The short answer: it generally doesn't. The IRS draws a hard line based on one question — who benefits from the policy? When the business itself stands to collect, deductibility is off the table under IRC Section 264(a)(1). But the full picture is more nuanced. Specific exceptions exist, meaningful tax advantages remain available even without premium deductibility, and your business structure changes the equation in ways that catch many owners off guard.

This article covers when premiums can be deducted, when they cannot, the tax advantages that apply regardless, and how entity type affects everything.

Key Takeaways

- Life insurance premiums are generally not deductible when the business is the direct or indirect beneficiary (IRC Section 264)

- Exceptions exist for group term life coverage, Section 162 executive bonus plans, and qualifying compensation arrangements

- Key person insurance and buy-sell policies are rarely deductible — even when they serve a clear business purpose

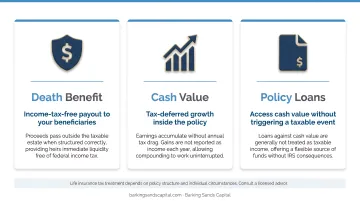

- Life insurance still delivers tax-free death benefits, tax-deferred cash value growth, and tax-free policy loans beyond any deduction question

- Your business entity type (sole proprietor, S corp, C corp) materially affects how premiums are treated

When Life Insurance Premiums Can Be Deductible

The core principle is straightforward: when a policy is structured to benefit an employee or their family — not the business — premiums may qualify as a deductible business expense. Two arrangements stand out.

Employer-Paid Group Term Life Insurance

Under IRC Section 79, businesses can deduct premiums paid for group term life insurance provided to employees, subject to one critical rule: the business cannot be the policy beneficiary.

For employees, the first $50,000 of coverage is excluded from gross income entirely. Coverage above that threshold doesn't disqualify the deduction, but the excess value becomes imputed income to the employee. That amount is calculated using IRS Table I rates from Publication 15-B and must be reported on Form W-2 in boxes 1, 3, 5, and 12 (code C).

Key requirements for the employer deduction:

- The employer must not be named as the beneficiary

- The plan must qualify as group-term coverage under applicable law

- Premiums must meet the ordinary and necessary business expense test under IRC Section 162

The $50,000 threshold is an employee income exclusion — not a cap on what the employer can deduct. The employer deduction is governed by IRC Section 162, not by Section 79 directly.

Section 162 Executive Bonus Plans

A Section 162 bonus plan (sometimes called an executive bonus plan) uses a straightforward structure: the business pays the life insurance premium as a cash bonus directly to a key employee or owner. The employee owns the policy and names their own beneficiary.

The business then deducts the premium as compensation under IRC Section 162(a), which allows deductions for reasonable compensation paid for services rendered.

Here's the trade-off: the employee must report the bonus amount as taxable income under IRC Section 61(a). That makes this arrangement tax-neutral for the employee — they receive value and pay tax on it — but it creates a legitimate, above-the-line deduction for the business.

Why do businesses still use it? Because the employee gains:

- A personally owned life insurance policy with death benefit protection

- Tax-deferred cash value accumulation inside a permanent policy

- Portability — the policy stays with them if they leave

The arrangement also avoids Section 264 disallowance because the employee — not the business — is the policy owner and beneficiary.

For business owners evaluating whether this structure fits, Barking Sands Capital's InteProcess™ coordinates tax, insurance, and financial planning in a single review — so the compensation structure is properly documented and the bonus is correctly reported on the employee's W-2.

When Life Insurance Premiums Are NOT Tax Deductible

IRC Section 264(a)(1) is unambiguous: no deduction is allowed for life insurance premiums when the taxpayer is "directly or indirectly a beneficiary under the policy." Treasury Regulation 1.264-1 reinforces this, specifically applying it to policies covering officers, employees, or financially interested persons when the business benefits.

Three common scenarios hit this wall.

Key Person Insurance

Key person insurance — where the business buys a policy on a critical owner or employee and names itself as beneficiary — is not deductible. The legitimate business purpose (protecting against the financial loss of a key contributor) doesn't matter for tax purposes. Because the business collects the proceeds, Section 264 disallows the deduction outright.

Businesses holding employer-owned life insurance also carry compliance obligations under IRC Section 101(j):

- Obtain written notice and consent from the insured employee before the policy is issued

- Preserve income-tax-free treatment of death benefit proceeds by meeting these requirements at issuance

- File Form 8925 annually to report employer-owned life insurance contracts

Buy-Sell Agreement Policies

Life insurance used to fund a buy-sell agreement faces the same problem. Whether structured as an entity redemption (the business buys back shares) or a cross-purchase (surviving partners buy the departing owner's interest), the business or surviving partners are the beneficiaries. The premiums are non-deductible — regardless of how sound the underlying succession strategy is.

Owner's Personal Life Insurance Paid by the Business

If a business pays premiums on an owner's personal life insurance policy — where the owner's family is the beneficiary — the IRS treats this as a personal expense regardless of how it's recorded in the books. It's not a deductible business expense, and treating it as one invites audit scrutiny.

Tax Advantages That Still Apply Without Premium Deductibility

Tax law intentionally trades premium deductibility for significant back-end advantages. No deduction on the way in — but meaningful tax benefits on the way out, across three distinct areas.

Tax-Free Death Benefit

Under IRC Section 101(a)(1), death benefit proceeds paid by reason of an insured's death are excluded from gross income — whether received by an individual beneficiary or a corporation. This applies to both term and permanent policies.

Two exceptions are worth knowing:

- Transfer-for-value rule (Section 101(a)(2)): If a policy is sold or transferred for valuable consideration, the income exclusion is limited to what the transferee paid plus subsequent premiums. Certain transfers — to the insured, a business partner, or a partnership/corporation in which the insured has an interest — are exempt from this rule.

- Employer-owned life insurance (Section 101(j)): Corporate death benefits lose their tax-free status if the notice and consent requirements weren't met before the policy was issued.

Tax-Deferred Cash Value Growth

Permanent life insurance policies that qualify under IRC Section 7702 accumulate cash value on a tax-deferred basis. The growth inside the policy is not a taxable event. Tax applies only if the policy is surrendered for more than its cost basis — at that point, the gain is included in ordinary income under the rules in IRS Publication 525.

This makes permanent life insurance a legitimate tax-deferred accumulation vehicle, particularly for business owners who have maxed out traditional retirement account contributions.

Tax-Free Policy Loans

Policyholders can borrow against cash value without triggering a taxable event — with one critical exception. If the policy is classified as a Modified Endowment Contract (MEC) under IRC Section 7702A, loans and withdrawals are treated as taxable distributions (subject to ordinary income tax and a 10% penalty before age 59½ under IRC Section 72(v)).

A policy becomes a MEC when premiums paid in the first seven contract years exceed the 7-pay test threshold. A few additional points to keep in mind:

- Staying under the 7-pay threshold — especially in early policy years — preserves tax-free loan flexibility

- Policy loans reduce the death benefit dollar-for-dollar

- A lapsed policy with an outstanding loan can trigger taxable income even on a non-MEC contract

How Business Structure Affects Life Insurance Tax Treatment

Your business structure determines which IRS rules apply to life insurance premiums — and the outcomes vary significantly by entity type.

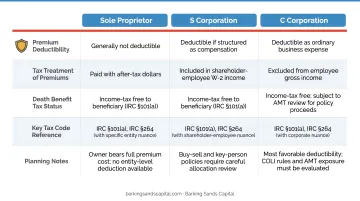

Sole Proprietors

Sole proprietors cannot deduct life insurance premiums on Schedule C. The IRS treats these as personal expenses regardless of business intent. There is no self-employed life insurance deduction analogous to the self-employed health insurance deduction available under Form 7206 — IRS Publication 502 explicitly excludes life insurance from deductible medical expenses.

S Corporations

S corporations carry a specific complication under IRC Section 1372: the S corp is treated as a partnership for fringe benefit purposes, meaning 2% or greater shareholders are treated like partners, not employees, for many fringe benefits.

For these shareholder-employees:

- Life insurance premiums may be deductible by the S corp as compensation

- The premium must be added to the shareholder's W-2 taxable wages

- The shareholder gets no net tax advantage — the deduction and income inclusion offset each other

Under Rev. Rul. 2008-42, premiums paid by an S corp on employer-owned life insurance do not reduce the Accumulated Adjustments Account (AAA). Tax-exempt death benefits go to the Other Adjustments Account (OAA) instead — a distinction that matters for shareholder distributions.

C Corporations

C corporations have the most flexibility of any entity type. Key rules include:

- Premiums for employee group life coverage are deductible as compensation or employee benefits under IRC Section 162

- Properly structured Section 162 executive bonus plans are also deductible

- Corporate-owned life insurance (COLI) death benefits are generally received income-tax-free under Section 101(a)(1), subject to Section 101(j) compliance requirements

- The premiums on COLI policies are not deductible, even though the death benefit is tax-free

This combination — non-deductible premiums with tax-free death benefits — is a core planning strategy for C corporations funding buy-sell agreements or key-person coverage.

Common Mistakes Business Owners Make

A few errors come up repeatedly — and each one carries real cost.

Key person or buy-sell premiums claimed as business expenses. Many owners incorrectly list these on their business returns. Because the business is the beneficiary, Section 264 disallows the deduction — and that triggers IRS scrutiny, amended returns, and potential penalties.

Premiums paid without proper W-2 reporting. A Section 162 plan only generates a legitimate deduction when the premium flows through the employee's taxable compensation and appears on their W-2. Paying the insurer directly without that step breaks the structure and can disqualify the deduction entirely.

Assuming all business insurance follows the same rules. Owners often apply the logic of property and casualty deductibility to life insurance. The rules are fundamentally different, and mixing them up is a common source of error.

The underlying problem in all three cases is treating insurance, tax, and financial planning as separate decisions. When a business purchases or restructures a policy without coordinating the tax implications, mistakes are almost inevitable.

This is exactly the kind of overlap that integrated planning is designed to prevent. Barking Sands Capital's InteProcess™ coordinates insurance, tax, legal, and financial planning as a single team — so a policy decision in one area doesn't quietly create a problem in another.

Frequently Asked Questions

Can I claim life insurance as a tax deduction?

For most individuals and business owners, life insurance premiums are not tax deductible. Limited exceptions apply when a business pays premiums as deductible compensation — such as group term life coverage for employees or a properly structured Section 162 executive bonus plan.

Is key person life insurance tax deductible for a business?

No. Because the business is the beneficiary, IRC Section 264(a)(1) disallows the deduction. However, the death benefit proceeds received by the business are generally income-tax-free under IRC Section 101(a)(1), provided Section 101(j) notice and consent requirements were met.

Can an S corporation owner deduct life insurance premiums?

A 2%-or-greater S corp shareholder may have premiums treated as deductible compensation — but the same premium amount must be included in the shareholder's W-2 taxable income. This creates an offset, not a true deduction.

Is the life insurance death benefit taxable to my business?

For employer-owned policies issued after August 17, 2006, the income-tax exclusion under IRC Section 101(a)(1) applies only if the employer met the notice, consent, and reporting requirements under IRC Section 101(j) before the policy was issued.

What is a Section 162 executive bonus plan and is it tax deductible?

A Section 162 bonus plan allows a business to pay life insurance premiums as a taxable bonus to a key employee who owns the policy. The business deducts the payment as compensation under IRC Section 162; the employee reports it as ordinary income.

Can a sole proprietor deduct life insurance as a business expense on Schedule C?

No. The IRS treats life insurance premiums as personal expenses for sole proprietors — unlike self-employed health insurance, there is no equivalent deduction for life insurance premiums on Schedule C.