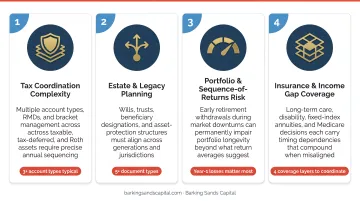

A generic 4% withdrawal rule or a standard 60/40 portfolio wasn't built for a balance sheet that includes business interests, concentrated equity positions, real estate, and alternative investments. Neither was it built for clients who face RMD tax cliffs, IRMAA Medicare surcharges, or estate tax exposure measured in the millions.

This guide covers the core strategies that matter at this level: building a complete financial picture, tax-efficient account structuring, strategic withdrawal planning, diversified income, insurance, and estate planning.

Key Takeaways

- HNWIs face structuring and distribution challenges, not just accumulation challenges

- Three-bucket account structures (tax-deferred, tax-free, taxable) give you flexibility to manage income and taxes throughout retirement

- SECURE 2.0 extended the RMD window, creating a prime opportunity for Roth conversions before distributions begin

- A private nursing home room costs $129,575 annually (CareScout, 2025) — long-term care is one of the most underestimated retirement risks

- At this wealth level, estate planning and retirement planning are the same conversation — coordinate them together

Why Standard Retirement Planning Falls Short for High-Net-Worth Individuals

Who Qualifies as High-Net-Worth

Capgemini's 2026 World Wealth Report defines HNWIs as individuals with at least $1 million in investable assets, excluding primary residence, collectibles, and consumables. The tiers break down as:

- $1M–$5M: Core HNWI

- $5M–$30M: Mid-tier/Very High Net Worth

- $30M+: Ultra High Net Worth

Planning complexity grows sharply at each tier. A $3M portfolio managed primarily through traditional retirement accounts presents very different challenges than a $15M portfolio spanning real estate, private equity, a family business, and multiple brokerage accounts.

Where Generic Models Break Down

Morningstar's 2025 research pegged the highest safe starting withdrawal rate at 3.9% for a consistent real-withdrawal strategy — and that's for straightforward portfolios. HNWIs contend with layers of complexity that generic models don't account for:

- RMD tax cliffs: Large tax-deferred balances generate mandatory distributions at age 73 (rising to 75 for those born after 1960 under SECURE 2.0) that can push income into higher brackets

- IRMAA surcharges: Medicare Part B premiums spike sharply above $106,000 single / $212,000 joint MAGI — a threshold easily crossed by an HNWI taking uncoordinated withdrawals

- Concentrated positions: A single stock comprising 30–40% of a portfolio introduces retirement-ending risk that a 60/40 allocation model never addresses

- Estate exposure: For estates above current exemption thresholds, the wrong account structure can create a significant and avoidable tax burden for heirs

Each of these challenges requires coordinated planning across tax, investment, and estate strategy — not a generic withdrawal model. Working with an independent, fee-based RIA ensures recommendations reflect your goals rather than a product shelf. Barking Sands Capital is structured precisely this way: as a registered investment advisor, it earns no commissions on managed accounts, and client assets are held with independent custodians including Schwab and Pershing.

Build a Complete Financial Picture Before Anything Else

Mapping Assets, Liabilities, and Long-Range Cash Flow

Before any withdrawal strategy or tax optimization can work, you need an accurate, complete picture of what you actually have. For HNWIs, this means going well beyond retirement account balances.

A comprehensive net-worth statement should capture:

- Retirement accounts (IRAs, 401(k)s, Roth accounts)

- Taxable brokerage accounts

- Real estate holdings — primary residence, investment properties, and their equity positions

- Business interests, including partial ownership stakes and anticipated buyout timelines

- Concentrated equity positions and restricted stock

- Alternative investments (private equity, hedge funds, real assets)

- Anticipated liquidity events: inheritances, business sales, deferred compensation payouts

Illiquid assets are where blind spots form. A business interest worth $4M on paper may take 3–5 years to monetize — and its absence from a cash flow model creates false confidence in income availability.

A long-range cash flow projection (20+ years) surfaces risks that a point-in-time snapshot misses entirely. The three most consequential:

- Sequence-of-return risk in the first decade of retirement, when early losses permanently impair portfolio longevity

- The RMD income spike, when mandatory distributions push taxable income higher than anticipated

- Liquidity gaps, where current liquid assets can't support planned lifestyle spending without forced asset sales at the wrong time

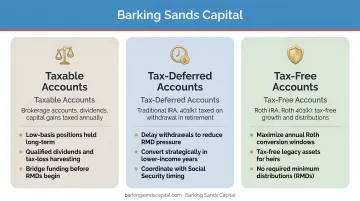

Choosing the Right Account Structure

Every HNWI retiree benefits from maintaining assets across three tax "buckets":

| Bucket | Account Types | Tax Treatment |

|---|---|---|

| Tax-Deferred | Traditional IRA, 401(k), SEP IRA | Contributions pre-tax; withdrawals taxed as ordinary income |

| Tax-Free | Roth IRA, Roth 401(k) | Contributions after-tax; withdrawals tax-free |

| Taxable | Brokerage accounts | Contributions after-tax; growth taxed at capital gains rates |

Having all three gives you flexibility to manage your effective tax rate year by year in retirement — drawing from different buckets depending on your income picture each year.

The gap-year conversion opportunity: The window between leaving the workforce and when RMDs begin is prime time for Roth conversions. Income is often at its lowest during these years, and converting tax-deferred balances to Roth at lower rates reduces the size of future mandatory distributions. For high earners above direct Roth contribution limits, backdoor Roth and mega-backdoor Roth strategies extend access to the same tax-free growth — regardless of income.

Barking Sands Capital's InteProcess™ coordinates these account structure decisions across tax, retirement, insurance, and estate planning together, so a Roth conversion doesn't inadvertently conflict with an estate plan or prompt an unplanned insurance review.

Tax Efficiency and Withdrawal Planning for High-Net-Worth Retirees

Strategic Withdrawal Sequencing

The conventional withdrawal order — taxable accounts first, then tax-deferred, then Roth — allows tax-advantaged assets to compound longer. For many retirees, this sequencing works well.

For HNWIs, a blended withdrawal approach often produces better outcomes. Rather than depleting one bucket entirely before touching the next, drawing from multiple account types in the same year can keep modified adjusted gross income below critical thresholds:

- IRMAA brackets: Even a modest unplanned distribution can push MAGI above the $106,000 single threshold, adding hundreds of dollars in monthly Medicare surcharges

- Tax bracket management: Staying just below the top of the 22% or 24% bracket often justifies a Roth conversion to fill that bracket, even when liquid cash isn't needed

SECURE 2.0 extended RMD start ages — currently age 73, rising to 75 for those born after December 31, 1959. That extended window is valuable: more time for Roth conversions, more time for tax-deferred accounts to compound, and more flexibility in sequencing withdrawals before mandatory distributions begin.

Tax-Advantaged Plans and Charitable Strategies

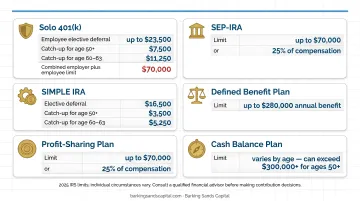

Withdrawal sequencing only captures part of the tax picture. For self-employed and small business owners, pre-retirement deferral opportunities can be equally consequential. IRS 2025 limits include:

- 401(k) elective deferral: $23,500

- Total defined contribution limit (solo 401(k)): $70,000

- SEP IRA cap: $70,000 (lesser of this or 25% of compensation)

- Defined benefit annual benefit limit: $280,000

Defined benefit and cash-balance plans can allow far higher contributions based on actuarial calculations — often the most effective pre-retirement deferral tool available to high-earning business owners. Barking Sands Capital integrates cash-balance plan analysis directly into its small business owner planning work, coordinating contribution strategy with the broader retirement picture.

Charitable giving vehicles serve a dual purpose — reducing taxable income while advancing philanthropic goals:

- Qualified Charitable Distributions (QCDs): Available starting at age 70½, with a 2025 annual limit of $108,000 (rising to $111,000 in 2026). QCDs count toward RMDs and are excluded from taxable income — a more efficient mechanism than taking a distribution and then donating separately.

- Donor-Advised Funds (DAFs): Cash contributions are generally deductible up to 60% of AGI; appreciated securities up to 30% of AGI — while the fund distributes grants on your timeline.

- Charitable Remainder Trusts: Provide income during your lifetime and transfer the remainder to charity, with a partial upfront deduction.

The current tax planning window: The IRS now lists the 2026 estate exemption at $15 million under Public Law 119-21. The broader TCJA provisions — including the 20% qualified business income deduction under Section 199A and the larger standard deduction — carry real legislative uncertainty beyond 2025.

Structuring conversions, gifts, and income recognition now — while current rates are confirmed — preserves optionality that becomes unavailable if rates rise or deductions narrow. That window is open today; it may not be in 2026.

Building Diversified, Durable Income Streams

Beyond the Traditional Portfolio

BlackRock notes that the traditional 60/40 portfolio is under pressure and that alternatives can help rebuild resilience. HNWIs are better positioned than most to act on this.

Income-generating alternatives worth considering:

- Private credit: Floating-rate returns with lower correlation to public equity markets

- Real assets and infrastructure: Inflation-sensitive income with long duration

- Dividend-focused equities: Cash flow without forced asset sales during downturns

- Rental real estate: Consistent income that can be structured for tax efficiency

The data supports this shift: according to Preqin, family offices — a reasonable proxy for UHNW portfolios — planned to allocate 42% to private markets in 2024. That's roughly double what most retail portfolios hold in alternatives — a gap that reflects different risk tolerances, liquidity needs, and time horizons.

Diversifying income sources reduces reliance on public market performance during downturns. If equities drop 30%, a retiree drawing solely from a stock portfolio locks in losses. A retiree with rental income, private credit distributions, and dividend income can avoid selling into a down market entirely.

Managing Concentration Risk

A concentrated equity position — often the result of a career at one company, a successful business exit, or restricted stock grants — can represent the single largest risk in an HNWI's retirement portfolio. A 40% single-stock position that declines 50% erases 20% of total net worth in one event.

Strategies for reducing concentration while managing tax consequences:

- Staged liquidation: Spreading sales across multiple tax years to stay within preferred capital gains brackets

- Exchange funds: Contributing shares to a diversified fund in exchange for a proportional interest, deferring the gain

- Charitable strategies: Donating appreciated shares directly to a DAF or CRT eliminates capital gains entirely while generating a deduction

- Hedging: Protective puts or collars allow participation in upside while limiting downside — at a cost

These strategies address the concentration problem directly, but portfolio resilience also depends on what replaces that position. Private equity, hedge funds, and real assets offer returns that don't move in lockstep with public markets — giving the portfolio a more stable foundation once the concentrated holding is reduced. Each comes with higher risk and limited liquidity, so the right mix depends on your overall financial picture and investment timeline.

Protecting Your Wealth: Insurance, Healthcare, and Risk Management

As net worth grows, so does exposure. Luxury properties, high-value vehicles, household employees, and public visibility all create litigation risk that standard homeowners and auto policies won't cover.

Umbrella insurance provides excess liability coverage beyond primary policy limits. For HNWIs, coverage limits should be reviewed against actual net worth regularly — not just at initial purchase. What was adequate at $2M in assets may be significantly insufficient at $8M.

Long-term care remains one of the most underestimated retirement costs. According to CareScout's 2025 survey:

- Private nursing home room: $129,575/year

- Assisted living: $74,400/year

- Home health aide: $75,432/year

The HHS/ACL reports that someone turning 65 has nearly a 70% probability of needing long-term care services, with women averaging 3.7 years of care and men 2.2 years. At private nursing home rates, that's a potential exposure exceeding $300,000 for women and $280,000 for men.

Hybrid LTC policies and asset-based solutions allow HNWIs to shift this risk off their personal balance sheet without permanently surrendering capital — if care is never needed, the policy's death benefit or remaining value transfers to heirs.

Curtis Hewitt, Barking Sands Capital's advisor specializing in Medicare Planning and Long-Term Care, works directly with clients on these strategies alongside IRMAA (Medicare premium surcharge) management.

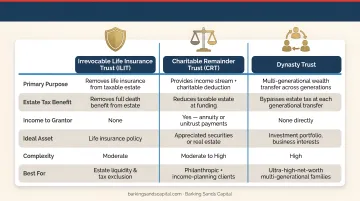

Life insurance needs evolve just as significantly. A policy purchased at 35 for income replacement may be the wrong tool at 60. Policies designed for estate liquidity, business continuation, or funding an Irrevocable Life Insurance Trust (ILIT) serve fundamentally different purposes. Review existing coverage against your current net worth, estate structure, and goals — don't simply renew it.

Estate Planning, Legacy, and Family Wealth Transfer

The IRS currently lists the 2026 basic estate and gift tax exclusion at $15 million per individual under Public Law 119-21. While this represents a favorable environment for wealth transfer planning, the history of this exemption — fluctuating significantly over the past two decades — makes a strong case for acting now rather than waiting.

Trust structures commonly used to remove future appreciation from taxable estates include:

- SLATs (Spousal Lifetime Access Trusts): Allow one spouse to gift assets irrevocably while the other retains indirect access

- GRATs (Grantor Retained Annuity Trusts): Transfer appreciation above a hurdle rate to heirs gift-tax-free

- ILITs (Irrevocable Life Insurance Trusts): Keep life insurance death benefits out of the taxable estate while preserving liquidity for heirs

Treat estate documents as living ones, not permanent ones. Wills, powers of attorney, beneficiary designations, and trust structures all need to reflect current net worth, family structure, and tax law — none of which stays static.

Common mistake: Failing to update beneficiary designations after a divorce, remarriage, or the birth of a grandchild ranks among the most costly oversights HNW retirees make.

Keeping documents current is only half the equation. Families who also communicate estate plans, trust structures, and financial expectations to heirs in advance are far better positioned to avoid conflict, preserve financial literacy across generations, and ensure charitable priorities are honored after the wealth transfers.

Barking Sands Capital coordinates estate planning as part of its InteProcess™ — integrating wills, trusts, and asset protection decisions with tax, retirement, and insurance planning rather than treating them as separate engagements.

Frequently Asked Questions

How do high-net-worth individuals plan for retirement?

HNWIs typically combine holistic balance sheet planning, multi-bucket tax account strategies, coordinated withdrawal sequencing, diversified income sources, and advanced estate planning tools. That complexity means a professional advisory team — one that coordinates tax, legal, insurance, and investment disciplines — is a necessity, not a nice-to-have.

What is the 70/30 rule for millionaires?

The 70/30 concept refers to an approximate allocation of 70% growth assets and 30% defensive or income-generating assets. It's a useful starting framework, but HNWIs should work with an advisor to customize allocation based on their actual risk tolerance, timeline, income needs, and the full range of assets they hold.

What is considered high net worth for retirement planning purposes?

The most widely cited thresholds come from Capgemini: $1M+ in investable assets for HNWI, $5M–$30M for the mid-tier, and $30M+ for ultra-high-net-worth. Planning complexity increases significantly at each tier.

What are the biggest retirement planning mistakes high-net-worth individuals make?

The most common include failing to update estate documents after life changes, underestimating long-term care costs, holding concentrated positions too long into retirement, missing multi-year tax optimization opportunities like Roth conversions, and not communicating estate plans to family members in advance.

How does estate planning connect to retirement planning for HNWIs?

For HNWIs, the two disciplines are deeply intertwined. Account type choices, withdrawal timing, beneficiary designations, and trust structures all affect both retirement income and eventual wealth transfer. Coordinating them under one planning framework consistently produces better outcomes than treating them as separate concerns.

When should high-net-worth individuals start working with a financial advisor for retirement planning?

Starting 10 or more years before retirement creates the most flexibility. That lead time allows for optimizing account structures, executing multi-year Roth conversion strategies, addressing estate planning while more options are still available, and building the diversified income streams a secure retirement requires.