Introduction

Your business is likely your largest asset. For most owners, it's also their retirement plan — yet the numbers on actual preparedness are sobering. According to the Exit Planning Institute's 2023 National State of Owner Readiness Report, only 42% of business owners had a written, formal transition plan in place. That means the majority of owners are carrying their single largest financial asset into retirement with no documented strategy for converting it into income.

Exit planning isn't just retirement planning with a business attached. It's a simultaneous set of decisions spanning business operations, personal finances, tax strategy, estate planning, and often family dynamics. Each dimension affects the others, and getting one wrong can unravel the rest.

This article covers what business owners nearing retirement need to understand:

- The financial stakes of an unplanned exit

- The full range of exit paths available

- How to prepare your business to maximize its transferable value

- How deal structure and taxes affect your actual proceeds

- How to turn a successful sale into a retirement income plan that lasts

Key Takeaways

- Your business likely represents 80% or more of your net worth — exit planning is how you convert that into retirement income

- Multiple exit paths exist beyond a simple sale — your goals, timeline, and readiness determine the best fit

- Deal structure and taxes frequently matter more than the headline price

- Successful planning integrates personal, financial, and business goals, not just the transaction

- Starting 3–7 years early gives you more options, more leverage, and better outcomes

Why Exit Planning Can't Wait

The Concentration Risk Most Owners Underestimate

The EPI's research shows a business typically represents 80% or more of an owner's total net worth. That level of concentration would be unacceptable in an investment portfolio — yet most owners carry it into the years immediately before retirement without a plan to diversify.

The math gets harder when you factor in market realities. According to the Exit Planning Institute, only 20% to 30% of businesses that go to market actually sell. Put those two facts together and the risk becomes clear: most of an owner's wealth is locked in an asset that statistically has a poor track record of transferring successfully.

Forced Exits Happen More Than Owners Expect

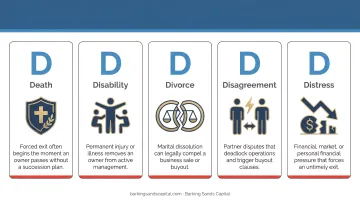

Planning for a voluntary exit isn't enough on its own. The EPI identifies the "5 D's" — Death, Disability, Divorce, Disagreement, and Distress — as the five most common triggers of an unplanned or forced business exit. Roughly 50% of all business exits result from one of these scenarios.

No owner plans for a health crisis or a partnership dispute, but both can force a sale at the worst possible time, under the worst possible conditions. A contingency plan — including buy-sell agreements, life and disability insurance, and succession protocols — is not optional; it's part of any credible exit strategy.

The Cost of Waiting

The compounding benefit of early planning is real. Start five years out and you have time to:

- Increase business value through operational improvements

- Reduce owner dependency that suppresses valuation

- Prepare a successor or management team

- Optimize the tax structure before a deal is negotiated

Start six months out and most of those options close. Tax structures are harder to change. Buyers discount businesses that still run through the owner. And the emotional pressure of an imminent transaction makes objective decisions harder.

The demographics reinforce the point. The same EPI report found that 49% of business owners intend to exit within 5 years, and 75% within 10 years. That's a large wave of businesses hitting the market at once — more competition for buyers' attention, and a weaker negotiating position for anyone who waits.

Many owners also delay for reasons that have nothing to do with numbers. The business feels inseparable from identity, and that's worth acknowledging. But an exit plan isn't a commitment to leave — it's the option to leave on your own terms.

Your Exit Strategy Options Explained

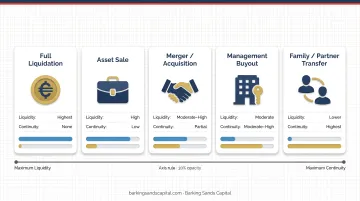

Most owners default to thinking about a third-party sale, but there are six realistic paths worth understanding:

| Exit Path | How It Works | Best Suited For |

|---|---|---|

| Third-Party Sale | Sale to a strategic buyer (industry player seeking synergies) or financial buyer (private equity focused on returns) | Owners prioritizing maximum liquidity and a clean break |

| Management Buyout (MBO) | Existing managers acquire the business, often with financing support | Owners who value internal continuity and have a capable leadership team |

| ESOP | Employees acquire shares through a tax-advantaged trust; the NCEO reports 6,609 active ESOP plans with over $2 trillion in assets | Owners who value employee ownership, culture preservation, and tax benefits |

| Family Succession | Ownership and/or leadership transfers to family members | Owners for whom legacy and family continuity outweigh maximizing sale price |

| Recapitalization | Partial sale provides immediate liquidity while the owner retains equity and future upside | Owners who want some liquidity now but aren't ready for a full exit |

| Orderly Wind-Down | Controlled closure of the business, distributing assets and settling obligations | Businesses without a viable transfer option or where owner simply prefers closure |

Choosing the Path That Fits Your Goals

The right path depends on honest answers to four questions:

- How soon do I want to exit? — A family succession may take a decade to execute well; a third-party sale can close in months

- How important is legacy and culture continuity? — ESOPs and family succession prioritize this; PE buyers typically do not

- Do I want full liquidity or some ongoing involvement? — Recaps and earn-outs keep you in the picture; a clean sale does not

- How much post-exit financial risk am I comfortable with? — Seller financing and earn-outs delay and condition your proceeds

The core tradeoff is between liquidity-focused options (third-party sale) and continuity-focused options (ESOP, family succession). A third-party sale typically delivers the highest upfront cash, but the buyer controls what happens next. An ESOP or family transfer preserves culture and relationships, usually at the cost of a lower immediate price and a timeline measured in years, not months.

Define your personal priorities first, then evaluate which paths are realistically available given your timeline and business condition. Owners who skip that first step tend to choose the path that looks best on paper — not the one that actually fits their life after the sale.

How to Prepare Your Business for a Successful Exit

The Core Principle: Independence Drives Value

Buyers, successors, and investors pay a premium for businesses that don't depend on the owner to function. A useful test: could your business run smoothly for 30 days if you were completely unavailable? If the honest answer is no, that gap directly reduces what a buyer will pay — and may reduce the pool of buyers willing to engage at all.

EPI's research found that only 57% of owners felt confident their management team could lead the business post-exit — meaning nearly half are approaching an exit without the leadership depth that buyers expect.

What to Strengthen Before You Go to Market

Focus on these five areas:

- Clean, well-documented financials — At minimum, three years of accurate, recast financials. Buyers and lenders rely on these for due diligence and deal financing

- Reduced customer or vendor concentration — Over-reliance on a handful of clients or suppliers introduces risk that buyers discount heavily

- Documented processes and systems — If key knowledge lives only in the owner's head, it doesn't transfer. Written procedures, SOPs, and operating manuals make the business more transferable

- A capable second-tier management team — This may be the single biggest driver of transferable value. Develop leaders who own client relationships and operational decisions independently

- Legal and compliance hygiene — Current contracts, licenses, IP ownership, and any outstanding disputes should be resolved before going to market

Getting a Formal Valuation — Earlier Than You Think

Many owners only seek a business valuation when they're ready to sell. Waiting until then forfeits most of the benefit. A valuation done 3–5 years before an exit serves a different purpose: it reveals the gap between what you think the business is worth and what a buyer would actually pay, and gives you a benchmark to track value-building progress.

Different exit paths also require different valuation approaches:

- Fair market value — The standard used for ESOPs and estate planning transactions, as defined under IRS guidance

- Control premium — Applies to competitive sales where a strategic buyer pays above fair market value because synergies justify it

Confirming which standard applies to your intended path early prevents costly surprises during negotiations.

Deal Structure, Taxes, and Post-Exit Income

Why the Headline Price Isn't the Right Number to Focus On

The structure of a deal often has more impact on what an owner actually receives than the stated sale price. Common deal components include:

- Upfront cash — The most certain component; taxed in the year of receipt

- Seller financing / installment notes — Spreads proceeds over time; IRS Topic 705 defines installment sales as those where at least one payment is received after the year of sale, which can defer tax recognition

- Earn-outs — Contingent payments tied to post-closing performance; they bridge valuation gaps but introduce payment uncertainty and tax complexity

- Retained equity — Common in PE transactions where the seller rolls a portion of equity into the new entity for a potential second payout on a future sale

Each component affects the timing, certainty, and total value of what you receive. A deal structured heavily around earn-outs or seller notes may carry a higher headline price than an all-cash offer. After accounting for risk and the time value of money, it may deliver less actual value.

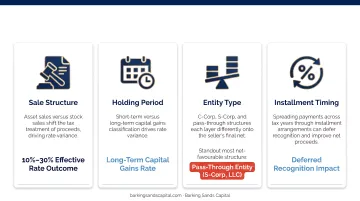

The Tax Dimension: Structure Matters More Than Most Owners Realize

Two deals with identical sale prices can produce very different after-tax outcomes. A practical example illustrates this well: in an S corporation asset sale scenario analyzed in The Tax Adviser, structuring the same transaction with an installment note and a qualifying plan of liquidation reduced the seller's taxable gain in the year of sale from $550 to just $67, deferring $483 to future years when note payments are received.

Key variables that affect net proceeds:

- Asset sale vs. stock sale — Asset sales typically expose sellers to higher ordinary income rates on certain asset classes; stock sales generally receive more favorable capital gains treatment but may require a price concession to attract buyers

- Entity structure — C corps, S corps, and LLCs each carry different tax implications on sale

- Installment sale elections — Can spread gain recognition, but require careful planning to avoid unintended acceleration

- Transaction timing — The year in which a deal closes can significantly affect which tax rates apply

Early coordination with a tax advisor is not optional. Once a deal is in progress, most structural options are already off the table. Those tax decisions also shape what you have available to live on — which makes the income planning phase the natural next step.

Converting Sale Proceeds Into a Retirement Income Plan

A successful closing does not automatically produce retirement security. Translating proceeds into a sustainable income plan requires dedicated planning:

- Define post-exit income needs in after-tax terms — Your spending needs don't change, but your income sources do

- Account for healthcare costs before Medicare eligibility — If you exit before 65, private coverage through the Marketplace can represent a significant expense

- Evaluate Social Security timing strategically — The SSA confirms that claiming before full retirement age permanently reduces benefits; for owners with substantial sale proceeds, delaying often makes mathematical sense

- Build an investment strategy suited to your new financial profile — You're no longer earning business income; the portfolio needs to generate income and grow while managing longevity risk

This is where coordinated planning matters most. Barking Sands Capital's InteProcess™ connects tax planning, asset distribution, and retirement income into a single process — so investment decisions aren't made apart from the estate and tax considerations that directly affect them.

Building Your Exit Planning Team

Exit planning is too complex for any single advisor to handle alone. The disciplines involved — financial planning, tax strategy, legal and estate planning, and business advisory — each require genuine expertise, and the decisions in each area affect the others.

The Core Team Roles

| Role | Primary Responsibility |

|---|---|

| Financial Advisor | Retirement income planning, investment management, coordinating the overall plan |

| Tax Advisor / CPA | Deal structure optimization, installment sale elections, post-exit tax efficiency |

| Attorney | Buy-sell agreements, entity restructuring, estate documents, transaction documents |

| Business Consultant / Fractional CFO | Operational improvements, value-building, pre-exit readiness |

Coordination across these roles is what separates a sound exit plan from a fragmented one. Advisors working in silos — even excellent ones — miss the interactions between disciplines. A tax decision that looks optimal in isolation, for instance, can quietly undermine the estate plan your attorney has structured.

Barking Sands Capital's approach is built around this kind of integration. As an independent, fee-based RIA, the firm has no commission-based incentive to push products. Their InteProcess™ is designed to coordinate financial planning, tax strategy, retirement analysis, and estate planning as a unified process — not a set of parallel conversations.

For business owners managing a multi-million-dollar transition, that coordination structure is worth as much as the individual expertise each advisor brings.

The timing recommendation from most advisors is consistent: begin assembling your team 3 to 7 years before your target exit date. The team's role doesn't end at closing — post-exit wealth management and income planning require ongoing guidance as investment conditions, tax laws, and personal circumstances evolve.

Frequently Asked Questions

What are the 5 D's of exit planning?

The 5 D's — Death, Disability, Divorce, Disagreement, and Distress — are the five most common triggers of an unplanned or forced business exit, as identified by the Exit Planning Institute. Planning proactively addresses all five by putting buy-sell agreements, insurance coverage, and succession protocols in place before any of them occur.

What are the 4 C's of exit planning?

The Exit Planning Institute's 4 C's are the four intangible capitals that drive business value:

- Human Capital — your people and leadership depth

- Structural Capital — documented systems and processes

- Customer Capital — diversified, transferable client relationships

- Social Capital — reputation and external relationships

According to the American Bankers Association, these four capitals may represent up to 80% of a company's total value.

At what age do most business owners retire?

There's no universal answer — one NFIB survey found that 46% of small business owners never intended to fully retire. The more relevant question is financial readiness: does the combination of business sale proceeds, investment assets, and other income sources support your desired lifestyle without depending on continued business income?

What is the difference between exit planning and succession planning?

Succession planning is one component of exit planning — it focuses specifically on identifying and preparing the next leader. Exit planning is the broader, more comprehensive process that also encompasses financial, tax, legal, estate, and operational planning for the owner's full transition out of the business.

How long does exit planning typically take?

Most advisors recommend starting 3 to 7 years before your target exit date, with early phases focused on assessment, value-building, and team assembly. Compressed timelines are possible but typically leave fewer strategic options and less room to improve tax outcomes.