This guide is for two audiences: individuals mapping a path to financial independence, and small business owners exploring employer-sponsored retirement plans. You'll find the five core selection criteria, the exact questions to ask every candidate, and the red flags that should end the conversation immediately.

Key Takeaways

- Fiduciary status is non-negotiable. Confirm it in writing before signing anything.

- Credentials like CFP®, ChFC, and CRPS signal real training — "financial advisor" alone carries no legal weight.

- Fee structure determines whose interests the advisor is actually serving.

- Verify every candidate through FINRA BrokerCheck and the SEC's IAPD before deciding.

- The right consultant integrates retirement planning with tax, insurance, and estate strategy, not investments alone.

What Is a Retirement Plan Consultant?

A retirement plan consultant is a financial professional who specializes in designing, implementing, and monitoring retirement strategies — distinct from a general financial advisor by their focused expertise in tax-advantaged accounts, plan compliance, and income distribution planning.

People hire retirement plan consultants in two primary contexts:

- As an individual or family — mapping a path to financial independence, optimizing Social Security, and building a tax-efficient drawdown strategy.

- As a business owner or plan sponsor — setting up and managing employer-sponsored plans like a 401(k), SEP-IRA, or SIMPLE IRA, including employee education and regulatory compliance.

Core Services a Retirement Plan Consultant Provides

A qualified consultant goes well beyond picking investments. Expect the scope to include:

- Retirement income analysis: projecting sustainable withdrawal rates and income gaps

- Investment selection and portfolio management: building and rebalancing a strategy aligned to your timeline

- Social Security optimization: analyzing claiming ages and spousal coordination strategies

- Tax-efficient withdrawal planning: sequencing distributions across taxable, tax-deferred, and Roth accounts

- For employers: plan design, employee enrollment education, and regulatory compliance oversight

A qualified consultant treats retirement planning as part of a broader financial picture, not an isolated exercise. Firms like Barking Sands Capital use a proprietary framework — their InteProcess™ — that coordinates legal, insurance, tax, retirement, and financial planning professionals into one integrated strategy.

That cohesion is what separates good retirement planning from great retirement planning. A tax decision made in isolation can undermine an income plan; an estate planning change can quietly affect insurance coverage.

What to Consider When Choosing a Retirement Plan Consultant

The right consultant depends on your life stage, financial complexity, and specific goals. A 35-year-old small business owner needs a different profile than someone three years from retirement. The factors below connect a consultant's technical profile to real outcomes for your financial security.

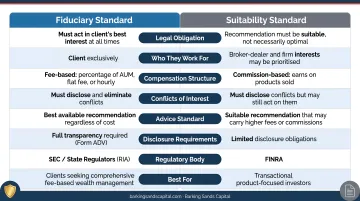

Fiduciary Status and Independence

This is where the selection process should start. Two standards govern how financial professionals treat client interests:

- Fiduciary standard — The advisor is legally obligated to act in your best interest at all times, disclosing all conflicts of interest.

- Suitability standard — The broker only needs to recommend products that are "appropriate" for you, not necessarily optimal. Higher fees or commissions that benefit the advisor are permitted under this standard.

The SEC confirms that an investment adviser's fiduciary duty under the Investment Advisers Act of 1940 comprises both a duty of care and a duty of loyalty. This is a materially higher standard than broker suitability rules under FINRA Rule 2111 — worth understanding before you sign anything.

An independent Registered Investment Advisor (RIA) structure removes the commission conflict: RIAs cannot receive commissions on managed accounts, so their compensation comes directly from clients rather than product sales. Barking Sands Capital is structured this way by design. JB and Kelly L'Esperance founded the firm specifically because they refused to push products that didn't align with client needs at their previous employers.

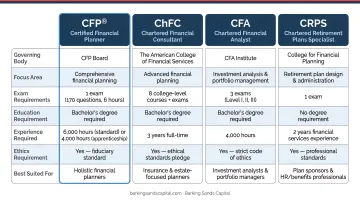

Credentials and Professional Designations

The title "financial advisor" is unregulated — anyone can use it. What actually signals competence and accountability is a verified professional designation.

| Designation | What It Requires |

|---|---|

| CFP® (Certified Financial Planner) | Coursework, 170-question exam, 6,000 hours experience, 30 hours CE every 2 years |

| ChFC (Chartered Financial Consultant) | 8 courses, course-level exams, 3 years experience, 30 hours CE every 2 years |

| CFA (Chartered Financial Analyst) | 3-level exam series, 4,000 hours qualifying work experience over 36+ months |

| CRPS (Chartered Retirement Plans Specialist) | Self-study course, closed-book exam, 16 hours CE every 2 years |

Always verify credentials directly through the issuing organization's directory — not just by taking the advisor's word for it. The CFP Board's verification tool and FINRA's professional designations database both offer free lookups.

Barking Sands Capital's team holds both a ChFC (JB L'Esperance) and a CFP® (Andrea Cervena), covering the core competencies in retirement planning and comprehensive financial strategy.

Relevant Specialization and Experience

A consultant who primarily works with corporate pension plans is not the same resource as one who has spent years designing cash-balance plans for small business owners. Specialization matters.

Ask specifically:

- What types of clients make up the majority of your practice?

- Can you describe a situation similar to mine and how you approached it?

- Have you handled [SEP-IRA / pre-retirement distribution / business succession] scenarios before?

For business owners in particular, look for demonstrated experience with small business plan structures. Barking Sands Capital specifically offers cash-balance plan consulting for business owners — an advantage generalist advisors rarely offer.

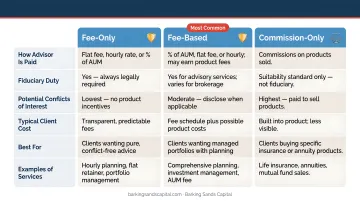

Fee Structure and Transparency

Three compensation models exist. Understanding which one your candidate uses is essential:

- Fee-only — Flat fee, retainer, or percentage of AUM. No commissions, ever. Highest alignment with client interests.

- Fee-based — Combination of fees and commissions. Conflicts are possible but must be disclosed.

- Commission-only — Paid when products are sold. Highest risk of conflicted advice.

For context on market rates: AdvisoryHQ's 2023 advisor fee study found AUM fees typically ranging from 0.59% to 1.18%, with a 1.02% median for a $1 million portfolio. Annual retainers generally run $6,000 to $11,000, and hourly rates fall between $120 and $300.

Request a written fee schedule before engaging anyone. If a consultant won't provide one in writing, that reluctance itself is a red flag worth taking seriously before committing.

Communication Style and Ongoing Availability

An advisor who meets with you once a year and disappears during market disruptions or major life events is not delivering full value. Clarify before signing:

- How often will we meet formally?

- What's your response time for questions between meetings?

- Who handles my account if you're unavailable or leave the firm?

The third question is the one most people skip. A firm with a structured client relationship management function — like Barking Sands Capital's dedicated Client Relationship Manager role — provides continuity that a solo practitioner cannot always guarantee.

Key Questions to Ask a Retirement Plan Consultant Before You Hire

A structured interview separates a well-matched consultant from one who simply interviews well. These five questions surface how an advisor actually operates.

1. "Are you a fiduciary, and will you put that in writing?" Any qualified, client-first consultant answers yes without hesitation and includes the fiduciary commitment in the engagement agreement. Any hesitation — or a refusal to formalize it in writing — tells you what you need to know.

2. "How are you compensated, and do you receive any third-party fees or commissions?" Ask this as a direct follow-up to the fiduciary question. You're confirming that stated values and actual incentive structure align. Request full disclosure of all revenue streams.

3. "What does your investment philosophy look like, and how does it apply to my specific situation?" This reveals whether the consultant customizes their approach or defaults to a generic strategy regardless of who's in the room. Good answers reference your risk tolerance, time horizon, and specific goals — not generic market narratives.

4. "What credentials do you hold, and how do you stay current with regulatory and tax law changes?" Advisors who cannot speak specifically to recent developments — for example, SECURE 2.0 Act changes to RMD ages (now 73, rising to 75 in 2033) or the new Roth catch-up contribution rules finalized in 2025 — are not current enough to advise you accurately.

5. "Who handles my account if you leave the firm or retire, and how will I be notified?" Retirement planning spans decades. A reputable firm has a formal succession and client transition protocol in place before this situation arises.

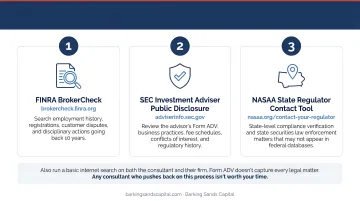

How to Verify a Consultant's Background Before Making a Final Decision

Background verification is not optional. Under ERISA, plan sponsors are legally required to conduct prudent due diligence when selecting advisors for employer retirement plans. This applies to anyone hiring an advisor — not just institutional plan sponsors.

Use these three free tools before making any final decision:

FINRA BrokerCheck (brokercheck.finra.org) — Search employment history, registrations, customer disputes, and any disciplinary actions going back 10 years.

SEC Investment Adviser Public Disclosure (adviserinfo.sec.gov) — Review the advisor's Form ADV, which discloses business practices, fee schedules, conflicts of interest, and regulatory history.

NASAA State Regulator Contact Tool (nasaa.org/contact-your-regulator) — For state-level compliance verification and any state securities law enforcement matters that may not appear in federal databases.

Also run a basic internet search on both the consultant and their firm. Form ADV doesn't capture every legal matter. Any consultant who pushes back on this process isn't worth your time.

How Barking Sands Capital Can Help

JB and Kelly L'Esperance founded Barking Sands Capital in 2004 after leaving larger financial organizations — both had grown frustrated pushing products that didn't fit their clients' actual needs. The firm was structured from day one around fee-based compensation, independent custody, and coordinated planning across legal, tax, insurance, and retirement disciplines.

What that looks like in practice:

- No commissions on managed accounts. As an independent RIA, compensation is transparent and fully disclosed.

- JB L'Esperance holds a ChFC designation; Andrea Cervena holds a CFP®. The full team carries Series 7, Series 63, Series 6, and Life/Health licenses across Michigan and Minnesota.

- Proprietary InteProcess™ — Integrates legal, insurance, tax, retirement, and financial planning into a single coordinated strategy rather than siloed services.

- Client assets are held with independent custodians — Altruist, Pershing, and Schwab — maintaining a clear separation between advisory services and asset custody.

- Over 20 years of experience — The firm has navigated the 2008 financial crisis, the 2020 pandemic collapse, and the 2021 inflation surge — not just bull markets.

If you're ready to talk through your retirement planning situation, reach out directly:

- Minnesota: 952-500-8854

- Michigan: 248-687-1040

- Email: jb@barkingsandscapital.com

Conclusion

Selecting a retirement plan consultant is not about finding the most recognized name or the lowest fee. It is about finding someone whose credentials, incentive structure, communication style, and planning philosophy genuinely align with your retirement goals.

The right consultant typically checks these boxes:

- Holds a fiduciary duty to act in your best interest

- Operates on a fee-based model with transparent compensation

- Communicates proactively — not just when you ask

- Integrates retirement planning with your broader financial picture

- Has a clear process for reviewing and updating your plan over time

Hiring a consultant is also the start of a long-term relationship, not a one-time transaction. Review performance periodically, update your goals as life changes, and pay attention to whether your consultant proactively initiates those conversations — or waits to be asked. That distinction tells you more than any credential check.

If you're looking for a fee-based, independent advisor who integrates retirement planning with comprehensive financial coordination, Barking Sands Capital works with individuals, families, and small business owners across Minnesota and Michigan — with no commissions and no product-pushing.

Frequently Asked Questions

What are the 3 C's of selecting a financial advisor?

The 3 C's are Credentials (verified designations and regulatory registration), Compensation (transparent disclosure of all fee sources), and Character (fiduciary commitment and a clean disciplinary record). Together, they give you a reliable framework for vetting any advisor before you commit.

What is the difference between a fiduciary and a non-fiduciary financial advisor?

A fiduciary is legally obligated to act in your best interest at all times and must disclose all conflicts of interest. A non-fiduciary broker follows only a suitability standard — they can recommend products that are broadly appropriate even if higher fees or commissions make those products better for the advisor than for you.

What credentials should a retirement plan consultant have?

The most respected designations are CFP®, ChFC, CFA, and CRPS. Each requires significant coursework, examinations, relevant experience, and ongoing continuing education. Always verify credentials independently through the issuing organization's directory — the title "financial advisor" itself carries no credential requirements.

How much does a retirement plan consultant typically charge?

Fee-only advisors typically charge either a percentage of assets under management (commonly 0.59%–1.18% annually) or an annual retainer (generally $6,000–$11,000). Hourly rates typically range from $120–$300. Commission-only arrangements carry the highest conflict risk and should be approached with caution.

What is Form ADV and why should I review it before hiring an advisor?

Form ADV is the SEC registration document all Registered Investment Advisors must file and update annually, disclosing fee schedules, business practices, conflicts of interest, and disciplinary history. Pull it from the SEC's IAPD portal (adviserinfo.sec.gov) before your first meeting — it's one of the most valuable due diligence tools available.

How often should I meet with my retirement plan consultant?

At minimum, plan for quarterly check-ins to review investment performance and adjust strategy. Additional meetings are warranted by major life events — job changes, inheritances, divorce, or approaching retirement — and by significant market shifts. A good consultant initiates these conversations proactively rather than waiting for you to schedule them.