Introduction

Running your own business comes with real trade-offs. No employer matching contributions. No automatic payroll deductions. No HR department enrolling you in a plan by default. If you're self-employed, retirement savings only happen when you make them happen.

Self-employed individuals actually have access to some of the most flexible, high-contribution retirement accounts available. A well-structured Solo 401(k) or SEP IRA can shelter significantly more income than most corporate employees ever could — if you know which account fits your situation.

This guide covers the five main retirement account options available to self-employed individuals and sole proprietors: how each one works, who it's best suited for, and how to build a strategy that holds up through variable income and shifting tax circumstances.

Key Takeaways

- Self-employed individuals can access five tax-advantaged accounts: Traditional IRA, Roth IRA, SEP IRA, Solo 401(k), and SIMPLE IRA — each with different contribution limits and tax treatment

- Solo 401(k)s and SEP IRAs offer the highest contribution ceilings for higher-earning self-employed individuals

- Income stability, tax bracket trajectory, employee headcount, and administrative complexity all factor into choosing the right plan

- Layering multiple accounts improves tax diversification and long-term retirement flexibility

- A fee-based financial advisor connects your retirement plan to your broader tax, business, and estate planning picture

Why Retirement Planning Looks Different When You're Self-Employed

When you're self-employed, you wear two hats: employer and employee. That dual role changes almost everything about how retirement contributions work — how limits are calculated, how deductions apply, and how much flexibility you have compared to a W-2 worker.

Three factors make this especially complex for the self-employed:

- Contribution math is circular. Limits on plans like the SEP IRA and Solo 401(k) are based on net self-employment earnings — calculated after deducting both the employer-equivalent portion of self-employment tax and the retirement contribution itself. Most people need a tax professional to calculate their true maximum.

- Income variability complicates fixed schedules. A strong quarter doesn't guarantee a strong year. Fixed monthly contributions that work for W-2 earners break down when revenue shifts by season or client cycle.

- No automatic enrollment safety net. W-2 workers often get enrolled in a 401(k) by default. Self-employed individuals have to build that structure themselves — entirely from scratch.

According to the Federal Reserve's 2024 household data, 31% of non-retired Americans had no retirement savings at all. Without employer-sponsored enrollment, self-employed individuals are disproportionately at risk of landing in that group.

5 Self-Employed Retirement Account Options

These five accounts represent the core options the IRS makes available to self-employed individuals and small business owners. Each one was designed with different income levels, tax preferences, and business structures in mind.

Traditional IRA

A Traditional IRA is the most accessible starting point. Contributions may be tax-deductible depending on your income and filing status, growth is tax-deferred, and withdrawals in retirement are taxed as ordinary income.

2025/2026 contribution limits:

- 2025: $7,000, plus $1,000 catch-up for ages 50+

- 2026: $7,500, plus $1,100 catch-up for ages 50+

Best for: Individuals early in their self-employment journey, those with lower net earnings, or anyone expecting to be in a lower tax bracket at retirement.

One important caveat: if you're also covered by a SEP IRA, SIMPLE IRA, or Solo 401(k), the IRS treats you as an "active participant" in a workplace plan. Your Traditional IRA deduction may phase out based on income.

In 2025, that phase-out begins at $79,000 for single filers and $126,000 for married filing jointly (both covered).

The main limitation is the contribution ceiling. At $7,000 annually, a Traditional IRA alone won't build the retirement savings most self-employed professionals need.

Roth IRA

The Roth IRA flips the tax treatment: you contribute after-tax dollars now, and qualified withdrawals in retirement are completely tax-free. There are also no required minimum distributions (RMDs) during your lifetime.

2025/2026 contribution limits: Same as the Traditional IRA — $7,000 in 2025 and $7,500 in 2026, with the same catch-up provisions.

2025 income phase-outs (MAGI):

- Single filers: $150,000–$165,000

- Married filing jointly: $236,000–$246,000

Best for: Self-employed individuals who expect to be in a higher tax bracket at retirement, those who want the option to withdraw contributions (not earnings) before retirement without penalty, or younger professionals who want decades of tax-free compounding.

The Roth IRA pairs well with other self-employed plans as a tax diversification tool. Higher earners above those thresholds can still contribute via a backdoor Roth conversion — a strategy worth discussing with your advisor.

SEP IRA

The SEP IRA (Simplified Employee Pension) is built for self-employed individuals and small business owners who want higher contribution limits without administrative complexity.

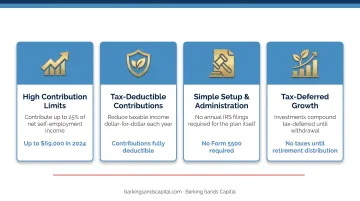

How contributions work: You can contribute up to 25% of net self-employment earnings, capped at $70,000 in 2025 and $72,000 in 2026. Contributions are tax-deductible and grow tax-deferred.

Key advantages for sole proprietors:

- No annual IRS filing requirement (no Form 5500)

- Contributions are flexible — contribute more in profitable years, less (or nothing) in lean ones

- Can be established and funded as late as your tax filing deadline, including extensions

- Setup requires only IRS Form 5305-SEP, a one-page document kept in your records

The employee consideration: If your business has eligible non-owner employees, SEP IRA rules require you to contribute the same percentage of compensation for each of them as you contribute for yourself. A SEP IRA often becomes cost-prohibitive once you add non-owner employees.

Solo 401(k)

The Solo 401(k) — also called a one-participant or self-employed 401(k) — is available to business owners with no employees other than a spouse. It offers the highest contribution ceiling of any self-employed retirement plan.

Why the limits are so high: Contributions come from two sources:

- Employee deferral: Up to $23,500 in 2025 ($24,500 in 2026)

- Employer profit-sharing: Up to 25% of net self-employment compensation

Total 2025/2026 limits:

| Year | Base Limit | Age 50+ Catch-Up | Age 60–63 Catch-Up |

|---|---|---|---|

| 2025 | $70,000 | $77,500 | $81,250 |

| 2026 | $72,000 | $80,000 | $83,250 |

Additional advantages:

- Roth contribution option available within many Solo 401(k) plans

- Plan loans permitted if the plan document allows it

- At lower income levels, the dual contribution formula allows higher contributions than a SEP IRA at the same earnings

Drawbacks to consider:

- Once plan assets exceed $250,000, you must file Form 5500-EZ annually

- Only available when you have no non-spouse employees — hiring even one eligible worker disqualifies you

- Per IRS Publication 560, sole proprietors may adopt a new Solo 401(k) by their tax filing deadline (without extensions) for tax years 2023 and later. Employer contributions can be made up to the filing deadline including extensions

SIMPLE IRA

The SIMPLE IRA (Savings Incentive Match Plan for Employees) is designed for businesses with up to 100 employees — including self-employed sole proprietors who anticipate building a team.

2025/2026 employee contribution limits:

- 2025: $16,500, plus $3,500 catch-up (age 50+), or $5,250 for ages 60–63

- 2026: $17,000, plus $4,000 catch-up (age 50+), or $5,250 for ages 60–63

Employer contribution requirement: Unlike a SEP IRA, you cannot skip employer contributions entirely. Two options apply:

- Match employee deferrals dollar-for-dollar up to 3% of compensation (reducible to 1%, but not for more than 2 out of any 5 years)

- Make a flat 2% non-elective contribution for all eligible employees

Best for: Self-employed individuals who already have employees or plan to hire, want a structured plan to offer staff, and can commit to annual employer contributions.

Critical restriction: Early withdrawals within the first two years of SIMPLE IRA participation carry a 25% penalty — not the standard 10% — making this plan significantly less liquid during the early participation window.

How to Choose the Right Plan for Your Situation

No single plan wins across all scenarios. Four factors determine which structure fits best:

- Income level and consistency — Higher, more stable earnings unlock the real value of SEP IRAs and Solo 401(k)s. At lower income levels, a Traditional or Roth IRA may be sufficient.

- Current vs. future tax bracket — Pre-tax plans (SEP IRA, Solo 401(k), Traditional IRA) benefit those expecting a lower tax rate at retirement. Roth accounts favor those expecting rates to rise.

- Employees now or soon — Solo 401(k) is eliminated as an option the moment you have eligible non-spouse employees. SEP IRA becomes more expensive with each employee added.

- Administrative tolerance — SEP IRAs and IRAs require minimal paperwork. Solo 401(k)s add filing requirements once assets exceed $250,000. SIMPLE IRAs require consistent employer contributions and formal plan documentation.

2025 Plan Comparison

| Plan | 2025 Contribution Limit | Tax Treatment | Best For | Key Limitation |

|---|---|---|---|---|

| Traditional IRA | $7,000 (+$1,000 age 50+) | Pre-tax (if deductible) | Lower income, starting out | Low ceiling; deduction phases out with active plan participation |

| Roth IRA | $7,000 (+$1,000 age 50+) | After-tax; tax-free withdrawals | Higher future bracket, flexibility | Income phase-outs apply |

| SEP IRA | Up to 25% of net earnings, max $70,000 | Pre-tax/deductible | Sole proprietors, high earners | Same % required for all eligible employees |

| Solo 401(k) | $70,000 total (+$7,500 age 50+) | Pre-tax and/or Roth | Owner-only businesses, max savings | No non-spouse employees; Form 5500-EZ at $250K |

| SIMPLE IRA | $16,500 employee deferral (+$3,500 age 50+) | Pre-tax | Businesses with up to 100 employees | Mandatory employer contributions; 25% early withdrawal penalty in year 1–2 |

Layering Multiple Accounts

Contributing to more than one account in the same year is allowed — and often the smarter approach. A self-employed individual can contribute to a Solo 401(k) for high pre-tax savings while simultaneously funding a Roth IRA for tax-free growth, achieving tax diversification across both accounts.

One interaction rule to know: if you're covered by a SEP IRA, Solo 401(k), or SIMPLE IRA, the IRS treats you as an active participant in a workplace plan. This can phase out your ability to deduct Traditional IRA contributions above certain income thresholds. It's also worth checking IRS Publication 560, which clarifies that the IRS model Form 5305-SEP cannot be used if you already maintain another qualified retirement plan — a relevant constraint if you're considering a SEP IRA alongside a Solo 401(k) for the same business.

These interactions get complex quickly. Barking Sands Capital's InteProcess™ coordinates tax, retirement, business, and estate planning through a team-based approach, so retirement account decisions are evaluated within the full context of your tax situation and business trajectory — not in isolation.

Strategies to Maximize Retirement Savings on Variable Income

Fixed monthly contribution amounts work well for salaried employees. For self-employed individuals, they're often the wrong framework.

Use a Percentage-of-Income Target

Commit to saving a set percentage of net income rather than a fixed dollar amount. This approach scales naturally — you contribute more in high-revenue periods and less in lean ones without abandoning the strategy. Targeting 15–20% of net earnings creates a disciplined system built around how self-employment income works.

Take Advantage of the "Feast and Famine" Window

Set aside retirement contributions in a dedicated holding account during strong revenue periods. Then make a lump-sum contribution before the tax deadline.

Deadlines that matter:

- SEP IRA: Can be established and funded up to the tax filing deadline, including extensions (typically October 15 for sole proprietors who file for extensions)

- Solo 401(k): Employer contributions can be made up to the filing deadline including extensions; sole proprietors with no employees can adopt a new plan by the filing deadline without extensions for 2023 and later tax years

- IRAs (Traditional and Roth): Contributions can be made up to the tax filing deadline (April 15, without extensions)

This flexibility means you can see your full-year income before deciding how much to contribute — which removes the guesswork from contribution decisions.

Align Contributions with Quarterly Estimated Taxes

Self-employed individuals already think in quarters because of estimated tax obligations. Scheduling retirement contributions on the same quarterly cycle builds a consistent habit and prevents the end-of-year scramble that leads many to leave unused contribution room behind.

Conclusion

There's no universally right retirement account for self-employed individuals. The best structure depends on your income level, tax situation, whether you have employees, and where you expect to be financially in 20 years. That said, self-employed individuals have a real advantage over employees with fixed employer plans: the ability to combine accounts, adjust contribution amounts annually, and optimize for both current and future tax positions. The challenge is using that flexibility with intention — not just taking the path of least resistance when tax season arrives.

Self-employed professionals who want their retirement accounts working in coordination with their tax, business, and estate planning goals can connect with the team at Barking Sands Capital. As an independent, fee-based RIA, advisors like JB L'Esperance (ChFC) and Andrea Cervena (CFP®) use the firm's proprietary InteProcess™ to evaluate retirement account structures within your full financial picture — not as a standalone decision.

Reach out at 952-500-8854 (Minnesota) or 248-687-1040 (Michigan) to get started.

Frequently Asked Questions

What is the best retirement plan for self-employed people?

There's no single best plan. Solo 401(k)s and SEP IRAs offer the highest contribution limits for higher-income self-employed individuals, while Roth IRAs add tax-free withdrawal flexibility. Many self-employed individuals benefit most from combining two accounts — for example, a Solo 401(k) paired with a Roth IRA — to achieve both high contribution capacity and tax diversification.

What is the $1,000 a month rule for retirement?

The $1,000/month rule is a general guideline suggesting consistent long-term saving can generate meaningful retirement income. It's not a reliable benchmark for self-employed individuals with variable income. A percentage-of-net-income approach is more practical — it scales with your earnings rather than requiring a fixed amount regardless of what your business generates in a given year.

What is the $400 rule for self-employed people?

Per IRS Topic 554, if your net self-employment income equals or exceeds $400 in a year, you must file a tax return and pay self-employment tax (15.3%, covering Social Security and Medicare). This matters for retirement planning because your net self-employment earnings — after deducting the employer-equivalent portion of SE tax — form the basis for calculating maximum contributions to plans like the SEP IRA and Solo 401(k).

Can I contribute to both a SEP IRA and a Solo 401(k) in the same year?

Generally, no — both plans fill the same employer contribution role, and IRS Form 5305-SEP cannot be used alongside another qualified plan. You can, however, pair a Solo 401(k) with a separate Roth or Traditional IRA in the same year. Consult a tax professional before combining plans, as the rules vary by business structure.

When is the deadline to open and fund a self-employed retirement account?

Deadlines vary by account type: Solo 401(k)s must be established by your tax filing deadline (no extensions); SEP IRAs can be opened and funded through your extended deadline, typically October 15; IRA contributions are due by April 15. Missing these windows means losing that year's contribution opportunity entirely.

How does self-employment tax affect retirement contributions?

Self-employed individuals pay the full 15.3% self-employment tax, covering both the employer and employee shares of Social Security and Medicare. You can deduct half of this SE tax when calculating your net earnings — which reduces the earned income base used to determine maximum contribution amounts for plans like the SEP IRA and Solo 401(k).