Introduction

Picture this: you've spent 35 years building a retirement nest egg — maxing out your 401(k), paying down debt, staying disciplined through every market downturn. Then, in your mid-70s, a health event requires nursing home care. Within two years, decades of savings are gone.

This isn't a worst-case outlier. According to AARP's 2024 analysis, 56% of people turning 65 between 2021 and 2025 will need some form of long-term services and supports.

The cost is staggering: nursing home care hit $111,325 per year for a semi-private room and $127,750 for a private room in 2024, per Genworth and CareScout's 2024 Cost of Care Survey.

Most people assume Medicare will cover it. It won't — not for long-term care. This guide explains exactly why that gap exists, how Medicaid rules work, and what specific steps can protect your savings before a health crisis forces the decision.

Key Takeaways

- Nursing home costs exceed $111,000 per year nationally and are not covered by standard Medicare

- Medicaid covers long-term care but requires assets below $2,000 in most states — nearly everything must be spent down first

- A 60-month lookback period means asset transfers must happen years before applying for Medicaid

- Preservation strategies — including irrevocable trusts, Medicaid-compliant annuities, and LTC insurance — must be structured well in advance

- Protecting your savings takes coordinated planning across financial, legal, and insurance disciplines — not a single fix

The Real Cost of Nursing Home Care — and Why Medicare Won't Save You

The Numbers Are Stark

Most people underestimate how quickly nursing home costs can drain a retirement account. At $111,325 per year for a semi-private room, a two-year stay costs over $222,000. A three-year stay approaches $334,000 — well above the average Vanguard defined contribution plan balance of $148,153 reported at year-end 2024.

For most households, even a moderate nursing home stay would wipe out retirement savings entirely — and that's before accounting for a spouse's ongoing living expenses.

The Medicare Gap

Medicare's coverage of skilled nursing facility (SNF) care is limited and conditional:

| Days in SNF | What You Pay (2026) |

|---|---|

| Days 1–20 | $0 (after Part A deductible of $1,736) |

| Days 21–100 | $217/day coinsurance |

| Days 101+ | You pay all costs |

There's also a key qualifier: Medicare SNF coverage only kicks in after a qualifying hospital stay of at least three days. It does not cover custodial care — meaning help with bathing, dressing, eating, or daily activities — which is exactly what most long-term nursing home residents actually need.

Private health insurance follows the same pattern. According to the ACL, most private plans cover only the same limited services as Medicare. That leaves two realistic funding sources: personal assets or Medicaid.

KFF reports that Medicaid is already the primary payer for more than 6 in 10 nursing facility residents — and in 2023, Medicaid paid 44% of all long-term institutional care costs. That's why knowing the Medicaid rules — eligibility, spend-down requirements, and asset protections — is where any serious planning has to start.

How Medicaid Works — and Why the 5-Year Lookback Changes Everything

Eligibility: The Asset Limits

Medicaid is a means-tested program. To qualify for long-term nursing home coverage, you must meet strict income and asset requirements. In most states, countable assets must be reduced to $2,000 or less per individual before Medicaid kicks in.

Not all assets count equally. Here's the distinction:

Exempt assets (not counted toward the $2,000 limit):

- Primary residence (up to a home equity limit of $752,000–$1,130,000 depending on the state in 2026)

- One vehicle

- Personal household belongings

- Certain life insurance policies and burial funds

Countable assets (must be spent down):

- Savings and checking accounts

- Investment and brokerage accounts

- Second properties or vacation homes

- Most retirement accounts (varies by state)

That spend-down requirement is precisely why Medicaid planning can't be left until a crisis hits.

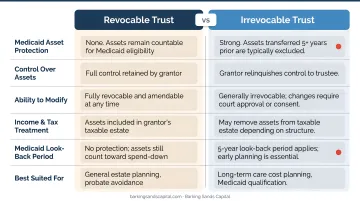

The 60-Month Lookback Period

Medicaid doesn't just look at what you own today. It reviews all financial transfers made in the 60 months (five years) prior to your application — and this catches many families completely off guard.

Any of the following can trigger a penalty period of Medicaid ineligibility:

- Gifts of cash or assets to children or grandchildren

- Transfers to irrevocable trusts

- Real estate transfers at below-market value

How the penalty is calculated:

The penalty period = uncompensated value of transferred assets ÷ average monthly nursing home private-pay rate in your state.

For example: if you gifted $90,000 to your children 18 months before applying for Medicaid, and your state's average monthly nursing home rate is $9,000, you'd face a 10-month penalty period during which Medicaid won't pay — even though your assets are otherwise depleted.

Estate Recovery After Qualification

Qualifying for Medicaid doesn't fully close the door on asset loss. Federal law (OBRA 1993) requires states to seek recovery from the estates of Medicaid enrollees age 55 and older for nursing facility services and related care.

Key points families often overlook:

- States must pursue recovery from probate estates at minimum

- Many states use broader definitions that reach jointly held property and assets passing outside probate

- A home that was exempt during the Medicaid application can still be subject to a recovery claim after death

- Protection strategies matter both before and after qualification

This is why estate planning and Medicaid planning need to work together — not as separate conversations.

Strategies to Protect Your Retirement Savings From Nursing Home Costs

Most of these strategies require a five-year runway to be effective. The right combination depends on your assets, health status, marital situation, and state of residence. None of them should be attempted without professional guidance.

Irrevocable Medicaid Asset Protection Trusts

An irrevocable Medicaid Asset Protection Trust (MAPT) works by permanently transferring ownership of assets into a trust. Once transferred:

- You relinquish control over those assets

- The trust becomes the legal owner

- After five years, Medicaid no longer counts those assets toward eligibility

Critical distinctions:

- A revocable living trust provides no Medicaid protection — federal rules treat the assets as still available to you

- Only an irrevocable trust, properly structured and funded more than 60 months before application, provides protection

- Trust structures that allow the creator to receive principal distributions will not qualify

IRAs require separate consideration. Some states allow an irrevocable income-only trust to shelter IRA assets, with only required minimum distributions (RMDs) flowing out as income. This preserves principal from Medicaid spend-down, but the rules are highly state-specific and require careful legal drafting.

Medicaid-Compliant Annuities

For people already close to needing care, or past the five-year planning horizon, a Medicaid-compliant annuity provides a faster path to eligibility. It converts a lump-sum countable asset into a structured income stream that Medicaid no longer counts against eligibility.

To qualify under federal rules, the annuity must be:

- Actuarially sound (payments must be completed within the applicant's life expectancy)

- Irrevocable and non-assignable

- Free of deferral or balloon payments

- Structured to name the state Medicaid agency as the primary remainder beneficiary

That state beneficiary requirement carries real consequences: upon death, the state can recover costs paid from any remaining annuity value. Not all commercially available annuities meet these requirements, which is why professional structuring is essential.

Strategic Gifting

Gifting assets to family members reduces your countable asset total, but only if done well outside the five-year lookback window.

The IRS annual gift tax exclusion is $19,000 per recipient in 2026, meaning you can give up to that amount per person without triggering a gift tax return. However, this has no bearing on Medicaid. A gift that's below the IRS threshold is still a Medicaid-penalized transfer if made inside the 60-month lookback period.

The most common mistake: assuming that giving assets to children or grandchildren now will protect those assets if care is needed within five years. It won't — and may leave you with depleted assets and a Medicaid penalty at the same time.

Spousal Protections

When one spouse requires nursing home care, Medicaid doesn't leave the healthy spouse with nothing. Federal spousal impoverishment protections include:

- Community Spouse Resource Allowance (CSRA): The at-home spouse may retain between $32,532 and $162,660 in assets (2026 federal range; states set the exact figure within this range)

- Minimum Monthly Maintenance Needs Allowance (MMMNA): The at-home spouse may retain between $2,643.75 and $4,066.50 per month in income (2026 federal range)

These federal floors offer meaningful protection, but a healthy spouse relying solely on them could still lose the majority of a lifetime's savings before eligibility kicks in. Early planning — ideally years before care is needed — can substantially raise the amount a couple actually keeps.

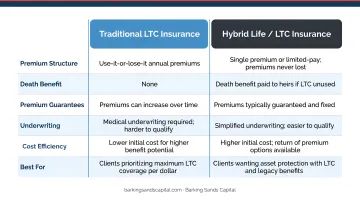

Long-Term Care Insurance: A Proactive First Line of Defense

Long-term care insurance takes a different approach than most asset protection strategies. Rather than restructuring assets after they're accumulated, LTC insurance creates a pool of benefits that pays for care directly. This can delay or eliminate the need to spend down assets or apply for Medicaid at all.

LTC insurance pays a daily or monthly benefit toward:

- Nursing home care

- Assisted living facility costs

- In-home care and adult day services

When to Buy — and What's Changed

Timing is the central trade-off. Premiums are significantly more affordable when purchased in your 50s or early 60s. AALTCI data shows that 55.2% of traditional LTC insurance buyers are ages 55–64, confirming this as the prime purchasing window. Premiums increase with age, and health conditions can disqualify applicants entirely — making early action, not eventual action, the right approach.

LIMRA estimated in 2024 that only 3% to 4% of adults over 50 carry any form of long-term care insurance, leaving the vast majority of retirees fully exposed.

That low uptake often comes down to one concern: paying premiums for decades and never collecting benefits. For those clients, hybrid life insurance policies with long-term care riders offer a practical alternative. These combination products, addressed under the Pension Protection Act, provide a death benefit if LTC benefits go unused — eliminating the "use it or lose it" concern of traditional standalone policies.

Curtis Hewitt, Barking Sands Capital's advisor specializing in Medicare Planning and Long-Term Care, helps clients evaluate these options as part of a broader retirement protection strategy. The goal isn't to sell a product — it's to determine whether LTC insurance, a hybrid policy, or a different approach fits each client's overall financial picture.

When to Start Planning — and Who Needs to Be Involved

The most consistent theme across every strategy in this guide: they require time. The five-year lookback period means that families who begin planning after a diagnosis or health crisis have already lost access to the most powerful tools available.

The Right Team

Protecting retirement savings from nursing home costs isn't a single-discipline problem. It requires two distinct types of expertise working in coordination:

- An elder law attorney to draft irrevocable trusts, life estates, and powers of attorney — legal structures that must be precisely executed

- A financial advisor to align investment management, LTC insurance, income planning, and asset structure so the protection plan doesn't create unintended consequences

Neither professional working alone produces the best outcome. An irrevocable trust drafted without considering income tax implications can create a new problem while solving the old one — and LTC insurance selected without evaluating Medicaid interaction can leave significant gaps.

Where Barking Sands Capital Fits

Barking Sands Capital is an independent, fee-based RIA serving clients in Minnesota, Michigan, and across the Midwest. Through their proprietary InteProcess™, Barking Sands Capital coordinates legal, insurance, tax, retirement, and financial planning — so long-term care protection is integrated into the client's complete financial picture, not handled as an afterthought.

The team brings focused expertise to this work:

- JB L'Esperance (ChFC) — investment management, retirement analysis, and estate planning

- Andrea Cervena (CFP®) — retirement planning, tax planning, and estate planning coordination

- Curtis Hewitt — Medicare planning and long-term care strategy

Because Barking Sands Capital operates on a fee-based model without commissions, insurance recommendations reflect what fits the client's situation — nothing else.

For clients approaching that five-year window, starting this conversation before a health event — not after — is what keeps the most effective options available.

Frequently Asked Questions

How can I protect my retirement savings from nursing home costs?

The most effective strategies (irrevocable trusts, long-term care insurance, Medicaid-compliant annuities, and strategic gifting) must be implemented at least five years before needing care. Start with a financial advisor and elder law attorney who can assess your specific situation and build a coordinated plan.

Can a nursing home take your money if you have an irrevocable trust?

Assets properly transferred into an irrevocable trust more than five years before applying for Medicaid are generally not counted toward eligibility. The nursing home or Medicaid program cannot access the trust principal, provided the five-year lookback and state-specific rules are carefully followed during setup.

Does Medicare cover nursing home costs?

Medicare only covers short-term skilled nursing facility stays — up to 100 days after a qualifying hospital admission — and only for skilled care, not custodial care. Ongoing nursing home residency for help with daily activities is not covered by Medicare.

What is the Medicaid 5-year lookback period?

Medicaid reviews all asset transfers made in the 60 months before an application. Transfers that appear designed to reduce assets, such as gifts, trust transfers, and real estate transfers, can trigger a penalty period of ineligibility calculated on the value transferred.

What assets are exempt from Medicaid when applying for nursing home coverage?

The primary residence (up to a state-set equity limit), one vehicle, personal household belongings, and certain life insurance policies are typically exempt from Medicaid's countable asset calculation. Rules vary by state, so verify your state's specific limits with an elder law attorney.

How does long-term care insurance protect retirement savings?

LTC insurance pays a daily or monthly benefit for nursing home or in-home care, reducing or eliminating the need to liquidate retirement accounts. Purchasing coverage in your 50s or early 60s provides the best balance of comprehensive coverage and affordable premiums — before health conditions affect eligibility.