Introduction

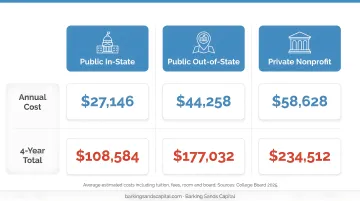

College is expensive — and getting more so every year. According to the College Board's Trends in College Pricing and Student Aid 2025, the full annual cost of attendance (tuition, fees, housing, and food) now runs $25,850 at public in-state schools, $45,780 at out-of-state public schools, and $60,920 at private nonprofit institutions.

Multiply those figures by four and factor in tuition inflation running at roughly 4% annually. A child born today could face a four-year price tag approaching $224,000 at an in-state public school — or over $528,000 at a private nonprofit — by the time they enroll.

Those numbers are daunting, but they're not inevitable. With the right approach, most families can close a significant portion of that gap.

Most families don't struggle because college is unaffordable. They struggle because they started too late, chose the wrong savings vehicles for their tax situation, or never built a structured plan. This guide addresses all three: when to start, which accounts to use, and how to put a realistic savings strategy in place.

Key Takeaways

- College costs outpace general inflation, meaning every year you delay saving costs more than the year before

- The right savings vehicle (529, ESA, UGMA/UTMA) depends on your income, flexibility needs, and timeline

- In the early years, automating contributions consistently outperforms waiting to save a larger lump sum

- Scholarships, AP credits, and family gifting can shrink how much you need to save out of pocket

- College savings produces better outcomes when integrated into your overall financial plan

How College Costs Accumulate Over Time

College bills don't arrive as one lump sum. They build over four years — and they tend to grow faster than most families expect.

The Inflation Gap

Tuition has grown at a compound annual rate of 4.04% in the 21st century, outpacing the Consumer Price Index. In 2025-26 specifically, private nonprofit tuition rose 4.0% while general inflation ran at 2.6% — a 1.4 percentage point gap that adds up meaningfully across a decade of saving.

What makes this harder to track: cost increases aren't uniform. Tuition tends to rise gradually each year, but room and board, fees tied to specific programs, and textbook costs can spike without warning. Families who only watch the tuition headline number often underestimate total spending by thousands.

The Perception Problem

Sallie Mae's How America Pays for College 2025 found that undergraduate families spent an average of $30,837 in 2024-25 — up 9% from the prior year. Two findings stand out:

- Only 18% of families expected to pay less than sticker price — yet 47% actually did

- The gap between anticipated and actual costs, in either direction, typically becomes clear only at enrollment

By the time enrollment makes the numbers concrete, the window for adjusting a savings strategy is narrow. Starting early matters precisely because compounding is unforgiving of delays: early contributions grow, and late starts require far more to catch up.

Key Factors That Shape Your College Savings Target

Before choosing a savings vehicle, it helps to anchor on a realistic number.

Baseline Costs by School Type (2025-26)

| School Type | Annual Cost | 4-Year Total (Today) |

|---|---|---|

| Public, in-state | $25,850 | ~$103,400 |

| Public, out-of-state | $45,780 | ~$183,120 |

| Private nonprofit | $60,920 | ~$243,680 |

Source: College Board Trends in College Pricing 2025. Costs include tuition, fees, housing, and food.

The One-Third Rule

You don't need to save the entire projected cost. SavingForCollege's one-third rule divides expected college costs into three roughly equal parts:

- One-third from savings accumulated before enrollment

- One-third from current income and financial aid during the college years

- One-third from student loans

For a family targeting an in-state public school, this means a savings goal closer to $34,000–$35,000 in today's dollars rather than the full $103,400. That's a number most families can reach with consistent effort over 15–18 years.

Variables That Shift the Target

Your savings goal isn't static. It changes based on:

- School type preference — in-state vs. out-of-state significantly changes the math

- Number of children — two college years can overlap

- Financial aid eligibility — income and asset levels affect what's available

- Early credit opportunities — AP and dual enrollment can reduce required semesters

Mapping these variables now — even roughly — tells you whether you need to save $25,000 or $75,000, which directly determines which savings vehicles make sense.

Strategies to Save for College

Effective college savings works on three fronts: the vehicles you choose, how consistently you manage them, and the external levers that reduce your total out-of-pocket need.

Strategies That Come Down to the Vehicles You Choose

Open a 529 College Savings Plan

The 529 plan is the most widely used tax-advantaged college savings vehicle — and for most families, it's the right starting point. Key features:

- Contributions grow tax-free at the federal level

- Withdrawals for qualified expenses (tuition, fees, room and board, books, required technology) are not taxed federally

- Many states offer deductions on contributions — Minnesota and Michigan both have state-level 529 tax benefits worth evaluating

- Aggregate limits are high — state plans typically allow balances between $529,000 and $606,000

- Two plan types: education savings plans (investment-based) and prepaid tuition plans (locks in today's rates)

As of December 2024, Section 529 plans held $525.1 billion in assets nationwide — a signal of how broadly families have adopted this vehicle.

Consider a Coverdell Education Savings Account (ESA)

ESAs offer tax-free growth and withdrawals for qualified expenses, with one meaningful advantage over 529 plans: they can cover K-12 expenses as well as college costs.

The tradeoffs are real, though:

- Annual contributions are capped at $2,000 per beneficiary

- Income limits apply: phase-outs begin at $95,000 for single filers and $190,000 for joint filers (2025), with no contribution allowed above $110,000 and $220,000 respectively

- Contributions must be made before the beneficiary turns 18; account must be distributed by age 30

ESAs work best as a complement to a 529 plan, not a replacement. For families weighing a third option — one without education restrictions — custodial accounts are worth understanding.

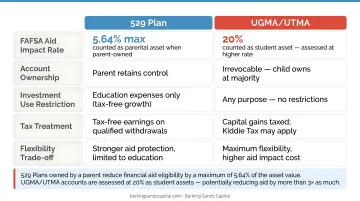

Explore UGMA/UTMA Custodial Accounts for Flexibility

UGMA and UTMA accounts allow you to invest in a child's name without restricting funds to education use — which gives them flexibility a 529 doesn't.

The critical tradeoff: UGMA/UTMA assets are treated as student assets on the FAFSA, subject to a 20% assessment rate. Compare that to a parent-owned 529, where the maximum financial aid impact is roughly 5.64% of the account value. For families expecting financial aid, this difference can be substantial.

Working with a fee-based fiduciary advisor — like the team at Barking Sands Capital — can help you evaluate which combination of these vehicles fits your specific tax situation, family structure, and timeline before committing to one approach.

Strategies That Come Down to How You Manage Contributions

Automate from Day One

Treat monthly 529 contributions like a utility bill — automatic and non-negotiable. Automation removes the temptation to skip contributions during tight months. Use natural income triggers — raises, bonuses, tax refunds — to increase the amount over time.

Shift Investment Allocation as College Approaches

A 529 invested heavily in equities when a child is young makes sense. That same allocation at age 16 doesn't. As college nears, shifting toward more conservative holdings protects what you've built. Most 529 plans offer age-based portfolios that rebalance automatically — a simple, low-effort option.

Use the 2K Rule as a Progress Checkpoint

Fidelity's 2K Rule offers a quick benchmark: multiply your child's current age by $2,000 to estimate where savings should stand if you're on track to cover 50% of a four-year public college. A 6-year-old? You should have roughly $12,000 saved. Behind? That's actionable data — not a reason to give up, but a prompt to increase contributions now rather than later.

Review Your Plan Every Year

Life changes. Income shifts, a second child arrives, or your teenager decides they're interested in a flagship state university rather than the local community college. Annual reviews allow families to update investment risk levels, increase contributions when income rises, and recalibrate against current cost projections. Even a 30-minute annual check-in can catch drift before it compounds into a shortfall.

Strategies That Reduce the Total Cost of College

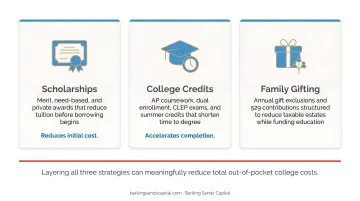

Pursue Scholarships and Grants Early

Scholarships don't need to be repaid — they directly reduce how much savings must cover. The U.S. Department of Labor's CareerOneStop Scholarship Finder lists more than 9,500 scholarship, fellowship, and grant opportunities. Sallie Mae's 2025 data found that scholarships and grants covered 27% of undergraduate college spending for families that year.

Start searching in 9th and 10th grade — not senior year. Many awards have early deadlines or require multi-year participation.

Earn College Credits in High School

AP, IB, and dual enrollment programs let students complete college-level coursework before they arrive on campus. Each credit earned in high school is one fewer credit to pay for later.

For the class of 2025, 37% of U.S. public high school graduates took at least one AP exam. Students who score well can skip introductory courses entirely — in some cases shaving a full semester off their degree timeline and tuition bill.

Involve Family Members in the College Fund

Grandparents, aunts, uncles, and family friends can contribute directly to a 529 plan through online gifting platforms — no account setup required on their end. This reframes holiday and birthday gifts as something with lasting financial value.

One important update: under the FAFSA Simplification Act, distributions from grandparent-owned 529 plans no longer need to be reported as untaxed student income starting with the 2024-25 academic year. Previously, those distributions could reduce a student's aid eligibility by up to 50% of the distribution amount. That rule has changed, making grandparent contributions significantly more attractive.

Conclusion

College savings isn't a single decision — it's an ongoing process. The families who struggle most aren't always the ones who saved the least. Often, they started late, chose vehicles that didn't fit their tax picture, or never connected their college savings plan to the rest of their financial life.

The strategies in this guide — from 529 selection to the 2K Rule to AP credits — each reduce a different part of the problem. Used together, they make the total funding gap manageable.

That said, college savings can't be planned in isolation. It competes with retirement contributions, insurance coverage, and near-term financial goals for the same dollars. A qualified financial advisor can help you sequence those priorities and build a college funding strategy that accounts for your full financial picture.

Barking Sands Capital offers education funding planning as a core service, helping families in Minnesota, Michigan, and across the Midwest build tax-advantaged savings strategies tailored to their income, timeline, and family structure. Whether you're starting from scratch or stress-testing an existing plan, a focused conversation with one of our advisors can clarify your next move.

Frequently Asked Questions

What is the best savings plan for college education?

For most families, a 529 college savings plan is the strongest starting point — it offers tax-free growth, high contribution limits, and flexibility for a wide range of qualified expenses. If K-12 costs are also a factor or you want additional tax-free capacity, pairing a 529 with a Coverdell ESA can work well. The right answer depends on your income level and how much flexibility you need.

What is the 3-3-3 rule for savings?

The 3-3-3 rule is not a standard personal finance concept — it applies primarily to real estate. A more useful framework for college planning is the one-third rule: split expected costs across pre-enrollment savings, current income and financial aid during school, and student loans. Breaking it into thirds makes the savings target feel far more manageable.

What is the 50/30/20 rule for college students?

The 50/30/20 rule is a general budgeting framework: 50% of income to needs, 30% to wants, and 20% to savings or debt repayment. For families saving for college, allocating a portion of that 20% bucket to a 529 plan each month creates a disciplined, automatic contribution habit without requiring a separate budgeting system.

How much should I save per month for college?

It depends on your target school and when you start. According to SavingForCollege, parents of a newborn covering one-third of public in-state costs should save roughly $170 per month (6% return, 4% annual tuition inflation); Vanguard estimates $250 per month from birth at a 5% return produces approximately $87,300 by age 18.

Does a 529 plan affect financial aid eligibility?

Yes, but modestly. A parent-owned 529 is assessed at a maximum 5.64% on the FAFSA — far lower than the 20% rate applied to student-owned assets like UGMA/UTMA accounts. Grandparent-owned 529 distributions are no longer counted as student income under the simplified FAFSA, making them an increasingly aid-neutral option.

When is the best time to start saving for college?

At birth, if possible. A child who has 18 years of compounding working in their favor needs far less monthly savings than one starting at age 10. That said, starting late is always better than not starting — it just means leaning more heavily on scholarships, aid, and loans to fill the gap that savings alone won't cover.