A single nursing home stay, a liability lawsuit, or a poorly timed market downturn in year two of retirement can permanently alter a plan that took 30 years to build. According to Fidelity's 2025 Retiree Health Care Cost Estimate, an average 65-year-old couple may need roughly $345,000 just for healthcare expenses in retirement — and that figure excludes long-term care entirely.

This guide covers the practical strategies — insurance-based, legal, and tax-efficient — that can shield a lifetime of savings from the specific risks retirees face.

Key Takeaways

- Asset protection in retirement is about preservation, not growth — the threats shift entirely once withdrawals begin

- Insurance (umbrella and long-term care) is the most accessible first layer of protection

- Legal tools like irrevocable trusts and proper beneficiary designations shield assets from creditors and courts

- Roth conversions and tax-location strategies protect more of your income from unnecessary tax erosion

- Most protection strategies must be in place before a threat arises; acting early is what makes them work

Why Asset Protection Looks Different in Retirement

During your working years, the primary financial threats are professional liability and debt. Retirement introduces an entirely different set of risks.

The five key threats retirees face:

- Healthcare and long-term care costs — the most underestimated risk

- Creditors and lawsuits — liability doesn't disappear at retirement

- Market downturns affecting income sustainability — especially dangerous in early retirement

- Estate taxes, probate, and estate disputes

- Fraud and financial exploitation — elder fraud losses hit $4.9 billion in 2024, a 43% increase from 2023

The Decumulation Problem

Once you begin drawing from your portfolio, early losses are fundamentally more damaging than the same losses during your working years. A worker who experiences a market crash can stop withdrawals, keep contributing, and wait for recovery.

A retiree withdrawing monthly is selling assets at depressed prices, permanently reducing the base from which future growth compounds. This is a structural vulnerability — not a theory — and it defines retirement finance.

What Asset Protection Is (and Isn't)

Asset protection means placing assets in legal structures that are harder for creditors, courts, and unforeseen costs to reach — legally, transparently, and without hiding income or evading taxes. Every strategy in this guide is legal, transparent, and — critically — must be established before a threat arises. Courts regularly reverse asset transfers made after a lawsuit or liability is known, treating them as fraudulent conveyance.

A note on state law: Michigan and Minnesota both have specific homestead exemptions, IRA protections, and annuity shelters built into state law. Knowing what your state already provides is the right place to start before layering on additional strategies.

Protecting Your Portfolio from Market Risk and Longevity Risk

Sequence of Returns Risk

Here's a scenario that illustrates why retirement timing matters more than average returns. Morningstar modeled two retirees, each starting with a $600,000 portfolio and withdrawing at 6% annually, but experiencing the same returns in opposite order. The retiree who received strong early returns still had assets above the starting value after 30 years. The retiree who experienced poor returns first ran out of money entirely by year 16 — despite identical average returns over the period.

Same average return, completely different outcomes — that's sequence of returns risk.

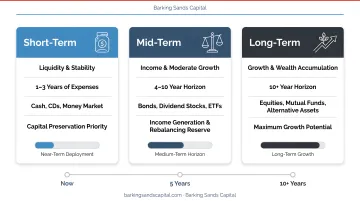

Asset Allocation as a Protective Tool

A retirement portfolio isn't optimized the same way as an accumulation portfolio. The goal shifts from maximizing growth to ensuring you can meet income needs without being forced to sell equities at a loss during downturns.

This typically means:

- Holding 1-3 years of expenses in stable, liquid assets (cash, short-term bonds)

- Keeping medium-term assets in balanced or fixed-income funds

- Allowing growth-oriented equities time to recover before you need to tap them

This framework — often called the bucket strategy — is one of the more practical approaches to translating allocation theory into actual retirement cash flow.

Guaranteed Income as a Foundation

The more guaranteed income you have (Social Security, pension, annuity), the less you need to withdraw from a volatile portfolio during a down market. Delaying Social Security to age 70 increases your benefit by 8% per year beyond full retirement age. For someone born in 1960 or later, claiming at 70 delivers 124% of the full retirement benefit — permanently, for life.

Active investment management can complement this foundation. Barking Sands Capital's approach centers on managing positions to minimize losses during down markets and preserve the portfolio base for the next growth cycle — rather than simply riding broad market movements up and down. For retirees facing sequence risk, that orientation toward loss minimization matters most in the early years of withdrawal.

Longevity Risk

The Social Security Administration projects that a 65-year-old male today can expect to live approximately 19 more years; a 65-year-old female, roughly 22 more years. Many retirees will far exceed those averages. Running out of money in your mid-80s is a financial catastrophe.

Morningstar's current research suggests a 3.9% safe starting withdrawal rate for a 30-year retirement with a 90% probability of success. That's meaningfully lower than the commonly cited 4% rule — factor that into your withdrawal plan from the start.

Insurance and Long-Term Care as Asset Protection Tools

Umbrella Insurance: The Overlooked Layer

Most retirees carry homeowners and auto insurance, but those policies have limits. A single serious auto accident or a personal injury lawsuit on your property can exceed those limits entirely, exposing personal assets.

Personal umbrella insurance provides excess liability coverage above existing policy limits — typically covering lawsuits, personal injury claims, and property damage. The cost is modest: industry data from Mercury Insurance shows $1 million in umbrella coverage typically runs $300–$600 per year. For $2 million, expect $600–$1,000 annually. For most retirees, this is among the highest-value protection they can buy relative to cost.

Long-Term Care: The Biggest Gap in Most Retirement Plans

Someone turning 65 today has nearly a 70% chance of needing some form of long-term care before they die. Without a plan, the costs can be devastating.

According to Genworth/CareScout's 2024 Cost of Care Survey, national median annual costs are:

| Care Type | National | Michigan | Minnesota |

|---|---|---|---|

| Nursing home (semi-private) | $111,325 | $127,750 | $146,000 |

| Nursing home (private) | $127,750 | $138,883 | $168,813 |

| Assisted living | $70,800 | $72,480 | $69,900 |

| Home health aide | $77,792 | $77,792 | $98,384 |

A two-year nursing home stay in Minnesota could cost over $330,000. Without insurance, that comes directly from retirement savings.

Medicare Planning and Long-Term Care

A common and expensive misconception: Medicare does not cover custodial long-term care. If you need help with daily activities — bathing, dressing, eating — Medicare won't pay for it. This is a coverage gap that catches many retirees off guard.

Options for addressing this gap include:

- Traditional long-term care insurance — dedicated coverage, though premiums have risen sharply in recent years

- Hybrid life/LTC policies — pair life insurance with an LTC benefit rider, so the coverage isn't forfeited if care is never needed

- Self-insuring — reserving a dedicated pool of savings; practical only for those with substantial liquid assets

Curtis Hewitt, an advisor with Barking Sands Capital who specializes in Medicare Planning and Long-Term Care, helps retirees evaluate which approach fits their health status, age, and overall financial plan. The starting point is usually health status and age: the earlier you act, the more options remain open — and the lower the premiums. That same logic applies when considering how life insurance fits alongside an LTC strategy.

Life Insurance in Retirement

Most retirees need less life insurance than during their working years. But permanent life insurance with cash value can still serve specific purposes:

- Provides a tax-advantaged liquid reserve accessible during retirement

- Equalizes inheritances when assets (like a business or property) can't be split evenly

- Funds an Irrevocable Life Insurance Trust (ILIT), keeping death benefits out of the taxable estate entirely

Trusts, LLCs, and Beneficiary Designations

Understanding What Trusts Actually Do

Not all trusts provide creditor protection. This distinction matters more than most retirees realize.

A revocable living trust is primarily a probate-avoidance tool. Because you retain control, creditors can still reach those assets. It does not shield wealth from lawsuits or Medicaid spend-down.

An irrevocable trust transfers control out of your estate. Done correctly, those assets become harder for creditors to reach and can be structured to avoid estate taxes. The tradeoff is exactly what the name implies: you cannot easily reverse the transfer.

The Medicaid Asset Protection Trust (MAPT) is specifically designed for retirees who may eventually need nursing home care and want to protect assets for heirs. The critical timing consideration: Michigan requires a 60-month lookback period for asset transfers. Minnesota applies similar lookback rules. Trusts established after a nursing home admission is imminent offer little protection — courts look back five years.

Because trust decisions intersect with tax exposure, Medicaid eligibility, and estate distribution, they rarely work in isolation. Barking Sands Capital coordinates with estate attorneys as part of its InteProcess™, integrating legal, insurance, tax, and retirement planning into a single engagement.

Beneficiary Designations Override Everything Else

Beneficiary designations on IRAs, 401(k)s, annuities, and life insurance policies are legal agreements with the institution — and among the most frequently overlooked details in estate planning. A will cannot override them.

If your IRA still lists an ex-spouse as beneficiary, that ex-spouse inherits the account regardless of what your will says.

Review beneficiary designations after:

- Death of a spouse or beneficiary

- Divorce or remarriage

- Birth of grandchildren

- Any significant change to your estate plan

One additional complexity: naming a trust as an IRA beneficiary requires careful structuring to satisfy IRS requirements. The rules around trust beneficiaries and Required Minimum Distributions are detailed and technical — consult a qualified advisor before making that designation.

LLCs for Real Estate Owners

Retirees who own investment real estate face liability exposure beyond their personal assets. An LLC separates the property from personal wealth, limiting the owner's exposure if a tenant or visitor sues.

That protection isn't automatic, though. Common trade-offs include:

- Setup and annual compliance costs

- Ongoing recordkeeping requirements to maintain legal separation

- Loss of liability protection if the LLC is improperly maintained ("piercing the corporate veil")

Family Limited Partnerships (FLPs) serve a similar function for those with significant family business interests, though they draw IRS scrutiny and require careful structuring.

Tax-Efficient Strategies That Preserve Your Wealth

Roth Conversions: The Window Between Retirement and RMDs

The years between retirement and age 73 represent the best window for Roth conversions. (For those born after January 1, 1960, RMDs don't begin until age 75.) Income is typically lower during this period, tax brackets are more manageable, and converting now reduces future RMDs that would otherwise force taxable withdrawals at potentially higher rates.

Benefits of converting traditional IRA assets to a Roth:

- Reduces future RMDs

- Lowers lifetime tax liability

- Passes a tax-free inheritance to heirs

Barking Sands Capital offers Roth IRA conversion strategies as a core component of their retirement planning services, integrated with broader tax and retirement coordination. The right conversion amount depends on your individual tax situation. Professional tax modeling is what turns a good idea into a precise, year-by-year plan.

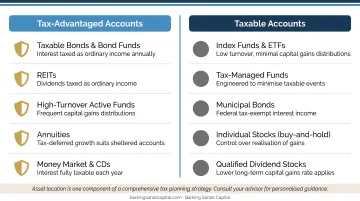

Tax-Location Strategy

Where you hold an investment matters almost as much as what you hold. The general principle:

- Tax-advantaged accounts (IRA, 401(k)): Hold tax-inefficient assets — bond funds, REITs, actively traded funds

- Taxable accounts: Hold tax-efficient assets — index funds, municipal bonds, buy-and-hold equities

This approach improves after-tax returns without changing your overall asset allocation or taking on additional risk. Over a 20-year retirement, the compounding difference between tax-efficient and tax-inefficient placement can easily reach five figures.

Qualified Charitable Distributions and IRMAA

Tax-location strategy manages where assets sit. QCDs manage what comes out — and at what cost. For retirees over age 70½, a Qualified Charitable Distribution (QCD) allows up to $111,000 annually (2026 limit) to be transferred directly from an IRA to a qualified charity. The distribution counts toward your RMD but is excluded from taxable income.

This matters beyond just the tax deduction. Lower adjusted gross income can:

- Keep you below IRMAA thresholds (Medicare surcharges begin at $109,000 MAGI for individual filers in 2026)

- Reduce taxation of Social Security benefits

- Lower your overall tax bracket

For retirees with charitable intent, a donor-advised fund offers additional flexibility: it allows a large deductible contribution in a high-income year, with distributions to charities spread over multiple years.

Frequently Asked Questions

How do I protect my assets in retirement?

Start with insurance — umbrella coverage and a long-term care plan address the most common and costly threats. Then ensure your legal documents are current: trusts, wills, and beneficiary designations. From there, manage portfolio risk through asset allocation and guaranteed income sources, working with a fee-based advisor well before any specific threat appears.

What is the $1,000 a month rule for retirees?

The $1,000-a-month rule estimates that every $1,000 of desired monthly retirement income requires roughly $240,000 saved, based on a 5% annual withdrawal rate. It's a conversation starter, not a financial plan — sequence of returns risk and longevity can significantly shorten how far that savings goes.

What is the biggest threat to retirement assets?

Healthcare and long-term care costs are the most commonly underestimated threats — a prolonged nursing home stay can exhaust a substantial retirement portfolio within a few years. Sequence of returns risk in early retirement is a close second, followed by longevity risk: simply living longer than your savings were planned to last.

Are 401(k) and IRA accounts protected from creditors in retirement?

ERISA-qualified plans like 401(k)s have strong federal anti-alienation protection under federal law. IRA protections vary by state — some states offer unlimited protection, others cap it. In bankruptcy, the federal IRA exemption is currently $1,711,975 per person (2025–2028). Once funds are withdrawn from any retirement account, they become regular assets and lose protected status.

When is the right time to set up asset protection strategies?

Before you need them. Courts can and do reverse asset transfers made after a lawsuit, liability, or healthcare crisis is already known — treating them as fraudulent conveyance. The best time to establish trusts, review insurance coverage, and update beneficiary designations is well before any specific threat appears.

Does long-term care insurance protect my retirement savings?

Yes — it shifts the financial risk of an extended care need to an insurer rather than your savings. A multi-year nursing home stay at $127,000–$168,000 annually (Minnesota rates) can quickly deplete most retirement portfolios. Hybrid life/LTC policies have grown in popularity for those who want coverage without the "use it or lose it" concern of traditional policies.