It's a legal, two-step workaround that's been used for years to access Roth's tax-free growth benefits regardless of income. No special account required — just two transactions and the right paperwork.

This guide covers what the backdoor Roth IRA is, who it's for, the 2025 and 2026 income thresholds, how to execute it step by step, and the tax pitfalls that catch people off guard.

Key Takeaways

- A backdoor Roth IRA is a two-step process — nondeductible traditional IRA contribution, then a Roth conversion — not a separate account type

- No income ceiling exists on backdoor Roth conversions, even above $500,000

- The pro-rata rule creates taxable complications if you hold pre-tax IRA balances elsewhere

- IRS Form 8606 must be filed every year you use this strategy

- Complete the conversion by December 31 — the IRS taxes conversions by calendar year, not tax filing deadline

What Is a Backdoor Roth IRA and Who Is It For?

The backdoor Roth IRA isn't a distinct account — it's a strategy. You make a nondeductible, after-tax contribution to a traditional IRA, then convert that account to a Roth. The legal foundation is simple: while direct Roth contributions are income-restricted, anyone can convert a traditional IRA to a Roth regardless of income level. The Tax Increase Prevention and Reconciliation Act of 2005 eliminated income limits on Roth conversions beginning in 2010, creating the opening that makes this strategy work.

Why the Roth Matters Enough to Bother

The Roth IRA offers three advantages that matter most to high earners:

- Contributions grow without annual tax drag — no taxes owed on gains year over year

- Qualified withdrawals in retirement are completely tax-free

- No required minimum distributions (RMDs) during the account holder's lifetime, unlike traditional IRAs and 401(k)s

Traditional IRAs, by contrast, defer taxes rather than eliminate them. Every dollar you withdraw in retirement gets taxed as ordinary income. For someone projecting a high income in retirement — or one that stays high — paying taxes now at a known rate beats paying them later at an unknown one.

Who Benefits Most

This strategy is most useful for people whose modified adjusted gross income (MAGI) exceeds the IRS phase-out thresholds — professionals, dual-income households, and small business owners in peak earning years. For Barking Sands Capital's Midwest client base, this commonly includes physicians, engineers, and business owners in Minnesota and Michigan who've outgrown direct Roth eligibility.

A non-working spouse can also use this strategy. As long as the couple files jointly and the working spouse has sufficient earned income, both spouses can each make a nondeductible IRA contribution and convert separately.

One important distinction: a standard Roth conversion moves pre-tax traditional IRA funds — fully taxable at conversion. The backdoor method uses after-tax contributions, so the conversion itself is typically not taxable, except for earnings that accrued between contribution and conversion.

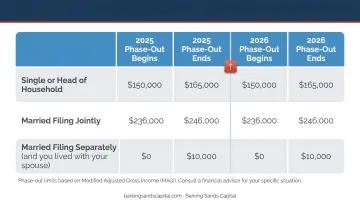

Backdoor Roth IRA Income Limits for 2025 and 2026

The limits below apply to direct Roth IRA contributions only — not to backdoor conversions, which have no income ceiling.

Direct Roth IRA Contribution Phase-Out Ranges

| Filing Status | 2025 MAGI Range | 2026 MAGI Range |

|---|---|---|

| Single / Head of Household | $150,000 – $165,000 | $153,000 – $168,000 |

| Married Filing Jointly | $236,000 – $246,000 | $242,000 – $252,000 |

| Married Filing Separately | $0 – $10,000 | $0 – $10,000 |

Source: IRS Notice 2025-67, 2026 Amounts Relating to Retirement Plans and IRAs

Above the top of the range, direct contributions are completely phased out. The backdoor strategy is designed for people who exceed these thresholds — and the contribution limits below apply regardless of which approach you use.

Annual IRA Contribution Limits

| Tax Year | Base Limit | Age 50+ Catch-Up | Total (Age 50+) |

|---|---|---|---|

| 2025 | $7,000 | $1,000 | $8,000 |

| 2026 | $7,500 | $1,100 | $8,600 |

These limits apply across all IRA accounts combined — not per account. Contributions also cannot exceed your earned income for the year.

The backdoor Roth contribution limit is the same as the standard IRA limit. Someone earning $400,000 can still only contribute $7,500 via the backdoor in 2026. Treat it as one piece of a broader retirement strategy alongside 401(k)s, cash-balance plans, and HSAs, not your primary savings vehicle.

How to Set Up a Backdoor Roth IRA: Step by Step

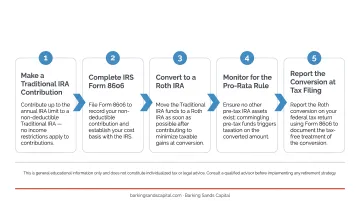

Step 1: Open a Traditional IRA and Make a Nondeductible Contribution

Open a traditional IRA if you don't already have one and contribute after-tax dollars up to the annual limit. Critical: the traditional IRA should carry a zero balance before you begin. Existing pre-tax funds in any traditional IRA, SEP-IRA, or SIMPLE IRA will trigger the pro-rata rule (covered in the next section), creating an unexpected tax bill.

If you already have pre-tax IRA balances, read the tax implications section before proceeding.

Step 2: Let the Contribution Settle

Most custodians require a few business days before funds are available for conversion. Some investors hold the contribution in cash during this window to avoid accruing investment gains — any earnings between contribution and conversion are taxable as ordinary income at conversion.

Step 3: Convert to a Roth IRA

Convert the full balance. Partial conversions leave a pre-tax/after-tax mix in the traditional IRA, complicating future conversions. The transfer can be done in-kind or as cash to an existing Roth IRA or a new one — your custodian's online platform typically handles this in a few clicks.

Step 4: Complete the Conversion by December 31

Roth conversions are taxed in the calendar year they occur — not by the tax filing deadline. Unlike traditional IRA contributions (which can be made up to April 15 of the following year), conversions must be done before year-end to count for that tax year.

Step 5: File IRS Form 8606

Form 8606 documents your nondeductible contribution and tracks your after-tax basis — preventing the IRS from taxing those dollars again when you eventually withdraw. Your custodian will also issue Form 1099-R reporting the distribution from the traditional IRA. You'll need both to properly document the conversion:

- Form 8606 — tracks your nondeductible (after-tax) basis in the IRA

- Form 1099-R — reports the distribution from the traditional IRA

- Form 5498 — issued by your custodian confirming the Roth conversion (for your records)

The Mega Backdoor Roth: A Related Option

For those whose 401(k) plans allow after-tax contributions, the mega backdoor Roth operates on similar logic at a much larger scale. The 2025 total defined contribution limit is $70,000 — nearly ten times the standard IRA limit — allowing far more after-tax dollars to reach Roth status. Not all plans support this feature, and the rules around in-service distributions vary by employer.

Barking Sands Capital's advisors, including CFP® and ChFC credentialed professionals, can review your employer plan documents and determine whether the mega backdoor Roth fits within your broader retirement income plan.

Backdoor Roth IRA Tax Implications: The Pro-Rata Rule and More

The General Tax Picture

When executed cleanly — zero-balance traditional IRA, no other pre-tax IRA assets — the backdoor conversion is typically not a taxable event. The contribution was already made with after-tax dollars. The only taxable amount is any earnings that accrued between contribution and conversion.

That clean scenario requires attention to what's sitting in your other IRA accounts.

The Pro-Rata Rule

The IRS doesn't evaluate your IRAs individually. It looks at all traditional IRAs, rollover IRAs, SEP-IRAs, and SIMPLE IRAs as a single combined pool when calculating the taxable portion of any conversion.

Here's a concrete example: suppose you contribute $7,000 after-tax to a new traditional IRA, but you also have $93,000 in pre-tax rollover IRA funds elsewhere. The IRS denominator is $100,000. Your after-tax basis is only 7% of the total — meaning 93% of whatever you convert is taxable, not 0%.

Converting $7,000 under these circumstances produces roughly $6,510 in taxable income — essentially defeating the purpose of the strategy.

The workaround: if your employer-sponsored 401(k) plan accepts incoming rollovers, moving the pre-tax IRA funds into that plan removes them from the pro-rata calculation entirely. Not all 401(k) plans allow this, so verify with your plan administrator before proceeding.

The 5-Year Rule for Conversions

Two separate 5-year rules apply to Roth IRAs. For backdoor conversions, the relevant one is this: converted funds must remain in the Roth for at least 5 years to avoid a 10% early withdrawal penalty on the converted amount if you're under age 59½. A few mechanics worth knowing:

- Each conversion starts its own independent 5-year clock on January 1 of the conversion year

- If you're 57 and convert today, those funds become accessible penalty-free at age 59½

- If you're younger than 54, the 5-year window is the binding constraint — not your age

Tax Bracket Considerations

A large conversion executed in a high-income year can push income into a higher marginal bracket. State income taxes compound this. Before converting — especially a large amount — model the income impact against your full picture.

This is where working with a fee-based advisor pays off. At Barking Sands Capital, our InteProcess™ coordinates tax planning with your broader retirement strategy, so a conversion decision doesn't create an unintended tax surprise elsewhere.

Pros, Cons, and When the Backdoor Roth Doesn't Make Sense

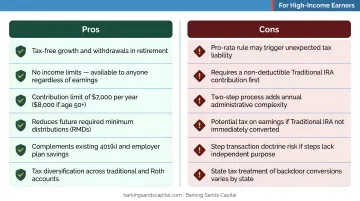

Pros of the Backdoor Roth IRA

- Tax-free growth on all future earnings in the Roth

- Tax-free qualified withdrawals in retirement

- No lifetime RMDs — Roth IRA owners are not required to take minimum distributions during their lifetime, per IRS Publication 590-B

- Estate planning advantages — heirs can inherit Roth IRAs without triggering immediate income taxes on qualifying distributions

Cons and Situations Where It May Not Be the Right Move

The backdoor Roth isn't the right call in every situation. Consider skipping it — or at least pausing — if:

- You have significant pre-tax IRA balances and no 401(k) to absorb them (the pro-rata rule significantly complicates the tax math)

- You may need the funds within 5 years and are under age 59½

- Your current tax bracket is lower than your expected retirement bracket — in that case, pre-tax contributions to a traditional IRA or 401(k) likely outperform Roth contributions now

- You haven't maxed out higher-priority accounts — 401(k) contributions, especially with an employer match, or an HSA should generally come first

Whether the backdoor Roth makes sense depends on your full financial picture — tax situation, estate goals, and income needs together. Barking Sands Capital evaluates these strategies in that broader context, not as standalone decisions.

Frequently Asked Questions

Is a backdoor Roth still allowed in 2026?

Yes. The backdoor Roth IRA remains legal and widely used as of 2026. A 2021 legislative proposal would have eliminated it, but that language was stripped from the final Inflation Reduction Act. No enacted law has eliminated the strategy, though Congress revisits retirement tax rules periodically — worth monitoring each year.

Can I do a backdoor Roth if I earn $500,000 a year?

Yes. There is no income ceiling on Roth conversions. Anyone can make a nondeductible traditional IRA contribution and convert it. The annual contribution amount is still capped at the IRA limit ($7,500 in 2026 for those under 50).

Should I convert $120,000 per year to a Roth to avoid RMDs?

Converting to a Roth reduces future RMDs, but large conversions create taxable income in the conversion year and can push you into a higher bracket. The right annual amount depends on your income, current bracket, and retirement timeline. A financial advisor can model the scenarios specific to your situation.

What happens if I already have a traditional IRA with pre-tax funds when doing a backdoor Roth?

Existing pre-tax IRA balances trigger the pro-rata rule, making a portion of your conversion taxable even if the contribution you're converting was after-tax. Rolling those pre-tax funds into a 401(k) before executing the backdoor Roth can eliminate this complication — if your employer plan allows incoming rollovers.

Do I need to file any special tax forms for a backdoor Roth IRA?

Yes. File IRS Form 8606 each year you make a nondeductible contribution — it tracks your after-tax basis and prevents double taxation. Your custodian will also issue Form 1099-R reporting the distribution from the traditional IRA.