Introduction

Watching an account balance drop by $80,000 in a single quarter is jarring. For someone who spent 30 years building that number, recession headlines don't feel like abstract economics — they feel personal. That anxiety is valid. But it also tends to produce the most costly financial decisions people will ever make.

The good news: every U.S. recession since 1945 has eventually ended. According to NBER data, the average recession since 1945 has lasted roughly 10 months, while the average expansion has lasted over 64 months. Recessions are real — and temporary.

What this guide covers:

- How recessions threaten retirement portfolios beyond the balance drop

- Strategies for protecting your savings before and during a downturn

- Age-specific adjustments based on your retirement timeline

- The costliest mistakes to avoid when fear takes over

Preparation before a recession matters far more than reacting during one — and these strategies are designed to help you build it.

Key Takeaways

- Sequence of returns risk is the real danger for new retirees — not just the market drop

- A 1–3 year cash buffer is your best defense against forced selling in a downturn

- Down markets are ideal for Roth conversions and tax-loss harvesting

- Panic-selling locks in losses and almost always means missing the recovery

- Age and proximity to retirement should drive your recession strategy

How a Recession Threatens Your Retirement Savings

It's Not Just the Balance Drop

A falling account balance is visible and painful. What's less obvious is the pressure a downturn creates to withdraw at exactly the wrong moment — selling shares when prices are lowest, permanently reducing what's available for recovery.

Market volatility and a formal recession are also related but distinct. Stocks frequently decline before a recession is officially declared, and they often begin recovering while economic news is still grim. Fidelity reports that in 2020, stocks rose 70% from March 23 through December 31 — while the economy was still struggling. Waiting for the "all clear" means missing much of the rebound.

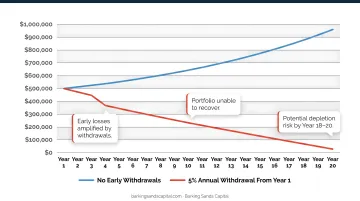

Sequence of Returns Risk: The Retirement-Specific Danger

This is the most underappreciated threat for people entering retirement. If markets drop early in retirement while you're already making withdrawals, you're forced to sell more shares to cover living expenses. That leaves fewer shares to benefit from the recovery — and your portfolio never fully catches up.

Morningstar research makes this concrete: nearly 70% of retirement plan failures in their study involved investment losses within the first five years of retirement. Avoid those early losses, and the failure rate drops to roughly 1% by year 15.

Consider the math: a $1 million portfolio with $40,000 in annual inflation-adjusted withdrawals, hit by a 2000-style equity crash in year one, could be cut nearly in half by year three. The culprit isn't overspending — it's the compounding effect of selling depleted shares to fund withdrawals before prices recover.

Compounding Risks

Recessions don't arrive alone. They often coincide with:

- Job loss for pre-retirees who planned on a few more earning years

- Increased pressure on Social Security and Medicare policy discussions

- Rising costs of living that reduce purchasing power of fixed withdrawals

Each of these forces a different kind of financial adjustment. Facing two or three at once — while also managing a declining portfolio — is exactly the scenario a recession contingency plan is built to handle.

Key Strategies to Protect Your Retirement Portfolio During a Recession

Diversify and Rebalance Your Portfolio

Diversification means spreading your assets across classes — stocks, bonds, cash, and potentially real assets — so no single sector collapse wipes out the whole portfolio. It's the most fundamental form of recession resilience, and it works because different asset classes rarely fall together at the same time or magnitude.

Rebalancing keeps diversification working over time. Strong-performing assets grow to represent a larger share of your portfolio than intended, gradually increasing your risk exposure. Rebalancing means trimming what has grown and adding to what has lagged, returning to your target allocation.

Vanguard recommends checking a diversified portfolio at least once a year. A market downturn can actually serve as a natural rebalancing trigger — buying assets at depressed prices while trimming those that held up better.

For a rough starting point, the 120-minus-age rule is commonly referenced: a 55-year-old might target roughly 65% equities and 35% bonds. Morningstar notes this has largely replaced the older 100-minus-age version given longer life expectancies.

That said, it's a heuristic, not a prescription. Your actual allocation depends on:

- Income sources in retirement (pension, Social Security, rental income)

- Anticipated spending needs and flexibility

- Personal risk tolerance and time horizon

Maintain a Cash Reserve and Liquidity Buffer

The most practical solution to sequence of returns risk is holding 1–3 years of living expenses in cash or cash equivalents (money market funds, short-term CDs). When markets drop, you draw from cash — not from your equity positions — giving investments time to recover before you touch them.

This is the logic behind the bucket strategy:

- Bucket 1: Cash for immediate needs (1–3 years of expenses)

- Bucket 2: Moderate-risk bonds for medium-term replenishment (years 4–10)

- Bucket 3: Long-term growth assets like equities (10+ years out)

Research published by the Financial Planning Association found that a cash-flow-reserve strategy produced plan survival rates up to 6 percentage points higher than drawing directly from investments, and reduced cumulative transaction costs by 88–90% in taxable environments.

The bucket approach also solves a behavioral problem. It removes the temptation to sell equities during a downturn by giving you a clear, separate pool to draw from.

Keep Contributing — Especially When Markets Are Down

Dollar-cost averaging — investing equal amounts at regular intervals regardless of market direction — means you automatically buy more shares when prices are lower. During a downturn, this works in your favor.

Stopping contributions during volatility reverses that advantage and adds a second problem: forfeiting your employer 401(k) match. According to Vanguard's 2025 research, 68% of Vanguard plans with employer contributions offer a matching contribution, with an average employer contribution rate of 4.6%. Pausing contributions to avoid watching your balance fluctuate means giving up guaranteed returns — typically a 50–100% immediate return on the matched portion — in exchange for avoiding discomfort.

The math doesn't support pausing. The discomfort of watching a falling balance is real, but forfeiting a guaranteed employer match to avoid it is a trade most investors would regret.

Recession-Smart Tax and Investment Moves

A market downturn isn't purely bad news. It creates specific tax opportunities that don't exist when markets are rising.

Tax-Loss Harvesting

If holdings are temporarily down, you can sell them to realize a loss that offsets capital gains elsewhere in your portfolio — reducing your tax bill without changing your overall investment exposure. The key is immediately replacing the sold position with a similar (but not identical) holding.

One critical rule: the IRS wash-sale rule prohibits deducting a loss if you repurchase a "substantially identical" security within 30 days before or after the sale. This is a strategy best executed with an advisor who can identify appropriate replacement securities and track the timing.

Strategic Roth Conversions

When account values are lower, converting a portion of a traditional IRA to a Roth IRA means paying income tax on a smaller dollar amount today. The converted funds then grow tax-free — and future withdrawals are also tax-free.

If a market drop reduces your traditional IRA from $500,000 to $380,000, you're converting at a $120,000 discount — locking in a lower tax basis before the account recovers.

This approach works best in years when your income is lower or you've dropped into a more favorable tax bracket. Coordinating the conversion timing with your overall tax picture is where advisors like those at Barking Sands Capital add the most value, using their InteProcess™ framework to align the move with your broader retirement plan.

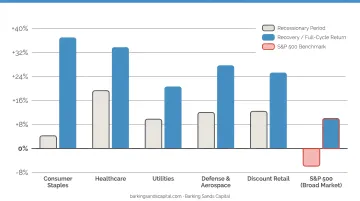

Recession-Resilient Sectors

Within an already-diversified portfolio, certain sectors tend to hold value better during downturns:

- Consumer staples — demand for groceries and household essentials persists regardless of GDP

- Utilities — revenue is relatively stable because people don't stop using electricity or water

- Healthcare — demand is driven by need, not consumer confidence

- Dividend-paying stocks with strong balance sheets and long payout histories

S&P Global data confirms that consumer staples, healthcare, and utilities outperformed the broad market during the March 2020 downturn, when the S&P Global BMI declined 14.3%. That doesn't make them immune to losses, but their relative stability can meaningfully reduce portfolio volatility when other sectors are sliding.

Adjusting Your Strategy Based on Age and Retirement Timeline

In Your 20s and 30s

Time is your most powerful asset. A market drop in your 30s is an opportunity to buy shares at lower prices across a multi-decade accumulation horizon. The greater risk at this stage is being too conservative — an overly bond-heavy portfolio at 32 will underperform over 30+ years of compounding.

Stay invested in a stock-heavy allocation and keep contributing. Time will do the rest.

In Your 40s and 50s

This is the decade to shift from pure accumulation to balanced protection. There's still time to recover from a downturn, but that window narrows every year. Gradually shift toward bonds and lower-volatility assets as retirement approaches.

This is also when building a concrete retirement income plan moves from "someday" to necessary. Key questions to work through now:

- What will annual expenses actually be in retirement?

- What income sources exist (Social Security, pension, part-time work)?

- What portfolio size do you actually need to fund the gap?

These questions don't live in separate silos. Barking Sands Capital's integrated planning approach works through tax, insurance, and investment dimensions together, so the answers actually align.

In Your 60s or Already Retired

The priority shifts from growth to protection. Specific strategies:

- Maintain a cash buffer (Bucket 1) to avoid selling equities during downturns

- Avoid drawing near-term income from volatile equity positions

- Delay Social Security if possible — every year past full retirement age locks in roughly an 8% annual increase in guaranteed monthly income, according to the SSA

If you're retiring into a recession, stress-test your plan. What happens if markets drop 20–30% in your first year of retirement? Knowing your portfolio's probability of success under adverse conditions is more useful than planning only for average-case outcomes.

Mistakes to Avoid When Recession Fears Strike

Panic-Selling

Moving entirely to cash locks in losses and almost always means missing the recovery — which tends to arrive suddenly and concentrate in a short window.

Schwab's analysis shows that missing just the 10 best market days between 2004 and 2023 would have reduced annualized returns from 9.7% to 5.4%. Those best days frequently cluster immediately after the worst days. Investors who fled to cash after a drop are often out of the market when it matters most.

The Vanguard comparison is equally direct: investors who maintained a 60/40 allocation through the March 2020 downturn earned 21% by December 2022. Those who moved to cash earned -2% over the same period.

Early 401(k) Withdrawals

Withdrawing from a 401(k) before age 59½ triggers an IRS penalty of 10% on the taxable portion — on top of ordinary income taxes. A $50,000 withdrawal could cost $15,000 or more depending on your bracket.

Even in genuine financial hardship, a 401(k) loan or drawing from a non-retirement cash reserve is almost always a better option than a permanent, penalized withdrawal.

Trying to Time the Market

Pausing contributions or waiting for the "perfect" moment to reinvest feels safe. It rarely works. DALBAR found that the average equity investor earned 16.54% in 2024 versus the S&P 500's 25.02% return — a gap driven largely by poor timing decisions during volatile periods.

That performance gap narrows considerably when investors work with a fee-based, fiduciary advisor whose compensation doesn't depend on what they sell you. Barking Sands Capital is structured as an independent RIA, meaning advisors cannot earn commissions on managed accounts. When market fear peaks and emotional pressure to react is highest, those incentives matter — your advisor's interests and yours point in the same direction.

Frequently Asked Questions

Frequently Asked Questions

How to protect your retirement savings in a recession?

Diversify your portfolio across asset classes, maintain 1–3 years of living expenses in cash, keep contributing to take advantage of lower prices, and avoid panic-driven decisions. The earlier you build these habits, the less a downturn will cost you.

Where is the safest place to put my 401(k) during a recession?

There's no single "safest" place, but a combination of diversified holdings — including bonds and cash equivalents — is more resilient than moving entirely to cash. Going all-cash forfeits gains when markets rebound. The right allocation depends on your age and time horizon.

Should I stop contributing to my 401(k) during a recession?

Generally no. Stopping contributions means missing the chance to buy shares at lower prices, and forfeiting any employer match.

How does a recession affect Social Security benefits?

Social Security is funded by payroll taxes, not investment markets — so a recession doesn't directly cut your benefits. However, a downturn may make delaying Social Security more attractive, since each year of delay past full retirement age adds roughly 8% in guaranteed monthly income.

What is sequence of returns risk and why does it matter for retirees?

It's the danger that a market drop early in retirement — when withdrawals begin — can permanently reduce portfolio longevity, because selling shares at depressed prices leaves fewer shares to participate in the recovery. A cash buffer covering 1–3 years of expenses is the most practical defense.

Should I move my retirement savings to cash during a recession?

It's a common instinct, but it usually backfires. Panic-selling locks in losses at the worst moment, and most investors who move to cash miss the early — and often sharpest — days of the recovery. Holding a 1–3 year cash cushion lets you cover expenses without selling at a loss, while the rest of your portfolio stays positioned to recover.