee-only is a compensation description. Most fiduciary RIAs are fee-only or fee-based, but the terms aren't interchangeable. Fee-only means no third-party commissions; fee-based means the advisor charges fees but may also earn commissions on certain products. Always confirm fiduciary status separately from the fee structure.

What types of financial planning do HNW retirees most need from a fiduciary advisor?

HNW retirees benefit most from fiduciary guidance in the areas where conflicts of interest run highest for non-fiduciary advisors:

- Tax-efficient withdrawal sequencing

- RMD planning and Roth conversions before mandatory distributions begin

- Estate and legacy coordination

- Social Security timing

- Medicare IRMAA management