The stakes are real. According to the College Board's Trends in College Pricing 2024, average published tuition and fees for 2024–25 reached $43,350 at private nonprofit four-year institutions and $11,610 for in-state students at public four-year schools. Meanwhile, 529 plan assets nationally totaled $508.3 billion as of mid-2024 — evidence that families are saving, but the right account still matters.

This article breaks down exactly how each account works, where they differ, and how to choose the right one for your family's situation.

Key Takeaways

- Both accounts offer tax-deferred growth and federal tax-free withdrawals for qualified education expenses

- Coverdell ESAs allow broader investment flexibility but cap contributions at $2,000/year per beneficiary with strict income limits

- 529 plans have no income restrictions, no federal annual cap, and allow lifetime balances into the hundreds of thousands

- Under SECURE Act 2.0, unused 529 funds can now roll into a Roth IRA — ESA funds carry no such option and must be used by age 30

- For most families, a 529 is the stronger primary savings vehicle; income-eligible families often do best holding both accounts simultaneously

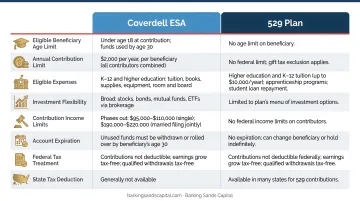

ESA vs. 529: Quick Comparison

| Feature | Coverdell ESA | 529 Plan |

|---|---|---|

| Annual contribution limit | $2,000 per beneficiary (all contributors combined) | No federal limit; gift tax reporting above $19,000/year (2025) |

| Lifetime limit | No federal cap, but $2,000/year caps accumulation | Varies by state; examples: PA $511,758 / CA $529,000 / UT $606,000 |

| Income restrictions | Phase-out: $95K–$110K (single); $190K–$220K (married) | None |

| Beneficiary age limits | Contributions stop at age 18; funds must be used by age 30 | No age restrictions |

| Investment options | Broad brokerage-style flexibility (subject to custodian offerings) | Pre-set portfolios (mutual funds, ETFs); reallocate up to twice/year |

| K–12 expenses | Yes — tuition, books, tutoring, computers | Yes — tuition only, up to $10,000/year |

| College expenses | Yes — tuition, fees, books, room and board | Yes — full range of qualified higher education expenses |

| Financial aid impact | Parental asset (up to 5.64% SAI rate) | Parental asset (up to 5.64% SAI rate) |

| Unused funds | Taxed + 10% penalty if not used by age 30 (unless transferred) | Transfer to family member; roll into Roth IRA under SECURE Act 2.0 |

Note: These rules reflect current federal tax law. State-specific 529 rules — including available tax deductions for contributions — vary significantly. Minnesota and Michigan residents, for example, should confirm their home state's contribution deduction rules and plan options before investing.

What Is a Coverdell Education Savings Account?

A Coverdell ESA is a tax-advantaged trust or custodial account designed to pay for a beneficiary's qualified education expenses from kindergarten through college. It's an investment account with specific IRS rules — not a standard savings account.

How the tax benefit works:

- Contributions are made with after-tax dollars (not deductible)

- The account grows tax-deferred

- Withdrawals are federal income tax-free when used for qualified expenses

Qualified expenses under IRS Publication 970 include tuition, fees, books, supplies, room and board, academic tutoring, computers, and internet access — for both K–12 and post-secondary education.

Key Limitations

Three constraints define the ESA's boundaries:

- $2,000 annual cap — Total contributions from all sources (parents, grandparents, anyone) cannot exceed $2,000 per beneficiary per year

- Income phase-out — Contributors with MAGI between $95,000–$110,000 (single) or $190,000–$220,000 (married filing jointly) face a reduced or eliminated contribution limit

- Age cutoffs — Contributions must stop when the beneficiary turns 18, and all funds must be distributed by age 30 (with an exception for special needs beneficiaries)

Any funds remaining at age 30 face income tax plus a 10% penalty on earnings — unless transferred to a qualifying family member under age 30.

Investment Flexibility: The ESA's Core Appeal

Investment flexibility is the ESA's defining advantage for income-eligible families. According to FINRA, there are virtually no investment restrictions for Coverdell ESA funds (except life insurance contracts), and accounts can be opened at brokerage firms, mutual fund companies, and other financial institutions.

That means access to individual securities and a wider universe of investment choices than most 529 plans allow.

Use Cases and Coordination Pitfalls

The ESA works best for families who:

- Fall under the income threshold

- Have young children (time for the investment flexibility to pay off)

- Want to fund K–12 private school costs alongside college savings

- Plan to contribute close to $2,000 per year and want self-directed portfolio control

Watch out for the grandparent contribution trap. The $2,000 limit applies across all contributors combined. If a grandparent independently opens an ESA for a child whose parents already contributed the full $2,000, the excess triggers a 6% excise tax under IRS Form 5329. Family members need to confirm contribution totals before funding — uncoordinated contributions can trigger that penalty silently.

What Is a 529 Plan?

A 529 plan is a state-sponsored, tax-advantaged investment account (officially a "qualified tuition program" under Section 529 of the tax code) designed to help families save for education costs. There are two types: savings plans and prepaid tuition plans. Savings plans are far more common and are the focus here.

How contributions work:

- After-tax contributions invest in pre-set portfolios (typically mutual funds or age-based options)

- Growth is tax-deferred; withdrawals are federal tax-free for qualified expenses

- No income restrictions for contributors

- Contributions above the 2025 annual gift tax exclusion of $19,000 may require gift tax reporting

Qualified uses include college tuition and expenses, K–12 tuition (up to $10,000/year), registered apprenticeship program expenses, and student loan repayment (up to $10,000 lifetime per individual).

Contribution Room and Lifetime Limits

There is no federal annual contribution cap for 529 plans. State-set aggregate limits vary widely — Pennsylvania caps accounts at $511,758 per beneficiary, California at $529,000, and Utah's my529 accepts contributions up to $606,000. For most families, hitting those ceilings won't be a realistic concern — but the bigger question is what happens to funds you don't end up using.

The SECURE Act 2.0 Roth IRA Rollover Option

The traditional concern about 529 plans — "what if my child doesn't go to college?" — has largely been addressed. Under SECURE Act 2.0, unused 529 funds can be rolled into a Roth IRA for the beneficiary, subject to several conditions:

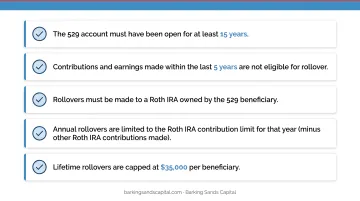

- The 529 account must have been maintained for at least 15 years

- The rollover must be a direct trustee-to-trustee transfer to the beneficiary's Roth IRA

- Annual rollovers are capped by the standard Roth IRA contribution limit, reduced by other IRA contributions that year

- Lifetime rollovers cannot exceed $35,000 per beneficiary

- Contributions and earnings from the prior 5 years are excluded

In practice, this provision converts leftover education savings into a head start on retirement. Barking Sands Capital's CFP® Andrea Cervena incorporates this rollover option when reviewing education funding alongside clients' broader retirement strategies.

Investment Flexibility: What the Rules Allow

The flexibility 529 plans offer in contribution size comes with less flexibility in investments. Per the SEC's investor bulletin on 529 plans, account holders choose from pre-set investment menus rather than self-directing into individual securities. Reallocations are permitted no more than twice per calendar year under federal law.

One important note: you are not required to use your home state's 529 plan. Shopping across states can yield better investment options and lower fees — though you may forfeit any state income tax deduction for contributions.

Use Cases for a 529

The 529 fits families who:

- Earn above the ESA income thresholds

- Want to save more than $2,000 per year

- Have a beneficiary of any age, including older children or adults returning to school

- Need flexibility to change beneficiaries if plans shift

- Have grandparents or extended family who want to contribute without coordination risk

ESA vs. 529: Which Is Right for Your Situation?

The decision comes down to five variables: income level, planned annual contribution amount, your child's current age, appetite for investment control, and how much K–12 coverage matters relative to college savings.

Scenario: Choose an ESA

A family earning under $190,000 (married), with a child under 10, who wants to invest in specific mutual funds or individual securities and plans to contribute around $2,000 per year is a strong ESA candidate. The self-directed investment flexibility can generate meaningful additional growth over a 10+ year horizon.

That said, maxing an ESA doesn't rule out a 529. Many families max the ESA first, then contribute additional dollars to a 529 — capturing investment control on one portion of savings while building the bulk of the fund elsewhere.

Scenario: Choose a 529

A family earning above the ESA income limits, wanting to save $5,000–$10,000+ per year, or a grandparent looking to make a meaningful lump-sum gift without navigating the $2,000 per-contributor coordination issue — these families should go straight to a 529. The contribution room, beneficiary flexibility, and Roth IRA rollover option provide broad long-term utility.

Can You Use Both?

Yes, and for income-eligible families with a strong savings rate, the dual approach makes sense:

- ESA: Self-directed investment flexibility on a smaller portion

- 529: Higher-capacity vehicle for the majority of education savings

- Combined: Full access to both investment control and contribution capacity

Financial Aid Impact

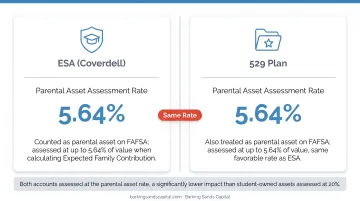

Both parent-owned 529 plans and Coverdell ESAs are treated as parental assets on the FAFSA, assessed at a maximum rate of 5.64% of value (calculated as a 12% parent asset conversion rate multiplied by a maximum 47% parent assessment rate, per the 2025–26 SAI and Pell Grant Eligibility Guide). This makes them among the least financially aid-impactful savings options compared to assets held in the student's own name.

For families weighing these trade-offs alongside retirement contributions, tax deductions, and estate planning, account-type selection rarely stands alone. Barking Sands Capital integrates education funding into broader financial planning — covering retirement, tax strategy, and estate coordination — as part of a single, cohesive process.

Conclusion

Neither account is universally better. The Coverdell ESA gives income-eligible families investment freedom and genuine K–12 versatility within tight contribution and age constraints. The 529 plan offers unmatched contribution room, beneficiary flexibility across life stages, and the Roth IRA rollover provision that eliminates much of the "what if" risk.

For most families, the 529 will carry the bulk of education savings. Those who qualify for the ESA may find real value in holding both.

Starting early and contributing consistently matters more than which account you choose. A financial planner can help you weigh income limits, state tax benefits, and long-term savings goals before committing to a strategy. Barking Sands Capital works with families to fit education funding into a broader financial plan — one that also addresses retirement security and tax efficiency. Their team includes CFP® professionals with hands-on education planning experience.

Reach them at 952-500-8854 (Minnesota) or 248-687-1040 (Michigan).

Frequently Asked Questions

Is it better to put money in a 529 or savings account?

A 529 plan offers significant advantages over a standard savings account for education — specifically, tax-deferred growth and tax-free withdrawals for qualified expenses. A regular savings account provides more flexibility but no tax benefits and is unlikely to keep pace with rising education costs over a 10–18 year savings horizon.

Can a 529 be used for speech therapy?

Speech therapy is generally not a qualified 529 expense unless it qualifies as a special needs service or school-connected educational therapy for an eligible special needs beneficiary. Standalone therapeutic services outside a school program do not meet the IRS definition of qualified education expenses under Publication 970.

Can you have both a Coverdell ESA and a 529 plan for the same child?

Yes. A beneficiary can hold both accounts simultaneously. This dual approach lets income-eligible families use the ESA's self-directed investment flexibility while using a 529 for higher annual contributions.

What happens to ESA or 529 funds if my child doesn't go to college?

Unused funds in either account can be transferred to another qualifying family member. Under SECURE Act 2.0, unused 529 funds may also roll into the beneficiary's Roth IRA (subject to a 15-year holding requirement and a $35,000 lifetime cap), while ESA funds not used by age 30 face income tax plus a 10% penalty on earnings.

Do 529 plans and Coverdell ESAs affect financial aid eligibility?

Both parent-owned 529 and Coverdell ESA accounts are reported as parental assets on the FAFSA and assessed at a maximum rate of 5.64% of their value. This makes them one of the least disruptive asset types for financial aid purposes — far less impactful than assets held directly in the student's name.

Can you roll over a Coverdell ESA into a 529 plan?

Yes. A Coverdell ESA distribution used to fund a 529 for the same beneficiary is treated as a qualified distribution under IRS Publication 970, making the move tax-free.