This scenario plays out far too often. According to a 2025 Gallup report, roughly half of U.S. small business owners either plan to close their business or have no long-term plan at all. Yet estate planning for business owners isn't simply about writing a will — the business itself is both a major asset and an ongoing responsibility that demands its own strategic framework.

This guide covers everything a small business owner needs to know: the core documents, succession planning mechanics, tax minimization strategies, life insurance tools, and the mistakes that quietly derail even well-intentioned plans.

Key Takeaways

- Personal wealth and business assets are tightly linked — most owners don't plan for what that means at death or disability

- A will, revocable trust, durable power of attorney, and buy-sell agreement are the core documents every owner needs

- Succession planning and tax strategy must be coordinated — not treated as separate exercises

- Life insurance funds buyouts and replaces income — two functions that matter most when a business is most vulnerable

- Estate plans should be reviewed every 2-3 years and after major business or life events

Why Estate Planning Is Uniquely Critical for Small Business Owners

Most small business owners hold the majority of their personal net worth inside the business itself. That concentration creates a specific kind of risk: if the business falters during an ownership transition, the family loses both the asset and the income stream simultaneously.

The generational transition data is sobering. The Conway Center for Family Business reports that only about 30% of family-owned businesses successfully transition to the second generation, 12% remain viable into the third, and just 3% make it to the fourth generation or beyond. Poor planning — not poor business performance — drives most of those failures.

Why Owners Delay (And Why That's Especially Costly)

Business owners delay estate planning for understandable reasons:

- Confronting mortality feels premature when the business demands daily attention

- Documenting ownership structures raises privacy concerns many owners prefer to avoid

- Separating personal and business finances is difficult, and most delay until it becomes urgent

- Assuming family or partners will figure it out when the time comes

Business owners face a higher cost of delay than most. Without a buy-sell agreement, a funded succession plan, or a durable power of attorney in place, a single unexpected event — death, disability, or divorce — can force a fire sale of a business that took decades to build.

Core Estate Planning Documents Every Business Owner Needs

A solid business estate plan doesn't rest on a single document. It requires several coordinated instruments working together, each covering a different failure scenario.

The foundational documents every business owner needs:

- Last will and testament — names heirs, designates an executor, and directs how business interests should be handled

- Revocable living trust — avoids probate, keeps the estate private, and preserves business continuity

- Durable financial power of attorney — authorizes a trusted person to manage business affairs during incapacity

- Healthcare directive — covers medical decisions separately, freeing the financial POA to focus on business operations

- Buy-sell agreement — governs ownership transfer at death, disability, retirement, or other triggering events

Wills vs. Trusts: Which Does Your Business Need?

A will is the starting point, but it has a significant limitation: it goes through probate. According to Nolo, probate commonly takes several months to over a year, and estates involving federal estate tax returns or litigation can take several years. During that time, a business without a clear operational authority can lose clients, employees, and value.

A revocable living trust solves this directly. Because trust property is legally owned by the trust — not the decedent — it passes outside probate entirely. The Oregon State Bar confirms that avoiding probate is one of the primary reasons individuals use revocable trusts. For business owners, this means operations can continue without court-imposed delays.

An irrevocable trust serves a different purpose: removing assets from the taxable estate. The tradeoff is surrendering control; once you transfer assets irrevocably, you cannot reclaim them. Most business owners use both structures together: a revocable trust for continuity and privacy, and one or more irrevocable trusts for tax planning.

Coordinating two trust structures while managing a business isn't straightforward. Barking Sands Capital addresses this through their proprietary InteProcess™, which brings legal, insurance, tax, and financial planning professionals together rather than treating each document as an isolated task.

Power of Attorney and Healthcare Directives

A durable financial power of attorney is not optional for business owners. Without it, a court must appoint a guardian before anyone can legally act on the owner's behalf during incapacity. That process can take weeks, and there's no guarantee the appointed person will know anything about your business.

A properly drafted financial POA explicitly authorizes a trusted agent to:

- Vote shares and sign business agreements

- Access business bank accounts and financial institutions

- File tax returns and manage tax matters

- Operate, modify, or transfer business interests

A healthcare directive (living will) handles medical decisions separately, which matters more than it might seem. When a healthcare crisis hits, family members should be focused on medical decisions — not scrambling to figure out who can sign a vendor contract.

Building a Business Succession Plan That Works

A succession plan answers three things in writing: who takes over, under what conditions, and through what financial mechanism. Without those answers documented, the business's fate gets decided by default, often in ways the owner never intended.

PwC's U.S. Family Business Survey found that only 34% of U.S. family businesses had a robust, documented, and communicated succession plan. That leaves the majority operating without a clear roadmap for one of the most consequential transitions a business ever faces.

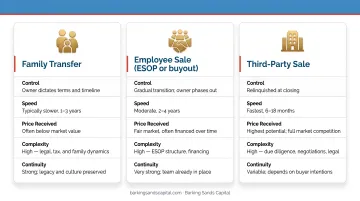

The Three Main Succession Paths

1. Transfer to a family member Passing the business to a child or relative requires more than naming them as heir. It demands honest planning around family dynamics, equitable treatment of non-active siblings, and whether the successor actually has the skills and interest to run the business. Skipping these conversations creates the conflicts that destroy family businesses.

2. Sale to a key employee or management team This path often makes operational sense — the buyers already know the operation inside and out. The financial mechanism typically involves installment payments structured over time, since most employees don't have cash on hand to buy a business outright. Documenting the terms in advance prevents disputes.

3. Sale to a third party A third-party sale requires a credible business valuation, proper timing (not a distressed sale), and preparation to make the business attractive to outside buyers. This path usually delivers the highest price but requires the most lead time — typically three to five years.

Whichever path an owner chooses, it must be documented in writing. An unwritten intention is legally worthless. For businesses with multiple owners, that documentation starts with one specific agreement.

Buy-Sell Agreements: The Cornerstone of Business Succession

For any business with more than one owner, a buy-sell agreement isn't optional — it's the document that prevents co-owners from accidentally ending up in business with a deceased partner's divorcing spouse or unknown heirs.

A buy-sell agreement pre-establishes:

- Who can purchase a departing owner's interest

- At what price — using a fixed price, formula, or third-party appraisal

- Under what triggering events — death, disability, retirement, divorce, or bankruptcy

Deloitte identifies two primary structures:

- Cross-purchase agreement: Co-owners buy the departing owner's interest directly. This increases the surviving owners' tax basis in the business — a significant advantage when the business is eventually sold.

- Entity redemption agreement: The business itself buys back the interest. This is simpler to administer with multiple owners but generally does not provide the same basis step-up.

One important recent development: the Supreme Court's 2024 ruling in Connelly v. United States held that life insurance proceeds used to fund a corporate redemption are included in the corporation's value for estate tax purposes — and that the redemption obligation does not offset that value. Business owners with entity redemption structures should review their agreements with an advisor in light of this ruling.

Life insurance is the most common funding mechanism for buy-sell agreements precisely because it delivers the needed capital at the exact moment it's needed — without forcing a fire sale. MassMutual's 2022 Business Owner Perspectives Study found that only 32% of business owners had a buy-sell agreement in place at all, and among those who did, 46% had funded it with life insurance.

Tax Strategies to Protect Your Business and Minimize Estate Taxes

Business interests are typically illiquid and concentrated — which creates a specific estate tax problem. An heir can't sell 20% of a family business to pay a tax bill the way they could sell publicly traded stock. Without planning, the only option is often a distressed sale of the whole business.

Per the Congressional Research Service, the federal estate tax rate on the taxable portion of an estate is 40% above the exemption threshold. The IRS confirms the 2025 exemption stands at $13,990,000 per person, rising to $15,000,000 in 2026 following the One Big Beautiful Bill signed July 4, 2025. While this reduces near-term exposure for many owners, business values can grow quickly — which is why planning early, even before hitting exemption thresholds, matters.

Gifting Strategies and Valuation Discounts

Annual gifting allows owners to transfer ownership stakes over time without triggering gift or estate tax. The 2025 and 2026 annual gift tax exclusion is $19,000 per recipient.

When business interests are transferred through entities like Family Limited Partnerships (FLPs) or LLCs, valuation discounts can reduce the taxable value below fair market value. The IRS recognizes two primary discount types:

- Lack-of-control discount — minority interests have less decision-making power

- Lack-of-marketability discount (DLOM) — interests in private businesses can't be easily sold

These discounts require qualified appraisals and must be structured carefully to withstand IRS scrutiny. Trusts offer a complementary layer of protection — and in some cases, can shift appreciating business assets out of the taxable estate entirely.

Advanced Trust Strategies

Three irrevocable trust structures are particularly useful for business owners:

Grantor Retained Annuity Trust (GRAT): The owner transfers assets into the trust while retaining annuity payments for a fixed term. Any appreciation above the IRS hurdle rate passes to heirs with minimal or no gift tax. This works especially well for business interests expected to grow.

Spousal Lifetime Access Trust (SLAT): One spouse creates an irrevocable trust for the other, removing assets from the taxable estate while allowing the beneficiary spouse to receive distributions. Caution: "reciprocal" SLATs between spouses can trigger IRS scrutiny and potential estate inclusion — professional structuring is essential.

Irrevocable Life Insurance Trust (ILIT): Addresses the liquidity problem directly. When a life insurance policy is owned inside an ILIT, the death benefit is excluded from the taxable estate under IRC Section 2042. The estate receives cash to pay taxes without selling business assets — but requires careful setup and ongoing administration, including annual Crummey notices, to remain effective.

None of these strategies work in isolation. Each requires legal, tax, insurance, and financial planning to align — a gap in any one area can unravel the others. Barking Sands Capital's InteProcess™ coordinates that work across disciplines, so the pieces hold together when it counts.

The Role of Life Insurance in Small Business Estate Planning

Life insurance serves two distinct functions for business owners, and conflating them leads to under-coverage on both counts.

Function 1: Income Replacement

When an owner dies, the business paycheck stops. A surviving spouse who was not active in the business may receive nothing from ongoing operations unless a formal mechanism is in place — a dividend policy, deferred compensation arrangement, or life insurance proceeds earmarked for income replacement.

Without this, a family that relied on the owner's salary faces a simultaneous loss of income and a potentially illiquid estate.

Function 2: Buy-Sell Funding

Life insurance provides the exact capital needed to execute a buyout at the moment it's triggered, without forcing remaining owners to liquidate assets, take on debt, or bring unwanted parties into the business.

Here's what that looks like in practice: two equal partners own a business worth $3 million. One dies unexpectedly. The surviving partner needs $1.5 million to buy out the deceased partner's estate. Without life insurance funding, the options are grim — take on significant debt, sell a portion of the business, or end up co-owning the company with the deceased partner's heirs. None of that was the intent.

Coverage needs change as the business grows. A policy purchased when the business was worth $500,000 is inadequate when the business reaches $2 million. Life insurance coverage should be reviewed alongside business valuations on a regular cycle — not left static from the year the policy was first purchased. Barking Sands Capital holds life insurance licenses in both Michigan and Minnesota, which allows the firm to integrate insurance review directly into its ongoing planning process rather than treating it as a separate engagement.

Common Estate Planning Mistakes Small Business Owners Make

Failing to Create or Update the Plan

The most critical mistake is having no plan — or having one that's years out of date. An outdated buy-sell agreement with a fixed price set a decade ago may massively undervalue the business at the triggering event (death, disability, or departure), leaving surviving partners or heirs in a dispute over a number that no longer reflects reality. Fixed-price agreements become stale quickly; formula-based or appraisal-driven valuation methods reduce this risk significantly.

Commingling Personal and Business Assets

When personal and business finances aren't clearly separated, courts can "pierce the corporate veil," holding business owners personally liable for business debts or exposing business assets to personal creditors. Cornell Law's Wex database confirms that intermingling personal and corporate assets is one of the primary grounds courts use to disregard limited liability protection.

Proper entity structure (LLC or corporation) combined with disciplined financial separation keeps those protections intact. A coordinated advisory team that reviews both the legal structure and financial records together catches these gaps far more reliably than working with a single advisor who only sees part of the picture.

Overlooking Digital Assets and Intellectual Property

Business websites, proprietary software, client databases, social media accounts, and online revenue streams are real assets — and they're routinely absent from estate plans. The Revised Uniform Fiduciary Access to Digital Assets Act (RUFADAA), enacted in most states, governs what fiduciaries can access after an owner's death or incapacity, but access isn't guaranteed without the right provisions in place.

Every business owner should:

- Inventory all digital assets: domains, software licenses, SaaS subscriptions, and online accounts

- Document access credentials in a secure, fiduciary-accessible location

- Include specific transfer instructions in the estate plan for each material digital asset

- Review platform terms of service — some accounts cannot be transferred at all, which makes pre-death planning essential

Each of these mistakes compounds the others. A plan that's current, legally clean, and digitally complete is the foundation everything else builds on.

Frequently Asked Questions

How many small business owners have a succession plan?

The numbers are consistently low. Gallup's 2025 survey found that roughly half of U.S. small business owners either plan to close or have no plan at all. PwC found only 34% of family businesses had a robust, documented succession plan.

What are common mistakes to avoid in estate planning?

The three most damaging: (1) failing to create a plan — or never updating it after major changes; (2) not separating personal and business assets, which exposes both to the other's creditors; and (3) neglecting buy-sell agreements or successor designations, leaving ownership transfer to chance when a triggering event occurs.

How do you keep an operating business out of the owner's estate?

Transferring business interests into irrevocable trust structures — such as SLATs, GRATs, or Intentionally Defective Grantor Trusts (IDGTs) — or gifting ownership shares over time using the annual exclusion can remove business value from the taxable estate. These strategies require coordinated legal, tax, and financial planning to execute correctly.

What is the 5x5 rule in estate planning?

The 5x5 rule refers to a trust provision under IRC Sections 2041 and 2514 that allows a beneficiary to withdraw the greater of $5,000 or 5% of trust assets per year without that lapse being treated as a taxable transfer. It's commonly used to give beneficiaries modest access while preserving the trust's estate tax benefits.

When should a small business owner start estate planning?

At formation — the business entity type directly affects which planning tools are available. At a minimum, estate planning should be in place before the business grows significantly in value, because transferring interests is far more tax-efficient when the business is worth less.

Do I need separate estate plans for my personal and business assets?

A single comprehensive plan can cover both, but it must specifically address business interests, ownership transfer mechanisms, and succession alongside personal asset distribution. The two sides affect each other in ways no single advisor sees in isolation — which is why Barking Sands Capital's InteProcess™ coordinates legal, tax, and financial planning as one integrated strategy.