Introduction

"Do I have enough saved to retire?" It's the question nearly every pre-retiree asks. But it's only one piece of a much larger puzzle.

Today's retirement can span 25–35 years. CDC data shows that a 65-year-old man can expect to live another 18.2 years on average, and a woman another 20.7 years — and those are averages, not ceilings. Healthy retirees and couples routinely plan for 30+ year horizons.

A savings balance alone can't protect against the risks that come with a multi-decade retirement:

- Rising healthcare and prescription costs

- Tax complexity during the distribution phase

- Long-term care needs that can erode assets quickly

- Estate decisions that shape how wealth transfers to the next generation

Holistic retirement planning is an integrated approach that coordinates investments, income strategy, tax efficiency, healthcare, estate planning, and lifestyle design into one cohesive plan — instead of managing each piece separately.

What follows covers the core components of a holistic plan, the strategies that protect income and health across a long retirement, and a practical framework you can start applying now.

Key Takeaways

- Retirement now spans 20–35 years, creating risks that a savings-focused plan alone cannot address

- Healthcare costs for a couple retiring at 65 can exceed $345,000 — not including long-term care

- Tax diversification across pre-tax, Roth, and taxable accounts gives retirees flexibility to minimize lifetime taxes

- 56% of people turning 65 will need some form of long-term care — yet Medicare covers very little of it

- Only 24% of Americans currently have a will; beneficiary designations on retirement accounts can override estate plans entirely

- Integration across tax, legal, insurance, and investment decisions — not just portfolio size — determines retirement security

Why Holistic Retirement Planning Matters Today

The traditional model — save a set percentage, invest in a 401(k), retire at 65 — was designed for a shorter retirement era. It focused almost entirely on accumulation. But accumulation alone leaves three critical risks unaddressed.

The Risks Accumulation Doesn't Cover

- Sequence-of-returns risk: According to Charles Schwab, a $1M portfolio taking 15% losses early in retirement with $50,000 annual withdrawals can be depleted in about 18 years — while the same losses occurring in years 10 and 11 leave nearly $400,000 after that same 18-year period. Timing matters as much as total return.

- Inflation erosion: Healthcare costs inflate at roughly twice the rate of general CPI, according to HealthView Services — meaning a plan built around today's expenses will fall short in year 15 or 20.

- Longevity risk: Boston College's Center for Retirement Research found 39% of working-age households are at risk of being unable to maintain their pre-retirement standard of living. That's not a fringe problem.

Two Compounding Pressures

Healthcare consistently ranks as one of the largest retirement expenses — and one of the most underestimated (more on the numbers below).

Tax complexity grows sharply once distributions begin. Required Minimum Distributions (RMDs) start at age 73, and without proactive planning during the accumulation phase, retirees can find themselves in higher tax brackets than expected — triggering Medicare surcharges (IRMAA), increasing taxes on Social Security benefits, and reducing flexibility.

Why Fragmented Planning Creates Gaps

Many people work with a tax preparer, an investment advisor, an insurance agent, and an estate attorney — each operating independently. When these professionals don't communicate, decisions made in one area can undermine another.

A Roth conversion that looks attractive in isolation may conflict with Medicare cost thresholds. An estate plan drafted years ago may have outdated beneficiary designations that override the will entirely.

That's the case for integration — and it shapes every component of a retirement plan worth having.

The Core Components of a Holistic Retirement Plan

A holistic retirement plan weaves together five interconnected pillars: lifestyle vision, financial foundation, income strategy, healthcare planning, and legacy goals. Weakness in any single pillar creates vulnerability across the entire plan.

Lifestyle Vision and Goals

Lifestyle vision comes first, before any financial target gets set. Travel preferences, housing choices, family proximity, part-time work, and hobbies directly determine how much income is needed and how assets should be allocated. Without this clarity, financial targets are arbitrary numbers.

Financial Foundation

The financial foundation covers three things:

- Diversified portfolio aligned with risk tolerance and time horizon

- Maximizing tax-advantaged contributions throughout the accumulation phase

- A conversion strategy that shifts accumulated assets into reliable income — not just grows them

For 2026, the IRS sets the 401(k) elective deferral limit at $24,500, with an $8,000 catch-up for those 50+ and an $11,250 higher catch-up for employees who turn 60–63 during the year. IRA contribution limits sit at $7,500, with a $1,100 catch-up for those 50+. These limits represent meaningful levers — especially in the final decade before retirement.

Building that foundation only matters if you have a plan for turning it into income. That's where retirement income strategy takes over.

Retirement Income Strategy

A holistic income plan goes well beyond withdrawal rates. It optimizes multiple streams simultaneously:

- Social Security timing — claiming at 70 versus 62 can mean the difference between 70% and 124% of your full monthly benefit (per SSA data for those born in 1960 or later)

- RMD management — IRS requires distributions from traditional IRAs and 401(k)s starting at age 73; poor planning can stack these on top of Social Security and push retirees into higher brackets

- Tax-efficient withdrawal sequencing — drawing from taxable, tax-deferred, and Roth accounts in the right order substantially reduces lifetime tax burden

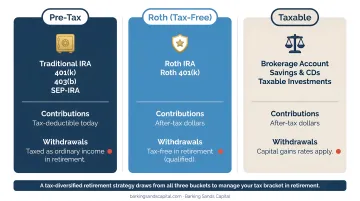

Building a Tax-Efficient Retirement Income Strategy

Tax planning during retirement is not a one-time event. It's an ongoing annual decision about which accounts to draw from, when to convert, and how to sequence income.

Tax Diversification: Why Account Type Matters

Holding assets across three "buckets" gives you flexibility each year:

| Account Type | Tax Treatment | Examples |

|---|---|---|

| Pre-tax (tax-deferred) | Contributions deducted; withdrawals taxed | Traditional 401(k), Traditional IRA |

| Post-tax (tax-free growth) | After-tax contributions; withdrawals tax-free | Roth IRA, Roth 401(k) |

| Taxable | No upfront deduction; capital gains treatment | Brokerage accounts |

By drawing from the right bucket based on your income each year, you can stay in lower tax brackets, avoid IRMAA surcharges, and reduce the size of future RMDs.

Roth Conversion Strategy

The window between retirement and age 73 (when RMDs begin) is often the most valuable period for Roth conversions. Income is lower, tax brackets are more favorable, and every dollar converted reduces future RMD obligations.

Consider a retiree who stops working at 65 and defers Social Security until 70 — that's five years of relatively low taxable income. Converting portions of a traditional IRA to Roth during this window means paying tax now at a lower rate, which shrinks future RMD obligations.

Vanguard's research on Roth conversions evaluates these decisions by comparing current versus expected future marginal tax rates — the key variable most people overlook.

Social Security Timing as a Tax Decision

Social Security timing carries significant tax consequences, not just income ones. Delaying to 70 increases your monthly benefit to 124% of your full retirement amount, but it also affects how other income sources are sequenced in the years before claiming. Coordinating Social Security timing with Roth conversions and withdrawal sequencing can add years to how long your portfolio lasts.

Small business owners face added complexity in this area. SEP-IRA balances, Solo 401(k) proceeds, and business sale proceeds can all create large taxable events in the same year. Key intersections to plan for include:

- SEP-IRA or Solo 401(k) distributions landing in a high-income year

- Business sale proceeds triggering capital gains alongside ordinary income

- Exit timing that pushes income into a higher bracket just before RMDs begin

A holistic plan accounts for how business exit timing intersects with personal retirement tax exposure.

Healthcare, Long-Term Care, and Medicare Planning

Healthcare is one area where retirement planning most often falls short — not because people ignore it, but because the numbers are genuinely difficult to fully grasp.

The Cost Reality

Fidelity estimates a 65-year-old couple retiring in 2025 needs approximately $345,000 after tax for retirement healthcare costs. A single person needs $172,500. Critically, these figures exclude long-term care entirely.

EBRI's 2026 data shows nearly 6 in 10 workers said healthcare costs hurt their ability to save, and 2 in 5 retirees reported higher-than-expected healthcare expenses.

Medicare Enrollment: What You Need to Know

Medicare has four main parts:

- Part A: Hospital coverage (generally premium-free if you've worked 10+ years)

- Part B: Medical/outpatient coverage (monthly premium required)

- Part C (Medicare Advantage): Bundled alternative through private insurers

- Part D: Prescription drug coverage

Missing your initial enrollment window triggers lifetime premium penalties for Parts B and D. The choice between Original Medicare and Medicare Advantage deserves careful comparison based on your health history, preferred providers, and drug needs. This is a meaningful financial decision with long-term cost implications.

Long-Term Care: The Gap Medicare Doesn't Fill

AARP reports that 56% of people turning 65 between 2021 and 2025 will need long-term services and supports during their lifetime. Medicare covers skilled nursing care for short periods after a qualifying hospital stay, but covers zero ongoing custodial care — help with bathing, dressing, eating.

2025 national median costs (CareScout data):

- Non-medical in-home caregiver: $35/hour

- Assisted living: $6,200/month

- Private nursing home room: $10,798/month

Planning options include traditional long-term care insurance, hybrid life/LTC policies, or deliberate self-funding. Each carries different cost, flexibility, and qualification trade-offs — and all are significantly easier to structure before health issues affect your eligibility.

HSAs: The Underused Healthcare Reserve

A Health Savings Account (HSA) offers triple tax advantages: contributions are pre-tax, growth is tax-deferred, and withdrawals for qualified medical expenses are tax-free. For 2026, contribution limits are $4,400 for self-only and $8,750 for family coverage, with an additional $1,000 catch-up for those 55+.

Starting HSA contributions a decade or more before retirement builds a dedicated healthcare reserve. Few vehicles offer this level of tax efficiency for a cost that virtually every retiree will face.

Estate Planning and Preserving Your Legacy

A 2025 Caring.com survey found only 24% of Americans have a will and just 13% have a living trust. That means most retirees are leaving critical decisions to state default laws — not their own intentions.

The Documents Every Retiree Needs

- Will or trust — directs asset distribution and, if applicable, names guardians

- Durable power of attorney (financial and medical) — designates someone to act on your behalf if you're incapacitated

- Healthcare proxy/advance directive — documents your medical wishes

- Updated beneficiary designations — on every retirement account and insurance policy

Beneficiary designations override wills — and that last item on the list is where many people make costly mistakes. A Wall Street Journal case highlighted a situation where an ex-girlfriend stood to inherit a $1 million retirement account simply because a decades-old beneficiary form was never updated. Review designations after every major life event: marriage, divorce, or the death of a named beneficiary.

The Role of Trusts

A revocable living trust can help assets avoid probate, maintain privacy, and give you control over how and when heirs receive assets. For those with larger estates, blended families, or minor beneficiaries, a trust adds structure that a will alone cannot provide.

Trusts also intersect with tax planning in ways worth understanding. For 2026, the federal estate tax basic exclusion is $15,000,000 per individual (updated under the One Big Beautiful Bill), with an annual gift tax exclusion of $19,000 per recipient. Most estates won't reach the federal threshold, but state estate taxes and beneficiary designation errors remain real planning risks at any asset level.

The Psychological Side of Retirement

Estate documents handle what happens to your assets — but holistic planning also addresses what happens to you. The loss of identity, structure, and purpose that accompanies leaving a career is one of retirement's most underestimated challenges. Many retirees are caught off guard by how disorienting the transition feels.

A complete plan intentionally addresses social engagement, community involvement, hobbies, and personal goals alongside investment strategy. Advisors at Barking Sands Capital incorporate this kind of life-planning conversation into their process — because financial security and personal fulfillment aren't separate goals.

How to Start Your Holistic Retirement Plan

A 6-Step Action Framework

- Define your retirement lifestyle vision — timeline, location, activities, and rough monthly income target

- Assess your complete financial picture — all assets, liabilities, income sources (Social Security, pension, rental), and insurance coverage

- Build or review your investment and income strategy — including withdrawal sequencing and Roth conversion opportunities

- Address healthcare coverage gaps — Medicare enrollment timing, long-term care options, HSA funding

- Update or create estate planning documents — will, trust, power of attorney, beneficiary designations

- Schedule annual reviews — tax laws, healthcare costs, and life circumstances change; your plan should too

What Integration Actually Looks Like

The difference between a piecemeal financial plan and a holistic one is coordination. When an independent, fee-based advisor acts as a central hub — working alongside tax professionals, estate attorneys, and insurance specialists — every decision reinforces the overall plan rather than creating unintended conflicts.

Barking Sands Capital's proprietary InteProcess™ does exactly this — integrating legal, insurance, tax, retirement, and financial planning into one fully coordinated process. Clients work with a unified team rather than juggling five separate professional relationships. That means a Roth conversion decision gets evaluated at the same time against tax bracket implications, Medicare surcharge thresholds, and estate planning objectives — not in isolation.

What to Look for in a Retirement Planning Advisor

- Fiduciary duty — your advisor is legally bound to prioritize your interests, not earn commissions on products

- Fee-only or fee-based compensation — no hidden incentives tied to what they recommend

- Relevant credentials — CFP® and ChFC designations require rigorous multi-discipline training, not just investment coursework

- Cross-disciplinary coordination — can actively collaborate with your tax preparer, estate attorney, and healthcare specialists

Frequently Asked Questions

What is holistic retirement planning?

Holistic retirement planning is a comprehensive approach that integrates financial, health, lifestyle, tax, and estate planning into one unified strategy, rather than managing each area in isolation. The goal is to ensure every planning decision supports overall retirement security and quality of life, not just portfolio growth.

What is the $1,000-a-month rule for retirees?

The $1,000-a-month rule suggests retirees need approximately $240,000 in savings for every $1,000 of desired monthly income, based on a 5% withdrawal rate. It's a useful rough benchmark, but a holistic plan replaces these rules of thumb with models built on actual income needs, tax exposure, healthcare costs, and longevity assumptions.

What are the three C's of retirement?

The three C's are commonly identified as Cash flow (sustainable income throughout retirement), Coverage (healthcare and insurance protection), and Care (long-term care planning). Most plans address cash flow adequately but underinvest in coverage and care — the two areas most likely to derail an otherwise solid strategy.

How early should I start holistic retirement planning?

Earlier is better, since compound growth, HSA accumulation, and tax diversification all benefit from time. That said, clients already in or near retirement still gain significantly from integrated planning, particularly around distribution sequencing, Medicare timing, and estate documents.

How much do healthcare costs affect retirement savings?

Fidelity estimates a couple retiring at 65 in 2025 will need $345,000 after tax for healthcare costs, excluding long-term care. Failing to budget for healthcare is one of the most common reasons retirement plans fall short, especially given that medical inflation runs at roughly twice general CPI.

What should I look for when choosing a retirement planning advisor?

Prioritize fiduciary duty, fee-only or fee-based compensation (no product commissions), and credentials such as CFP® or ChFC. Beyond that, look for an advisor who actively coordinates across tax, estate, healthcare, and investment planning, not one who treats each as a separate conversation.