Consulting too late means missed deductions, compliance penalties, and avoidable IRS scrutiny. Consulting proactively — at the right moments — leads to better outcomes at every stage of business. The difference isn't just how much you pay in taxes. It's whether the damage is fixable at all.

This article covers the specific situations, warning signs, and business milestones that signal it's time to bring in a tax advisor, and what's at stake if you wait.

Key Takeaways

- Consult a tax advisor before you register your business — entity structure affects your taxes for years

- Hiring your first employee, crossing revenue thresholds, and expanding to new states are critical trigger points

- Any IRS correspondence warrants immediate professional consultation — responding alone raises your risk

- Waiting until tax season is the most common and most expensive mistake small business owners make

- Year-round tax advisory catches planning opportunities that a once-a-year filing appointment misses entirely

Why the Timing of Tax Advice Matters More Than Most Owners Realize

Business tax decisions compound — in both directions. Make the right ones early, and they work in your favor for years. Make the wrong ones and ignore them, and they snowball into multi-year problems that cost significantly more to fix than they would have to prevent.

That difference traces back to two modes of working with a tax advisor:

- Reactive tax help — calling an advisor after something has already gone wrong

- Proactive tax planning — making decisions in advance so the tax outcome is built in from the start

Timing determines which mode you're in. The IRS penalty structure puts a real dollar figure on what the reactive mode costs.

IRS FY2025 data shows 540,452 S corporation delinquency penalties assessed — totaling over $1 billion — and 420,328 corporation estimated-tax penalties exceeding $1 billion in the same period.

These aren't anomalies. They reflect how consistently business owners underestimate their tax obligations until those obligations arrive with penalties attached.

A GAO report on sole proprietor compliance found the IRS attributes roughly $80 billion in unpaid taxes annually to sole proprietors underreporting income — about 16% of the total estimated tax gap. Most of that isn't fraud. It's misunderstanding, poor timing, and decisions made without professional guidance.

The Key Situations That Signal It's Time to Call a Tax Advisor

The "right time" to consult isn't a single universal moment. It shifts based on where you are in your business lifecycle. These are the most critical trigger points.

When You're Starting or Structuring Your Business

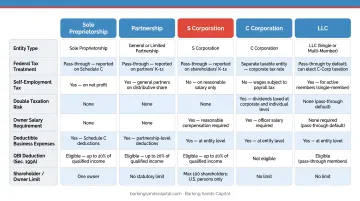

This is the most consequential moment — and the one most owners get wrong. The entity structure you choose before registering your business has lasting tax implications that follow you for years.

The tax treatment varies significantly by structure:

| Structure | Key Tax Implication |

|---|---|

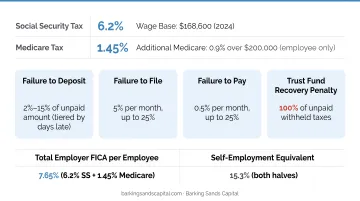

| Sole proprietor | Self-employment tax at 15.3% on net income |

| Partnership | Pass-through taxation; K-1s issued to each partner |

| LLC | Flexible — taxed based on election made at formation |

| S corporation | Pass-through with potential SE tax savings on distributions |

| C corporation | Corporate income tax + potential double taxation on dividends |

According to the IRS and Tax Foundation, nearly 30 million sole proprietorship returns, 5.3 million S corporations, and 4.5 million partnerships filed in 2022 alone. Most of those owners made their structure decision without a tax advisor — and many are paying more than necessary as a result.

Restructuring later is possible but disruptive and costly. The same revenue can produce dramatically different tax outcomes depending on structure. This conversation belongs before you register, not after your first profitable year.

When Your Business Becomes More Complex

Complexity accumulates faster than most owners expect. Each of the following changes your tax obligations in ways that aren't obvious until something goes wrong:

- Revenue growth: crossing thresholds where quarterly estimated taxes become significant

- Adding partners: creates K-1 obligations and partnership tax filing requirements

- New income streams: adding product sales to a service business changes sales tax exposure entirely

- Multi-state operations: especially common for Midwest businesses expanding across state lines

Multi-state operations deserve particular attention. Minnesota requires remote sellers to collect sales tax after exceeding $100,000 in retail sales or 200 retail transactions in the prior 12 months.

Michigan's threshold is identical — $100,000 in sales or 200 transactions in the prior calendar year. Miss those thresholds and you're liable for uncollected sales tax, potentially back to the date you crossed them.

When You Hire Your First Employee

Hiring doesn't just create an HR obligation — it transforms your tax situation.

You become an employer, which means:

- Matching 6.2% Social Security on wages up to $184,500 per employee

- Matching 1.45% Medicare with no wage base ceiling

- Federal and state unemployment tax obligations

- Payroll deposit schedules and reporting requirements

Worker classification adds another layer of risk. Misclassifying an employee as an independent contractor exposes you to back income tax withholding, FICA liabilities, and deposit penalties ranging from 2% to 15%.

The 100% trust fund recovery penalty for willful failure to remit payroll taxes is in a different category entirely. It isn't capped — it's assessed personally against whoever is deemed a "responsible person" in the business.

The IRS takes misclassification seriously. If you're not certain whether someone qualifies as an employee or contractor, that uncertainty itself is a reason to call a tax advisor before you issue your first paycheck.

When You Receive IRS Correspondence

Any notice from the IRS — inquiry, proposed assessment, or audit notification — warrants immediate professional consultation, not a Google search or a DIY response.

Delays make IRS matters worse. The IRS correspondence process is time-sensitive, and your response (or lack of one) sets the tone for what follows.

One clarification worth understanding: a CPA handles tax preparation, planning, and filing. A tax attorney handles legal disputes, potential fraud investigations, and tax court proceedings. For most small business owners receiving a routine notice, a CPA or enrolled agent is appropriate. If the matter involves potential fraud allegations or significant legal exposure, an attorney is the right call. Getting to the right professional on the first call avoids wasted time and unnecessary escalation.

Clear Signs You've Waited Too Long

These are observable signals that you should have called a tax advisor already — and that you shouldn't wait any longer:

- You're unsure how much to pay in quarterly estimated taxes

- Your business income jumped significantly year over year

- You've been mixing personal and business finances

- You received a penalty notice or IRS letter

- You're about to sell the business, add a partner, or begin succession planning

- You feel anxious or uncertain heading into a major financial decision

Discomfort before a major financial decision is a reliable indicator that professional guidance is overdue.

There's a distinction worth understanding here: asking "how do I fill out this form?" is a task for a tax preparer. Asking "how should I structure this hire, this acquisition, or this ownership change to minimize my tax exposure?" requires a strategic tax advisor. Most small business owners default to one when they actually need the other.

What Happens When Small Business Owners Wait Too Long

Waiting until April to consult a tax advisor doesn't just mean missed savings — it often means the window for action has already closed.

Missed Deductions and Credits

Many deductions require action before year-end to be valid. Retirement account contributions, Section 179 equipment deductions (up to $2,560,000 in 2026), home office setup, and vehicle mileage tracking all require proactive setup or documentation. Consulting in April for the prior year means those windows have already closed.

Penalty Accumulation

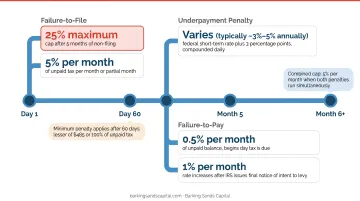

The IRS doesn't wait for you to catch up. Underpaying quarterly estimated taxes triggers penalties regardless of whether you pay in full at filing. The current underpayment rate for Q2 2026 is 6%, rising to 7% for Q3 2026. A small business owner who discovers a $50,000 tax liability in April has already incurred three quarters of underpayment interest.

Failure-to-file penalties run 5% of unpaid tax per month, up to 25% — and failure-to-pay penalties add another 0.5% per month on top of that. Penalties and audit exposure often compound together, which is where the real financial damage sets in.

Audit Risk Through Documentation Gaps

Audit rates for small businesses are low — below 0.1% for most entity types in TY2023 — but aggregate odds don't tell the full story. The IRS uses audit technique guides for specific industries, and certain patterns attract disproportionate attention:

- High deductions relative to reported income

- Home office deductions (which require regular and exclusive business use)

- 100% business use claimed for a vehicle

- Large losses reported across multiple consecutive years

- Cash-intensive businesses

Without professional guidance on how to document and substantiate these claims, legitimate deductions become audit vulnerabilities.

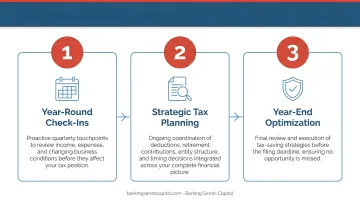

How to Get More Value from Your Tax Advisor Year-Round

Tax advisors add the most value when engaged throughout the year — not just at filing time. Decisions made in Q1 or Q2 (retirement contributions, equipment purchases, business structure changes) can't be reversed in April.

Practical steps:

- Schedule a mid-year check-in — not just a pre-filing meeting. Review estimated payments, anticipated income changes, and year-end planning opportunities before they expire.

- Bring your advisor into major decisions before they happen — hiring, expansion, partnership changes, or business sales. After the transaction, your options narrow considerably.

- Keep organized records throughout the year — not just for filing but for real-time tax planning conversations.

For small business owners, the most strategic move is treating your tax advisor as part of a broader financial team — one that coordinates tax planning alongside retirement, insurance, and estate considerations. Decisions made in one area routinely create unintended consequences in another.

A retirement plan contribution that reduces current taxes might affect Medicare surcharge calculations. A business sale that looks clean from a tax perspective might complicate estate planning.

This is where firms like Barking Sands Capital provide a different kind of value. Through their proprietary InteProcess™, advisors coordinate tax planning, retirement strategy, insurance, and estate planning in a single integrated engagement. For small business owners who have outgrown annual filing help and need forward-looking strategy, that kind of cross-discipline coordination can prevent costly blind spots.

Frequently Asked Questions

When should a small business owner consult a tax advisor?

At business formation, when your tax situation grows complex, when hiring employees, and proactively before any major financial decision. The goal is to consult before the decision — not after. Most tax-shaping choices can't be undone retroactively.

How much does a tax advisor cost for a small business?

Fee structures vary: flat fees per return, hourly rates, and annual retainers for ongoing advisory relationships. Complexity, location, and scope all affect cost. Compare that cost against what IRS penalties, missed deductions, or a poorly structured business could cost you over time.

What are red flags to the IRS for a small business?

Common audit triggers include consistently reporting large losses, high deductions relative to income, home office claims that don't meet IRS use tests, 100% business vehicle use, and cash-intensive operations. A tax advisor helps ensure legitimate claims are properly documented and substantiated.

What is the difference between a tax advisor and a CPA for small businesses?

CPAs are licensed accountants focused on tax preparation, bookkeeping, and filing. A tax advisor (who may or may not be a CPA) focuses on strategic planning to minimize tax liability. For complex business situations, you may need both: a preparer to handle filing and an advisor to shape the decisions that determine what gets filed.

How often should a small business owner meet with a tax advisor?

At minimum, schedule a year-end planning meeting and a mid-year check-in. Add consultations whenever a major business event is on the horizon — hiring, expansion, partnership changes, or ownership transitions. Annual filing appointments alone leave most of the planning value on the table.