The freedom is real. So is the financial complexity.

Most people enter self-employment without a financial roadmap. This article is that roadmap — 10 essential tips organized into actionable themes covering daily money management, tax strategy, retirement planning, insurance, and long-term protection.

Key Takeaways

- Separating business and personal finances is the foundation of every other financial decision

- Self-employed individuals owe 15.3% self-employment tax on net earnings, plus federal and state income taxes — budget for quarterly estimated payments

- Tax-advantaged retirement accounts (Solo 401(k), SEP IRA, SIMPLE IRA) exist specifically for the self-employed and offer contribution limits that rival employer plans

- An emergency fund of 6–12 months of living expenses is the appropriate target — larger than the standard guidance for salaried employees

- Coordinating tax, retirement, insurance, and estate planning together produces far better outcomes than managing each in isolation

Tips 1–3: Separate and Organize Your Finances

Mixing personal and business finances is one of the most common — and most costly — mistakes self-employed people make. The Federal Reserve's 2022 Small Business Credit Survey found that 6% of nonemployer firms used no financial services at all, including basic bank accounts. Beyond the audit risk, mixed funds create bookkeeping nightmares and make it nearly impossible to know whether your business is actually profitable. Tips 1–3 address all three problems directly.

Tip 1 — Open a Dedicated Business Bank Account

A separate business account does more than keep things tidy. The practical benefits are concrete:

- Cleaner tax preparation — every deductible expense is already isolated, not buried in personal transactions

- Audit protection — a clear paper trail is your best defense if the IRS asks questions

- Accurate cash flow visibility — you'll know what your business actually earns and spends

- Professional credibility — clients and vendors expect business payment from a business account

When choosing an account, look for low monthly fees, debit card access, and online bill pay. Sole proprietors can often use a separate personal account, but incorporated businesses (LLC, S-Corp) typically need a formal business account. Check with your bank and a tax advisor on the right structure for your entity type.

Tip 2 — Pay Yourself a Consistent Salary

Spending directly from business revenue is a fast path to financial confusion. Instead, designate a fixed transfer from your business account to your personal account — an "owner's draw" — on a regular schedule. This simulates a paycheck even when income varies month to month.

One practical approach: set up an automatic transfer for your minimum living expenses every pay period, then make additional distributions in strong months. Keep in mind that tax treatment differs by business structure — S-Corp owners who pay themselves a formal salary face different requirements than sole proprietors taking draws. A tax professional can clarify which approach fits your entity type.

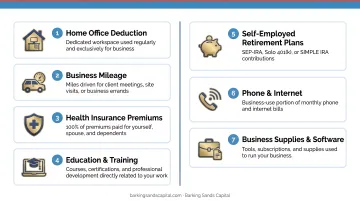

Tip 3 — Track Every Business Expense

Many self-employed individuals leave money on the table by missing deductible expenses. Per IRS Publication 535, an expense is deductible when it is both "ordinary" (common in your trade or business) and "necessary" (helpful and appropriate).

Commonly overlooked deductions include:

- Home office (dedicated workspace used regularly and exclusively for business)

- Business mileage

- Self-employed health insurance premiums

- Retirement plan contributions

- Professional development and education

- Software subscriptions and business tools

- Legal and professional fees

Pay all business expenses from your business account, use bookkeeping software to categorize transactions, and keep digital receipts organized by category. Doing this monthly takes 30 minutes. Doing it at tax time takes days.

Tips 4–5: Understand and Plan for Self-Employment Taxes

W-2 employees split payroll taxes with their employer. Self-employed individuals pay both sides themselves. That's the core shift that catches most new freelancers and business owners off guard.

Tip 4 — Save Consistently for Self-Employment Tax

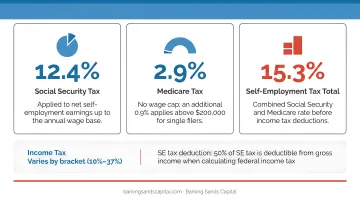

The IRS self-employment tax rate is 15.3%, broken down as:

- 12.4% for Social Security (applied to net earnings up to $184,500 in 2026)

- 2.9% for Medicare (applied to all net earnings)

- 0.9% additional Medicare tax for high earners above $200,000 (single filers) or $250,000 (married filing jointly)

Two details here that many people miss. SE tax applies to 92.35% of net profit, not the full amount — the IRS excludes the employer-equivalent half before calculating, so on $100,000 of net profit, SE tax applies to $92,350. You can also deduct half of your SE tax from your adjusted gross income on Form 1040, which partially offsets the burden.

A practical starting point: set aside 25–30% of net income each quarter for SE tax and federal income tax combined. Your actual rate will depend on income level and applicable deductions.

Tip 5 — Pay Quarterly Estimated Taxes on Time

If you expect to owe $1,000 or more in federal taxes for the year, you're required to pay quarterly estimated taxes using Form 1040-ES. The standard due dates are:

| Quarter | Due Date |

|---|---|

| Q1 | April 15 |

| Q2 | June 15 |

| Q3 | September 15 |

| Q4 | January 15 (following year) |

Missing a payment isn't just inconvenient — the IRS Failure to Pay penalty runs 0.5% per month on unpaid taxes, up to 25%, plus interest. Use the IRS Tax Withholding Estimator to calculate appropriate payment amounts throughout the year.

Reducing what you owe starts with tracking every eligible deduction. Key above-the-line deductions that lower your taxable income:

- Home office deduction

- Self-employed health insurance premiums

- Retirement plan contributions

- The Qualified Business Income (QBI) deduction — eligible self-employed individuals can deduct up to 20% of qualified business income

Tips 6–7: Build a Retirement Strategy for the Self-Employed

Without an employer plan, every dollar of your retirement savings depends entirely on you. The good news: the IRS has created retirement accounts specifically for self-employed individuals with contribution limits that rival (and in some cases exceed) traditional 401(k)s.

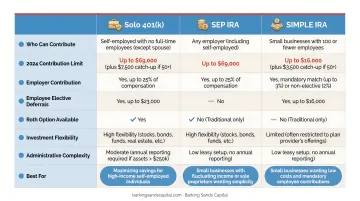

Tip 6 — Choose the Right Retirement Account for Your Situation

Three primary options exist for self-employed individuals:

Solo 401(k)

- Employee deferral limit: $24,500 in 2026

- Additional employer profit-sharing contribution: up to 25% of compensation

- Combined annual cap: $72,000

- Allows Roth contributions and loans

- Best for: self-employed individuals with no non-owner employees

SEP IRA

- Contribute up to 25% of net self-employment earnings, capped at $72,000 in 2026

- Employer contributions only — no employee deferrals

- Simpler to set up than a Solo 401(k)

- If you have employees, you must contribute the same percentage for them as for yourself

- Best for: higher earners who want flexibility and minimal administration

SIMPLE IRA

- Employee deferral limit: $17,000 in 2026

- Requires either a 3% matching or 2% nonelective employer contribution

- Available to businesses with up to 100 employees

- Best for: self-employed individuals with employees who want a straightforward plan

Traditional and Roth IRAs remain available as a baseline, with a 2026 contribution limit of $7,500 — meaningful, but far below the self-employed-specific options above.

Choosing between these accounts depends on your business structure, income level, whether you have employees, and how contributions fit into your annual tax strategy. A fee-based fiduciary advisor — the team at Barking Sands Capital works through exactly this kind of analysis — can match the right vehicle to your situation before you finalize your tax plan for the year.

Tip 7 — Start Early and Automate Contributions

Consistency builds retirement savings more reliably than any single account choice. Set up automatic monthly transfers to your chosen retirement account and treat them like a fixed operating expense — non-negotiable, not discretionary.

One valuable flexibility: SEP IRA contributions can be made up to the tax filing deadline (including extensions) for the prior tax year. This gives self-employed individuals the ability to maximize contributions after calculating annual net income — useful when income varies significantly year to year.

Tip 8: Budget and Save for Unpredictable Income

Variable income requires a different budgeting approach than a salary. Start by calculating your bare-bones budget — the minimum monthly amount needed to cover housing, food, utilities, and essential insurance. This number tells you exactly how much you must earn each month to stay afloat and guides decisions during slow seasons.

Emergency fund target: 6–12 months of living expenses. That's larger than the 3–6 month standard for salaried employees — and for good reason. The CFP Board notes that self-employed individuals face income variability, seasonal slow periods, the risk of losing a major client, and quarterly tax obligations, all of which demand a bigger cushion.

Keep this fund in a high-yield savings or money market account for accessibility while earning a better return than a standard savings account.

To make this systematic, use automatic transfers:

- Simulate a paycheck by transferring a fixed amount from your business account to personal each month

- Build your cushion automatically with a dedicated monthly transfer to your emergency fund

- Automate retirement contributions so they happen before discretionary spending

This "pay yourself first" structure works especially well during high-revenue months — when income spikes, the automation prevents lifestyle inflation from quietly eroding what should be savings.

Tip 9: Protect Yourself with the Right Insurance and Benefits

Self-employment means losing employer-sponsored health coverage, disability income protection, and group life insurance simultaneously. Building your own benefits package is as essential as any other financial decision you'll make.

The three coverage types every self-employed person needs:

Health Insurance

Start by exploring marketplace plans through Healthcare.gov, Medicaid eligibility based on income, or a high-deductible health plan (HDHP) paired with a Health Savings Account (HSA).

The HSA offers a triple tax advantage: contributions are deductible, growth is tax-free, and qualified medical withdrawals are tax-free. Health insurance premiums are also fully deductible on Form 1040 for self-employed individuals not eligible for a spouse's employer plan.

Disability Insurance

Disability insurance is statistically more urgent than life insurance. SSA actuarial data shows that a 20-year-old insured worker has a 25% probability of disability before normal retirement age, compared to a 13% probability of death. Look for "own occupation" coverage, which pays benefits if you can't perform the duties of your specific occupation — even if you could theoretically work in another field.

Life Insurance

Term life insurance provides a cost-effective death benefit that replaces lost income for dependents. For most self-employed individuals without complex estate planning needs, term coverage is a reasonable starting point.

Also consider liability insurance — general business liability or professional liability (errors & omissions) — especially for service-based businesses where client disputes are a meaningful risk.

Tip 10: Think Long-Term — Exit Planning, Estate Planning, and Professional Guidance

For many self-employed individuals, the business itself is one of their most valuable assets. Planning for what happens to that asset — whether through a sale, transfer, or succession — shouldn't wait until retirement is imminent.

Gallup reported in 2025 that about one-third of U.S. business owners had no long-term plan for their business. Among nonemployer business owners, only 9% planned to sell or transfer ownership in the next five years. This is a significant planning gap — especially considering that the Exit Planning Institute estimates only 20–30% of businesses that go to market actually sell.

Exit planning basics for self-employed individuals:

- Determine your exit path early: outright sale, family transfer, employee buyout, or liquidation

- A buy-sell agreement funded by life or disability insurance protects both you and your family if death or disability forces an unexpected ownership transition

- Begin increasing business documentation, systems, and client diversification years before any planned exit

Estate planning essentials — at every age, not just at retirement:

- An up-to-date will

- Correct beneficiary designations on retirement accounts and insurance policies (these override your will)

- Powers of attorney for financial and healthcare decisions

- Review these documents after any major life change: marriage, divorce, birth of a child, business restructuring

Managing exit planning, estate documents, retirement accounts, tax strategy, and insurance coverage in parallel is where things get complicated — and where gaps tend to appear. Barking Sands Capital's proprietary InteProcess™ coordinates all of these areas into a single, unified plan so nothing falls through the cracks between advisors. As an independent, fee-based RIA, Barking Sands Capital is compensated directly by clients, not by commissions on products — which means the advice is built around your situation, not around what pays the most.

Frequently Asked Questions

How much tax will I pay on $30,000 a year as self-employed?

At $30,000 of net self-employment income, SE tax applies to 92.35% of that amount ($27,705), resulting in approximately $4,239 in SE tax (not the full $4,590 many assume). Federal income tax is added on top based on your bracket, though deductions can reduce what you actually owe — consult a tax advisor or use the IRS Tax Withholding Estimator for your specific situation.

What expenses can be written off as self-employed?

Common deductible expenses include home office costs, business mileage, health insurance premiums, retirement plan contributions, professional development, software and subscriptions, and legal or professional fees. Per IRS rules, expenses must be "ordinary and necessary" to your business and should be documented with receipts.

What is the $1,000-a-month rule for self-employed people?

The $1,000-a-month rule is a retirement savings benchmark: for every $1,000 of desired monthly retirement income, you need approximately $240,000 saved at a 5% withdrawal rate, or $300,000 at a more conservative 4% rate. It's a quick way to estimate your retirement savings target based on the income you want.

What retirement accounts are available to self-employed individuals?

The three primary options are the Solo 401(k), SEP IRA, and SIMPLE IRA. All offer tax advantages comparable to employer-sponsored plans, with contribution limits that vary by account type and income. Traditional and Roth IRAs are also available, though their limits are significantly lower.

How much should a self-employed person save in an emergency fund?

Target 6–12 months of living expenses — considerably more than the 3–6 months typically recommended for salaried employees. The larger cushion accounts for income variability, slow seasons, client loss, illness, and the reality that quarterly tax payments are due whether revenue is strong or not.