Consider this: according to Fidelity's 2025 Retiree Health Care Cost Estimate, a 65-year-old individual may need $172,500 in after-tax savings just to cover healthcare costs in retirement—and that assumes Original Medicare with no employer-provided retiree coverage. For couples, double it.

This guide walks through everything that matters: Medicare's four parts, enrollment rules and their penalties, what you'll actually pay, how to choose supplemental coverage, what Medicare won't touch, and how to weave all of it into a retirement income strategy that holds together.

Key Takeaways

- Medicare's four parts (A, B, C, D) each carry distinct coverage and costs—understanding all four is non-negotiable before retirement

- Late enrollment penalties are permanent; missing the Initial Enrollment Period can cost you for life

- Higher-income retirees pay IRMAA surcharges on Parts B and D based on income from two years prior; today's withdrawal strategy directly shapes tomorrow's premiums

- Original Medicare leaves real gaps: dental, vision, hearing, and long-term care require separate planning

- These decisions connect directly to Social Security timing, tax strategy, and investment withdrawals—they can't be planned in isolation

Understanding Medicare's Four Parts

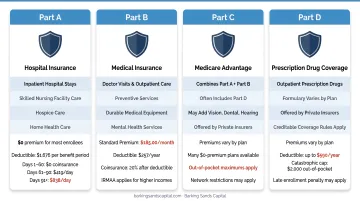

Medicare is built around four distinct parts, each covering a different slice of healthcare:

- Part A – Hospital insurance covering inpatient care, skilled nursing facility care, hospice, and home health care. Premium-free for most people with 10 or more years of qualifying work history, but carries a per-benefit-period inpatient deductible of $1,676 in 2025

- Part B – Medical insurance covering doctor visits, outpatient care, preventive services, and durable medical equipment. Carries a standard monthly premium ($185.00 in 2025) and an annual deductible ($257 in 2025)

- Part C (Medicare Advantage) – A private-insurer alternative that bundles Part A and Part B coverage, usually including Part D, and often adding extras like dental or vision

- Part D – Standalone prescription drug coverage, available as an add-on to Original Medicare

Parts A and B together form Original Medicare—the federal baseline. Before enrolling in a Medicare Advantage plan, you must first enroll in Original Medicare.

Original Medicare vs. Medicare Advantage

Which path you choose affects your provider flexibility, monthly costs, and whether you can add a Medigap policy later.

Original Medicare lets you see any provider that accepts Medicare nationwide—no referrals, no network restrictions. It's the more flexible option, particularly for retirees who travel frequently, split time between states, or need specialist access without prior authorization.

Medicare Advantage plans operate through private insurers using HMO or PPO networks. They often carry $0 or low monthly premiums and may include dental, vision, and hearing benefits Original Medicare excludes. The tradeoff: narrower provider networks and more administrative friction.

Where Medigap Fits

If you go with Original Medicare, Medigap (Medicare Supplement Insurance) is the tool that fills the cost-sharing gaps—covering deductibles and coinsurance that Original Medicare leaves on you. It can significantly reduce out-of-pocket exposure.

Medigap cannot be combined with Medicare Advantage. If you enroll in an Advantage plan, no Medigap policy can cover that plan's copays, deductibles, or premiums.

Who Qualifies and When to Enroll

Eligibility Pathways

Most people qualify at age 65 if they're U.S. citizens or permanent residents with a qualifying work or Social Security history. Three under-65 pathways also exist:

- Received Social Security disability benefits for at least 24 months

- Diagnosed with end-stage renal disease (ESRD) requiring dialysis or a kidney transplant

- Diagnosed with ALS—Medicare begins in the first month disability benefits are received

The Three Enrollment Windows

| Window | Timing | Key Notes |

|---|---|---|

| Initial Enrollment Period (IEP) | 7 months centered on your 65th birthday (3 months before, birthday month, 3 months after) | Most critical window—missing it triggers permanent penalties |

| Annual Open Enrollment | October 15 – December 7 | For switching plans; changes take effect January 1 |

| Special Enrollment Period (SEP) | Triggered by qualifying life events | Losing employer coverage, moving, etc. |

Creditable Coverage and Delayed Enrollment

One exception to the IEP deadline applies if you're still working at 65 with employer coverage—you may delay Part B and Part D without penalty, provided the employer has 20 or more employees. At organizations that size, the group plan pays first and Medicare pays second, which qualifies as creditable coverage and shields you from late-enrollment penalties.

This exemption does not apply to COBRA, retiree health plans, or small-employer plans (fewer than 20 employees). If you're on any of those at 65, enroll in Medicare on time.

Penalties for missing the window:

- Part B: An extra 10% added to your premium for each full 12-month period you went without coverage—permanently

- Part D: 1% of the national base beneficiary premium ($38.99 in 2026) multiplied by the number of months without creditable drug coverage—also permanent

What Medicare Actually Costs: Premiums, Deductibles, and IRMAA

The 2025 Cost Baseline

| Cost Item | 2025 Amount |

|---|---|

| Part B standard monthly premium | $185.00 |

| Part B annual deductible | $257 |

| Part A inpatient deductible (per benefit period) | $1,676 |

| Part D national base beneficiary premium | $36.78 |

For a married couple, every one of these figures doubles—they're per-person costs.

IRMAA: The Surcharge Higher-Income Retirees Pay

IRMAA (Income-Related Monthly Adjustment Amount) adds surcharges on top of standard Part B and Part D premiums for beneficiaries above certain income thresholds. The Social Security Administration uses your MAGI from two years prior to calculate these surcharges.

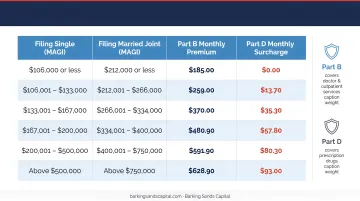

2025 IRMAA Tiers:

| Individual MAGI | Joint MAGI | Part B Total Premium | Part D Add-On |

|---|---|---|---|

| ≤ $106,000 | ≤ $212,000 | $185.00 | $0 |

| $106,001–$133,000 | $212,001–$266,000 | $259.00 | $13.70 |

| $133,001–$167,000 | $266,001–$334,000 | $370.00 | $35.30 |

| $167,001–$200,000 | $334,001–$400,000 | $480.90 | $57.00 |

| $200,001–$499,999 | $400,001–$749,999 | $591.90 | $78.60 |

| ≥ $500,000 | ≥ $750,000 | $628.90 | $85.80 |

What Counts as MAGI for IRMAA

MAGI for IRMAA purposes includes:

- Taxable retirement distributions (401(k), traditional IRA)

- Capital gains from investments or a home sale

- Interest and dividend income

- Roth conversion amounts

A single large event—a Roth conversion, a home sale, or a required minimum distribution—can push your income into a higher IRMAA tier. You won't see the higher premium bill until two years later, long after the income event is forgotten.

Appealing an IRMAA Surcharge

If your income has dropped due to retirement, reduced work hours, divorce, or death of a spouse, you can appeal the surcharge using SSA Form SSA-44. This is one of the most overlooked tools in Medicare planning—IRMAA surcharges are not set in stone if your circumstances have changed.

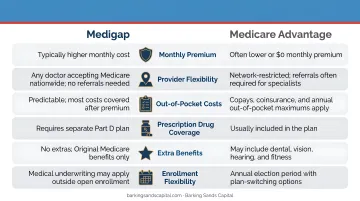

Medigap vs. Medicare Advantage: Which Path Makes Sense?

These two supplemental paths are mutually exclusive. Choosing one closes the door on the other.

Medigap: Predictable Costs, Maximum Flexibility

Medigap plans charge higher monthly premiums but sharply reduce year-to-year cost variability. With Plan G—the most popular Medigap option, held by nearly 5.3 million enrollees as of 2023—your annual out-of-pocket exposure is essentially limited to the Part B deductible ($257 in 2025) plus your monthly premium.

Average Plan G premiums ran around $164/month in 2023, ranging from $140 in Washington, D.C. to $236 in New York, according to KFF. Premiums also vary by age and insurer.

Plans C and F, which covered the Part B deductible, are no longer available to anyone who became newly eligible for Medicare on or after January 1, 2020, making Plan G the most comprehensive option for new enrollees.

Medicare Advantage: Lower Premiums, Variable Risk

Advantage plans frequently advertise $0 or low monthly premiums, which looks appealing on paper. But a serious illness changes the math quickly. The 2025 maximum out-of-pocket (MOOP) limit for in-network services is $9,350. If you have back-to-back medical events spanning two calendar years, you could hit that MOOP twice.

The practical risk: someone who chooses Medicare Advantage for the low premium and then develops a complex condition may face significantly more out-of-pocket exposure than a Medigap enrollee would.

Key tradeoffs to weigh before choosing Advantage:

- Premiums: Often $0/month, but cost-sharing adds up fast with heavy use

- Network restrictions: Most plans require in-network providers or referrals

- MOOP exposure: Up to $9,350/year in-network; out-of-network costs may be unlimited

- Extra benefits: Many plans include dental, vision, and drug coverage

The Medigap Enrollment Window You Can't Ignore

That tradeoff analysis only matters if you can actually get Medigap coverage when you want it. Your Medigap Open Enrollment Period is a one-time, six-month window starting when your Part B begins at age 65. During this window, insurers cannot deny coverage or charge higher premiums based on pre-existing conditions.

After this window closes, insurers in most states can apply medical underwriting. Getting Medigap coverage with significant health conditions later in life may be expensive or impossible. A handful of states offer broader guaranteed-issue protections year-round — Connecticut, New York, Massachusetts, and Maine among them — but most do not.

What Medicare Doesn't Cover—And How to Plan for It

The Coverage Gaps That Cost Retirees Most

Original Medicare excludes several categories that represent real financial exposure:

- Dental care – Routine cleanings, fillings, extractions, and major dental work are not covered

- Vision – Eye exams for prescription glasses, glasses themselves, and contacts are excluded

- Hearing aids – Neither the devices nor the fitting exams are covered

- Long-term custodial care – The largest gap by far

Some Medicare Advantage plans include limited dental and vision benefits, but coverage varies widely and isn't comprehensive.

Long-Term Care: The Retirement Risk Nobody Plans for Until Too Late

Medicare covers short-term skilled nursing facility care under very specific conditions—up to 100 days per benefit period, following a qualifying inpatient hospital stay of at least three consecutive days. It does not cover custodial care, assisted living, or long-term home health aide services.

According to the Administration for Community Living, someone turning 65 today has nearly a 70% chance of needing some form of long-term care services. The 2024 national median costs: $70,800 per year for assisted living and $111,325 per year for a semi-private nursing home room, per Genworth/CareScout data.

These figures make long-term care the most significant uninsured financial risk most retirees carry. Three approaches exist: traditional LTC insurance, hybrid life/LTC policies, and self-funding. The right fit depends on your health status, asset levels, and whether you're still insurable at the time you're planning.

Other Gaps Worth Planning For

- Pre-Medicare coverage – Retirees who leave work before 65 need bridge coverage through COBRA, an ACA marketplace plan, or a spouse's employer plan; this period carries its own costs and planning requirements

- Over-the-counter products – Vitamins, most OTC medications, and health aids aren't covered

- Medical transportation – Especially relevant for retirees in rural areas, non-emergency transport to appointments isn't a standard Medicare benefit

How to Connect Medicare to Your Broader Retirement Income Strategy

Medicare doesn't exist in a vacuum. The decisions you make about withdrawals, Social Security, and HSAs directly shape what you pay for healthcare coverage.

Withdrawal Strategy and IRMAA

Because IRMAA is calculated from MAGI two years back, the sequencing of retirement account withdrawals matters more than most retirees realize. A year of heavy traditional IRA distributions can push you into a higher IRMAA bracket—and you won't know until the bill arrives.

Maintaining a mix of account types (traditional IRA, Roth IRA, taxable accounts) gives you flexibility to manage taxable income in years where IRMAA exposure is high. Barking Sands Capital's tax planning and Roth conversion services coordinate these decisions directly—their IRMAA Strategies service works to reduce surcharges and protect retirement assets from unnecessary premium costs.

Social Security Timing

Claiming Social Security early raises your taxable income and may trigger or worsen IRMAA surcharges. Delaying benefits lowers current taxable income but changes the premium calculation differently in later years. Once Social Security begins, Part B premiums are automatically deducted from your monthly benefit check.

Model Social Security and Medicare costs together. Treating them as separate decisions is among the costliest planning mistakes retirees make.

HSA Strategy Around Medicare Enrollment

Once you enroll in any part of Medicare—including premium-free Part A—HSA contributions must stop. If you're also collecting Social Security when you apply, Part A can be backdated up to six months, which means you could inadvertently make ineligible contributions without realizing it.

Stop contributions at least six months before you plan to apply.

The flip side: existing HSA funds can be used tax-free to pay Medicare Part B, Part D, and Medicare Advantage premiums, as well as deductibles and qualified medical expenses. (Note: Medigap premiums are not eligible for tax-free HSA reimbursement.) A well-funded HSA heading into retirement is one of the most valuable healthcare assets you can carry.

Annual Plan Review

Medicare plans change every fall. Premiums, drug formularies, and provider networks can all shift between years. Review your Annual Notice of Change document each October before the Annual Enrollment Period (October 15–December 7) closes. A plan that made sense last year may not be the right fit this year.

Working With an Advisor Who Integrates All of This

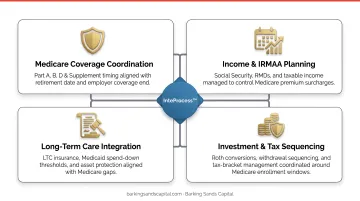

Effective Medicare planning means coordinating several moving parts at once:

- Enrollment timing and coverage selection (Medigap vs. Advantage)

- IRMAA management and withdrawal sequencing

- Social Security timing relative to premium calculations

- HSA drawdown strategy in retirement

Each decision affects the others. Handling them in isolation leaves money on the table.

At Barking Sands Capital, advisor Curtis Hewitt specializes in Medicare Planning and Long-Term Care. The team's proprietary InteProcess™ coordinates these decisions across legal, insurance, tax, and retirement planning disciplines so clients aren't left managing the moving parts on their own. Medicare planning is available as a standalone service or as part of a comprehensive wealth management engagement—whichever fits your situation. Reach Curtis and the team at 952-500-8854 (Minnesota) or 248-687-1040 (Michigan).

Frequently Asked Questions

Do financial planners help with Medicare?

Yes. Financial planners help time enrollment to avoid penalties, model IRMAA surcharges based on projected income, evaluate Medigap versus Medicare Advantage, and integrate healthcare costs into your retirement income plan. Medicare planning works best when it's coordinated with Social Security timing and withdrawal strategy—not handled separately.

Does lupus qualify for Medicare before age 65?

Lupus alone does not qualify someone for early Medicare. However, if lupus causes end-stage renal disease requiring dialysis or a transplant, or if the individual qualifies for Social Security Disability Insurance (SSDI) and has received benefits for 24 months, Medicare may be available before 65.

Is metformin covered by Medicare?

Metformin is covered under most Medicare Part D plans, but tier placement and copay amounts vary by plan. Use Medicare's Plan Finder tool to verify formulary inclusion and costs for your specific plan before each enrollment period.

When should I enroll in Medicare if I'm still working?

If you're covered under an employer group plan at a company with 20 or more employees, you may delay Part B and Part D without penalty. Verify your plan qualifies as creditable coverage and start the enrollment process at least three months before losing that coverage to avoid a gap.

What is IRMAA and how can I reduce it?

IRMAA is a surcharge on Part B and Part D premiums for higher-income beneficiaries, calculated from your MAGI two years prior. You can reduce it by managing taxable income before retirement, timing large asset sales carefully, or filing SSA Form SSA-44 if income dropped due to retirement or a qualifying life event.

Can I use my HSA to pay for Medicare expenses?

Yes—existing HSA funds cover Medicare Part B, Part D, and Medicare Advantage premiums, plus deductibles and qualified expenses, all tax-free. New contributions must stop once you enroll in any part of Medicare, and Medigap premiums do not qualify for tax-free reimbursement.