Traditional tax planning and strategic tax planning may sound interchangeable, but they differ in scope, timing, and long-term impact. That distinction matters most for small business owners, high earners, and anyone approaching a major financial transition. Understanding where you fall on that spectrum is the first step toward keeping more of what you earn.

Key Takeaways

- Traditional tax planning is reactive — it ensures accurate, on-time filing but doesn't actively reduce your tax burden throughout the year

- Strategic tax planning is proactive, integrating tax decisions with business structure, investments, retirement, and estate goals year-round

- The key differentiator is timing: traditional planning responds after the tax year ends; strategic planning works continuously before and throughout it

- Effective strategic planning draws on multi-disciplinary expertise across law, investment management, retirement strategy, and estate planning — not just tax preparation

- Those with business income, growing assets, or complex financial situations stand to benefit most from a strategic approach

Strategic Tax Planning vs. Traditional Tax Planning: At a Glance

Here's how these two approaches compare across the dimensions that matter most:

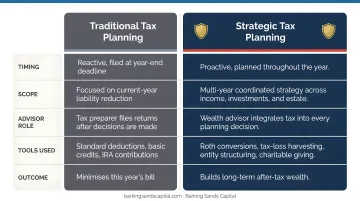

| Dimension | Traditional Tax Planning | Strategic Tax Planning |

|---|---|---|

| Timing | Reactive, year-end | Proactive, year-round |

| Scope | Compliance, deductions, credits | Holistic financial picture |

| Primary Goal | Accurate filing | Minimize lifetime tax burden |

| Advisor Type | CPA or tax preparer | Multi-disciplinary advisor or team |

| Integration | Standalone tax activity | Connected to retirement, estate, and investment planning |

Neither approach is inherently wrong. The right fit depends on your financial complexity — and that gap widens significantly once retirement accounts, business interests, or estate planning enter the picture.

What Is Traditional Tax Planning?

Traditional tax planning is the process of reviewing financial records at or near year-end to ensure returns are filed accurately, standard deductions are captured, and compliance obligations are met. It's reactive by design — it looks backward at what already happened.

What It Typically Includes

- Claiming eligible deductions: mortgage interest, charitable contributions, and business expenses

- Making last-minute IRA contributions before the April 15 filing deadline to reduce taxable income

- Reviewing all income sources to ensure accurate reporting

- Capturing credits and carryforwards that apply to the current year

For context, IRS Statistics of Income data for tax year 2022 shows that roughly 12.2 million returns claimed charitable contribution deductions totaling $222 billion — the kind of year-end activity that defines traditional planning.

Its Core Limitation

Because traditional planning occurs after most financial decisions have already been made, the window to meaningfully reduce tax liability is narrow. Strategies like restructuring income, timing large purchases, or repositioning investments are simply no longer available once December 31 passes. At that point, you're working with what you have, not what you could have arranged with earlier action.

AICPA data found that 45% of tax-filing Americans didn't know when they last updated their withholding — a clear sign that active, year-round tax management isn't the norm.

What Is Strategic Tax Planning?

Strategic tax planning is a year-round process that looks at a client's complete financial picture: income, investments, business structure, compensation, estate plan, and retirement goals. The goal is to make the most tax-efficient decisions possible at every stage. Not just at filing time.

Forward-Looking by Design

Unlike traditional planning, strategic tax planning identifies tax-saving opportunities before they expire. It structures financial decisions to reduce future liability and aligns tax strategy with long-term objectives. A Roth conversion completed in January looks entirely different from one rushed in December — the timing affects not just this year's taxes, but potentially Medicare premiums two years from now.

A Much Broader Scope

Strategic tax planning goes well beyond deductions and credits. It encompasses:

- Business entity structure — choosing between sole proprietorship, LLC, S-corp, or C-corp based on tax implications, not just operational convenience

- Executive and owner compensation — optimizing the mix of salary, distributions, and benefits to minimize employment taxes

- Retirement account selection and funding — defined contribution plans allow up to $72,000 in contributions for 2026, far exceeding standard IRA limits

- Capital gains management — including tax-loss harvesting, which Vanguard research estimates can add up to 1.27% in annualized after-tax returns under optimal implementation

- Estate planning coordination — ensuring wealth transfer decisions align with tax strategy

- Asset protection and succession planning — especially for business owners approaching a transition

A change in one area routinely affects several others. When multiple specialists work in isolation, those connections get missed — and that's where tax savings slip through the cracks.

Why It Requires More Than a CPA

Strategic tax planning isn't a standard CPA service. It requires someone who understands how tax decisions intersect with investment management, retirement planning, legal structures, and estate strategy. A CPA focused on compliance is indispensable — but they're typically not reviewing your capital gains exposure alongside your Medicare surcharge risk or your business succession timeline.

Barking Sands Capital addresses this through its proprietary InteProcess™, which embeds tax strategy directly into the financial planning process. Rather than treating taxes as a year-end task, it coordinates tax decisions alongside retirement planning, estate planning, insurance, and investment management as one connected whole.

Key Differences Between Strategic and Traditional Tax Planning

Timing and Posture

Traditional planning is reactive — it responds to what already happened. Strategic planning is proactive. Financial decisions are made with tax consequences in mind throughout the year, allowing for income deferral, expense acceleration, and structural adjustments that simply aren't available after December 31.

Scope of Coverage

Traditional planning focuses narrowly on income, deductions, and credits. Strategic planning covers:

- Business structure optimization

- Retirement account strategy and funding

- Capital gains management and tax-loss harvesting

- Estate planning coordination

- Tax implications of major life events — a business sale, inheritance, or ownership transition

Financial Impact Over Time

This is where the difference compounds. Traditional planning helps you avoid overpaying in the short term. Strategic planning builds cumulative advantage over years.

The compounding effect shows up across several strategies:

- Asset location: Vanguard estimates strategic asset location alone adds 5 to 30 basis points of after-tax return annually

- Tax-loss harvesting: Offsets gains systematically rather than reactively at year-end

- Roth conversions: Timed correctly, they reduce future taxable income during peak earning years

- Retirement contributions: Optimized funding reduces current-year tax exposure while building long-term wealth

Stack these together over 20 years, and the gap in net worth can reach six figures.

For high earners, the stakes are higher still. The 2025 top federal bracket of 37% kicks in above $626,350 for single filers. At that level, every unplanned dollar of income is expensive.

Integration with Your Overall Financial Plan

Traditional planning operates in isolation. It doesn't account for how a Roth conversion might trigger Medicare's income-related monthly adjustment amount (IRMAA) — which is calculated based on your tax return from two years prior. It doesn't consider how selling a business asset reshapes your estate plan.

Strategic planning treats every financial decision as interconnected. That integration is especially critical for small business owners, those approaching retirement, and high-net-worth individuals navigating multiple income streams.

Which Approach Is Right for You?

Traditional Planning Is Sufficient When

- You have a single income source with standard deductions

- You don't own a business or have significant investment holdings

- Your financial situation is relatively straightforward

For this group, an annual review with a CPA ensures compliance and captures common deductions. That's all that's needed.

Strategic Planning Makes Sense When

You fall into one or more of these profiles:

- Small business owners — especially pass-throughs, where 83% of small businesses operate and where entity structure, owner compensation, and retirement plan design all carry significant tax implications

- Multiple income streams or significant investment portfolios — where capital gains management, asset location, and tax-loss harvesting add measurable after-tax value

- Higher tax brackets — where unplanned income triggers the steepest tax bills

- Those approaching retirement — where Roth conversions, IRMAA exposure, and distribution sequencing all interact in ways that require advance planning

- Anyone with estate planning needs or a pending major financial transition — a business sale, inheritance, or property transfer that touches multiple planning areas at once

For these individuals, reactive compliance-only planning leaves meaningful money on the table. That's where a more integrated advisory relationship makes the difference.

How Barking Sands Capital Fits In

Barking Sands Capital's InteProcess™ is built specifically for clients who recognize they need more than a tax return. The framework coordinates each major planning area under one advisory relationship:

- Tax strategy aligned with investment decisions

- Retirement planning and distribution sequencing

- Estate coordination and asset protection

- Insurance coverage reviewed alongside financial goals

If your financial picture has grown beyond what a single annual filing can optimize, that's the conversation worth having. Contact the Barking Sands Capital team at 952-500-8854 (Minnesota) or 248-687-1040 (Michigan) to explore whether a more integrated approach fits where you are.

Frequently Asked Questions

What is strategic tax planning?

Strategic tax planning is a proactive, year-round process that integrates tax decisions with business structure, investments, retirement goals, and estate planning. The objective is minimizing your lifetime tax burden — not just ensuring accurate annual filing.

Is hiring a tax strategist worth it?

For individuals with business income, significant assets, or complex financial situations, yes — typically by a wide margin. The savings from coordinated Roth conversions, entity optimization, and capital gains management typically far exceed the cost of the service.

What is the difference between a tax planner and a tax strategist?

A tax planner typically focuses on compliance and deductions within the current tax year. A tax strategist takes a multi-year, holistic view — designing structures and strategies that reduce tax liability across your entire financial picture over time.

Can traditional and strategic tax planning be used together?

They're not mutually exclusive — compliance (traditional planning) is always necessary. Strategic planning layers on top, ensuring every compliance decision fits within a broader framework designed to reduce your total tax burden.

When should I start strategic tax planning?

The earlier in the year — and the earlier in your financial journey — the more options you have. Income timing, entity structuring, and retirement contributions must be put in place before year-end to be effective.

What does strategic tax planning include beyond deductions and credits?

Key areas include:

- Business entity structure and owner compensation design

- Retirement account selection and funding

- Capital gains and tax-loss harvesting management

- Estate planning, asset protection, and succession planning

Each area is considered as part of a connected whole, not in isolation.