This guide is for adults nearing 65, retirees transitioning off employer coverage, and anyone already enrolled who wants to switch or disenroll from a plan. We'll cover every major enrollment window, the step-by-step enrollment process, how to disenroll properly, and the mistakes that cost people the most money.

The stakes are real: The 2026 standard Part B premium is $202.90 per month. Miss your enrollment window without qualifying coverage, and that number goes up—permanently.

Key Takeaways

- Medicare enrollment is not automatic for everyone—timing depends on age, employment status, and whether you have qualifying coverage

- There are four main enrollment windows: IEP, AEP, MA OEP, and Special Enrollment Periods

- Missing your enrollment window without qualifying coverage results in permanent late-enrollment penalties for Part B and Part D

- Switching from Medicare Advantage back to Original Medicare is possible, but only during designated annual windows

- Medicaid eligibility can unlock additional enrollment opportunities for qualifying low-income individuals

Understanding Medicare and Medicaid Plan Types

Medicare has four parts, and each one has its own enrollment rules:

| Part | What It Covers |

|---|---|

| Part A | Hospital insurance: inpatient care, skilled nursing, hospice, some home health |

| Part B | Medical insurance: doctor visits, outpatient care, preventive services |

| Part C | Medicare Advantage: private plans bundling Parts A and B (usually including D) |

| Part D | Prescription drug coverage |

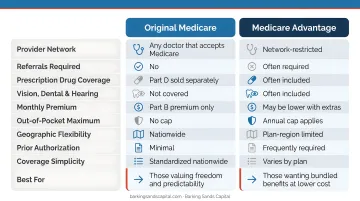

Original Medicare vs. Medicare Advantage

Original Medicare (Parts A and B) is managed directly by the federal government. You can use any provider who accepts Medicare nationwide, and you add optional Part D drug coverage and a Medigap supplement separately.

Medicare Advantage (Part C) comes from private insurers approved by CMS. These plans bundle Parts A and B—and usually Part D—into one plan, often adding dental, vision, and hearing benefits. According to KFF, 35 million people, or 55% of eligible Medicare beneficiaries, are enrolled in Medicare Advantage in 2026.

The enrollment and disenrollment rules differ significantly between these two structures—knowing which applies to you determines which windows you have to act, and when you can switch.

Where Medicaid Fits In

Medicaid is a separate, state-administered program for people with limited income and resources. People who qualify for both Medicare and Medicaid are called dual-eligible individuals. Dual eligibility opens up several advantages:

- Access to Special Enrollment Periods outside standard windows

- Reduced or eliminated cost-sharing on Medicare services

- Eligibility for Dual Eligible Special Needs Plans (D-SNPs), a category of Medicare Advantage designed specifically for this population

Understanding whether you qualify as dual-eligible is worth confirming early—it can meaningfully expand your enrollment options.

Key Medicare Enrollment Periods You Need to Know

Initial Enrollment Period (IEP)

Your IEP is a 7-month window centered on your 65th birthday: the 3 months before your birthday month, your birthday month itself, and the 3 months after.

During this window, you can sign up for Parts A, B, and D. Missing it without qualifying employer coverage triggers a permanent Part B penalty—10% added to your monthly premium for each full 12-month period you delayed (per Medicare's penalty guidelines). At $202.90 per month in 2026, even a one-year delay adds roughly $20 per month for life.

When you enroll in Part B, you also have your Initial Coverage Election Period (ICEP) for Medicare Advantage. MA coverage cannot start before both Parts A and B are active.

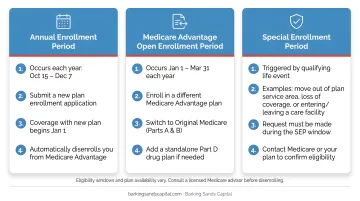

Annual Enrollment Period (AEP)

- Dates: October 15 – December 7 each year

- Who it's for: Anyone with Medicare

- What you can do: Join, switch, or drop a Medicare Advantage or Part D plan

- When changes take effect: January 1 of the following year

This is the primary opportunity for most enrollees to make plan changes. Don't skip it—plans change every year.

Medicare Advantage Open Enrollment Period (MA OEP)

- Dates: January 1 – March 31 each year

- Who it's for: People already enrolled in a Medicare Advantage plan

- What you can do: Switch to a different MA plan, or return to Original Medicare and join a separate Part D plan

Keep in mind: the MA OEP is not an opportunity for people already in Original Medicare to join or switch a stand-alone Part D plan. That window is limited to MA enrollees making a change.

Special Enrollment Periods (SEPs) for Workers

If you delayed Part B because you had employer group health coverage, you receive an 8-month SEP after that coverage ends—either through retirement or job loss—to enroll in Part B without penalty. Your ICEP for Medicare Advantage runs concurrently.

Enroll in Part B just before retirement rather than waiting until the SEP starts. Waiting, even briefly, can create a gap in coverage between your employer plan ending and Medicare beginning.

How to Enroll in a Medicare or Medicaid Plan

Step 1: Confirm Your Eligibility

Medicare eligibility generally starts at 65 for those with at least 40 quarters (10 years) of work credits paying into Social Security. Earlier eligibility applies for people with qualifying disabilities (after a 24-month SSDI waiting period) or end-stage renal disease.

Verify your eligibility at SSA.gov or by calling Social Security directly.

Step 2: Choose Between Original Medicare and Medicare Advantage

Your choice here shapes everything downstream — provider access, drug coverage, and costs. Here's a quick comparison:

| Factor | Original Medicare | Medicare Advantage |

|---|---|---|

| Provider access | Any Medicare-accepting provider | Network-restricted (usually) |

| Drug coverage | Add Part D separately | Usually bundled |

| Supplemental benefits | None | Often includes dental, vision |

| Medigap availability | Yes, with full protections during OEP | Medigap protections may not apply later |

| Travel flexibility | Strong | Varies by plan |

The right choice depends on your prescriptions, doctors, budget, and travel habits. It's also worth factoring in IRMAA surcharges, which can increase your Part B and Part D premiums based on income — a detail that's easy to overlook without a broader retirement income review. Curtis Hewitt at Barking Sands Capital specializes in Medicare Planning and can help you work through these tradeoffs in context.

Step 3: Compare and Select a Plan

Use Medicare's Plan Compare tool at medicare.gov during your enrollment window. Compare:

- Monthly premiums and annual deductibles

- Provider network (confirm your doctors are in-network)

- Drug formulary (confirm your prescriptions are covered)

- Star ratings (Medicare's quality score for each plan)

- Out-of-pocket maximums

Plans vary by ZIP code. The same plan can have different costs and networks across counties.

Step 4: Submit Your Enrollment Application

You can enroll through any of these channels:

- Medicare.gov to enroll in Parts A and B through Social Security

- The plan's website directly for Medicare Advantage and Part D plans

- 1-800-MEDICARE for phone enrollment

- A paper form submitted to CMS

Coverage typically starts the first of the month following enrollment during most periods.

Step 5: Apply for Medicaid Through Your State Agency

If you're enrolling in Medicaid — or you qualify for both Medicare and Medicaid — the process is separate. Medicaid is administered at the state level, not through Medicare.gov. Apply through your state's Medicaid agency or use healthcare.gov to find local assistance. Dual-eligible individuals should also ask about D-SNPs, which may offer lower cost-sharing and additional coordinated care benefits.

How and When to Disenroll or Switch Your Plan

Your Disenrollment Windows

- AEP (Oct. 15 – Dec. 7): Drop or switch any Medicare Advantage or Part D plan; changes effective January 1

- MA OEP (Jan. 1 – Mar. 31): Switch MA plans or return to Original Medicare

- SEPs: Mid-year changes when qualifying life events occur (moving out of a plan's service area, losing employer coverage, gaining Medicaid eligibility, etc.)

How to Formally Disenroll

There are three legitimate ways to leave a Medicare Advantage plan:

- Enroll in a new MA plan — you're automatically disenrolled from the old one

- Return to Original Medicare during the MA OEP or AEP

- Use an applicable SEP if a qualifying life event occurs

Stopping premium payments is not a valid disenrollment method. CMS guidance indicates that non-payment may eventually result in plan-initiated involuntary disenrollment after a grace period, but this is not a clean exit and can cause coverage complications.

The Medigap Timing Trap

Beyond the mechanics of disenrollment, there's a longer-term risk worth understanding before you make any plan changes.

When you first enroll in Medicare Part B, you have a 6-month Medigap Open Enrollment Period during which insurers cannot deny coverage based on your health status. This is a one-time window.

If you join a Medicare Advantage plan first and later return to Original Medicare, you may lose those guaranteed-issue Medigap protections depending on your state's rules. In most states, insurers can apply medical underwriting when you try to buy a Medigap plan outside of this initial window.

For many people, this means a pre-existing condition could result in higher premiums or outright denial — so consulting a Medicare advisor before leaving an MA plan is worth the time.

What Happens If You Miss All Windows

If none of these windows apply to your situation, you stay in your current plan until the next AEP. Your coverage continues uninterrupted, but you're locked into that plan's premiums, formulary, and network until January 1 of the following year.

Common Enrollment Mistakes That Can Cost You

Assuming Enrollment Is Automatic

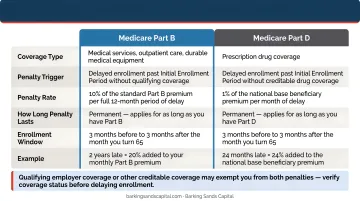

Part A is typically automatic for Social Security recipients—but Part B is not. Many people unknowingly delay Part B enrollment without valid employer coverage. The result: a 10% premium surcharge per 12-month delay period, for life. With the 2026 Part B premium at $202.90, two years of delay means paying roughly $40 extra every month indefinitely.

Part D carries a similar penalty: 1% of the national base beneficiary premium ($38.99 in 2026) for each month without creditable coverage, permanently added to your premium.

Not Reviewing Plans During AEP

KFF found that 69% of Medicare beneficiaries did not compare their current plan with other options during open enrollment. That's a costly habit. Plans change every year—premiums shift, formularies drop drugs, and networks drop providers. Auto-renewing without a review means you might be paying more for less starting every January 1.

Making the MA vs. Medigap Decision Without Guidance

Choosing Medicare Advantage can feel like the lower-cost option initially. But if you later want to return to Original Medicare with Medigap coverage, you may face medical underwriting, meaning an insurer can charge you more or deny coverage based on your health history. That option narrows significantly as you age.

A Medicare planning specialist can walk through both paths before you commit. Barking Sands Capital's advisors fold Medicare enrollment into your broader retirement income strategy, including IRMAA planning to keep your retirement income from quietly inflating your premiums.

Frequently Asked Questions

What happens if I miss my Medicare Initial Enrollment Period?

Missing your IEP without qualifying coverage means waiting for the General Enrollment Period (January 1 – March 31) to sign up for Part B, with coverage starting the month after you enroll. You'll also likely face a permanent late-enrollment penalty added to your monthly premium for as long as you have Part B.

Can I switch from Medicare Advantage back to Original Medicare?

Yes. You can return to Original Medicare during the MA OEP (January 1 – March 31) or the AEP (October 15 – December 7). Be aware that switching may affect your ability to get Medigap coverage at standard rates, depending on your state's guaranteed-issue rules.

How does Medicaid affect my Medicare plan enrollment?

Dual eligibility—qualifying for both Medicare and Medicaid—can open access to Special Enrollment Periods, lower cost-sharing, and D-SNPs. Medicaid also typically helps cover Medicare premiums and out-of-pocket costs for qualifying low-income individuals.

What qualifies me for a Special Enrollment Period?

Common qualifying events include:

- Moving out of a plan's service area

- Losing employer or union coverage

- Becoming eligible for Medicaid or Extra Help/Low Income Subsidy

- Moving into or out of a skilled nursing facility

Most plan-change SEPs provide a 2-month window to act.

Will I face a penalty for delaying Medicare Part B or Part D enrollment?

Yes—unless you have qualifying creditable coverage like active employer group insurance. Part B delays add 10% per 12-month period without coverage, permanently. Part D delays add 1% of the national base beneficiary premium ($38.99 in 2026) per uncovered month, and that penalty is also permanent.

When is the best time to review my Medicare plan options?

Review your plan every September when your Annual Notice of Change (ANOC) arrives—before the AEP opens October 15. This gives you time to compare options on Medicare's Plan Finder and make an informed switch before the December 7 deadline.