Many people approaching 65 feel overwhelmed. The mail starts arriving months early. The decisions feel permanent. And the cost of getting it wrong isn't abstract — a missed enrollment window can mean permanent premium penalties that compound every year you're enrolled.

This guide cuts through the noise. Whether you're approaching 65 in good health, still working, or trying to coordinate Medicare with a broader retirement income plan, here's what you actually need to know.

Key Takeaways

- Medicare has four parts (A, B, C, D), and how they interact determines every enrollment decision you'll make

- Most people have a 7-month Initial Enrollment Period centered on their 65th birthday; missing it triggers lifetime penalties

- Two main coverage paths exist: Original Medicare with a Medigap supplement, or Medicare Advantage; the right choice depends on your health needs and budget

- Active employer coverage (20+ employees) may allow penalty-free delay — COBRA does not qualify

- Medicare doesn't cover dental, vision, hearing, or long-term care, so separate coverage planning is essential

What Is Medicare? The Four Parts Explained

Medicare is built around four distinct parts, each handling a different slice of your healthcare costs. The official Medicare.gov breakdown describes them clearly, but here's the practical version:

| Part | What It Covers |

|---|---|

| Part A | Inpatient hospital care, skilled nursing facility care, hospice, home health care |

| Part B | Doctor visits, outpatient services, preventive care, durable medical equipment |

| Part C | Medicare Advantage — private plans bundling A + B + usually D |

| Part D | Prescription drug coverage |

Parts A and B together form "Original Medicare." Most people qualify for premium-free Part A if they or a spouse paid Medicare taxes for at least 10 years. Part B carries a standard monthly premium of $202.90 in 2026.

What Medicare Doesn't Cover

This is where many people get surprised. Original Medicare does not cover:

- Routine dental care or dentures

- Routine vision exams or eyeglasses

- Hearing aids or hearing exams for fitting

- Non-medical long-term care (custodial care)

These gaps can add up quickly in retirement. Most people address them through a Medigap policy, Medicare Advantage extras, or standalone plans — and choosing the right option depends on your health needs and budget.

When and How to Enroll in Medicare at 65

The Initial Enrollment Period

Your Initial Enrollment Period (IEP) is a 7-month window:

- Starts 3 months before your birthday month

- Includes your birthday month

- Ends 3 months after your birthday month

Enrolling in the 3 months before your birthday month means coverage starts the first of your birthday month. Enrolling during or after your birthday month delays coverage by a month. Enrolling early avoids that delay entirely — your coverage simply starts on time.

If you're already receiving Social Security benefits before 65, Medicare typically enrolls you in Parts A and B automatically.

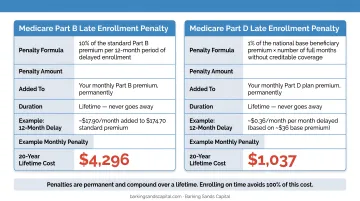

Late Enrollment Penalties — These Are Permanent

Miss your IEP without a qualifying reason, and the penalties stack up for life:

- Part B: 10% added to your premium for each full 12-month period you went without coverage. At $202.90/month in 2026, even a one-year gap adds roughly $20/month — permanently.

- Part D: 1% of the national base beneficiary premium ($38.99 in 2026) for every month without creditable drug coverage. That's about $0.39/month per uncovered month, compounding for as long as you're enrolled.

Neither penalty is capped. Both are calculated and added to your premium indefinitely.

The General Enrollment Period (Fallback Option)

If you miss your IEP, you can enroll during the General Enrollment Period (January 1 – March 31) each year. Coverage starts the month after you sign up. This creates a potential coverage gap and doesn't eliminate late penalties.

How to Actually Enroll

Once you're ready to sign up, you have three options. The fastest is online at SSA.gov, taking 10–15 minutes. You can also call the Social Security Administration directly or visit a local SSA office in person.

Choosing Your Medicare Coverage Path

This is the decision most people agonize over — and for good reason. The two paths look very different on paper, and that gap widens when a serious health episode occurs.

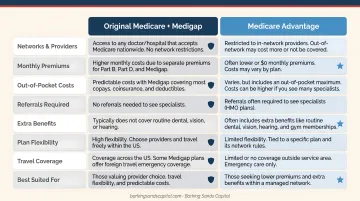

Path 1: Original Medicare (Parts A + B) + a standalone Part D drug plan + a Medigap/Medicare Supplement policy

Path 2: Medicare Advantage (Part C), which bundles A, B, and usually D through a private insurer

Medicare Advantage enrollment reached approximately 35 million beneficiaries — about 55% of eligible Medicare enrollees — as of February 2026, so both paths are mainstream choices with real tradeoffs.

Medigap / Medicare Supplement

Medigap policies are sold by private insurers and pay after Medicare, picking up your share of costs like copays, coinsurance, and deductibles. Key advantages include:

- Access to any provider nationwide that accepts Medicare (no networks)

- Predictable costs, particularly valuable if you have chronic conditions or travel frequently

- Standardized plan types (Plan G is the most comprehensive for new enrollees in most states)

Medigap Plan G averaged approximately $164/month in 2023, with significant variation by state. Timing matters here more than most people realize.

Your Medigap Open Enrollment Period is a 6-month window that starts when you're both 65 or older and enrolled in Part B. During this window, insurers cannot deny coverage or charge higher premiums based on health conditions. After it closes, medical underwriting applies in most states. A pre-existing condition could make you uninsurable or significantly increase your premium.

Medicare Advantage (Part C)

Medicare Advantage plans are offered by private insurers approved by Medicare, and the lower upfront costs draw many enrollees:

- Average premium of approximately $14/month in 2026 across all MA plans

- Often bundles dental, vision, hearing, and drug coverage

- Annual out-of-pocket maximum capped at $9,250 in-network for 2026 (per KFF data)

The tradeoffs are equally real. Most MA plans use HMO or PPO networks; you may need referrals, and your preferred doctor may not be in-network. Annual out-of-pocket exposure during a serious illness can reach into the thousands.

Worth noting: MA plans change their networks, formularies, and benefits every year. A plan that fits your providers and prescriptions at 65 may leave gaps by the time your health needs are more complex.

Curtis Hewitt, a Barking Sands Capital advisor specializing in Medicare Planning and Long-Term Care, helps clients evaluate exactly these tradeoffs. He weighs the cost appeal of Medicare Advantage against the coverage predictability of Medigap based on each person's health situation, provider relationships, and financial picture.

Special Situations: Working Past 65, COBRA, and HSAs

Still Working at 65?

If you're covered under an active employer group health plan at a company with 20 or more employees, you can delay Medicare Part B without penalty. When your employment or employer coverage ends, you have an 8-month Special Enrollment Period (SEP) to enroll in Part B without a late penalty.

Employer size matters. If your employer has fewer than 20 employees, Medicare becomes your primary coverage at 65 — even if you're still working and have employer coverage. The employer plan pays second, meaning every claim is processed as if you have no primary insurance until you enroll.

The COBRA Trap

COBRA is not active employer coverage for Medicare SEP purposes. Medicare.gov states this explicitly: the 8-month SEP window starts when active employment or employer coverage ends, not when COBRA ends. If you leave your job, elect COBRA, and delay Medicare enrollment until COBRA runs out, you'll face late enrollment penalties. Enroll in Medicare when your active employer coverage ends.

HSA Contributions and Medicare

Enrolling in Medicare Part A — even premium-free Part A — ends your ability to contribute to a Health Savings Account (HSA). Three rules to know before you enroll:

- HSA contributions stop on the date your Medicare Part A coverage begins

- Part A can backdate up to 6 months if you apply for Social Security, making contributions during that window excess contributions subject to IRS penalties

- Stop contributions at least 6 months before applying for Medicare or Social Security to avoid a surprise tax bill

These rules catch many people off guard, especially those who delay Social Security. If you're still contributing to an HSA close to 65, review your enrollment timeline carefully before filing any Medicare or Social Security applications.

Common Medicare Mistakes to Avoid

A few missteps here can cost you for life. These are the ones worth knowing before you turn 65:

Assuming COBRA or marketplace coverage extends your enrollment window. Neither qualifies as active employer coverage. Missing the IEP due to this misunderstanding results in permanent Part B and Part D premium penalties, with no appeal process to remove them.

Skipping Part D because you don't take medications. Every uncovered month creates a penalty that applies for life once you eventually enroll. A low-cost Part D plan (some run under $15/month) protects against the penalty and provides coverage the day a new prescription arises.

Set-it-and-forget-it on Medicare Advantage. Plans change every year — networks shrink, formularies shift, premiums rise. Review your coverage each Annual Enrollment Period (October 15 – December 7). Switching back to Original Medicare with a Medigap policy after initial enrollment closes is subject to medical underwriting. Waiting until you're sick to switch may not be an option.

Connecting Medicare to Your Retirement Financial Plan

Medicare is not free, and the monthly costs add up quickly. A representative monthly cost picture for 2026:

| Coverage Component | 2026 Monthly Cost |

|---|---|

| Part B premium (standard) | $202.90 |

| Part D standalone plan (average) | ~$34.50 |

| Medigap Plan G (average) | ~$164.00 |

| Original Medicare + Medigap + Part D | ~$401/month |

| Medicare Advantage (average premium) | ~$14.00 |

| Medicare Advantage path | ~$217/month |

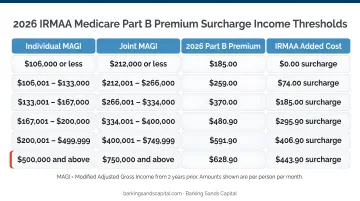

IRMAA: When Your Income Raises Your Premium

Higher-income earners face additional surcharges through IRMAA (Income-Related Monthly Adjustment Amount), applied to both Part B and Part D. The 2026 thresholds use your 2024 tax-year income:

| 2024 Individual MAGI | 2026 Part B Premium |

|---|---|

| ≤ $109,000 | $202.90 |

| $109,001–$137,000 | $284.10 |

| $137,001–$171,000 | $405.80 |

| $171,001–$205,000 | $527.50 |

| $205,001–$499,999 | $649.20 |

| ≥ $500,000 | $689.90 |

A Roth conversion or asset sale in the wrong year can push you into a higher IRMAA bracket two years later. That exposure ties Medicare planning directly to when you retire, when you claim Social Security, and how you sequence withdrawals from retirement accounts.

Barking Sands Capital's advisors, including Curtis Hewitt who specializes in Medicare Planning and Long-Term Care, integrate Medicare costs and IRMAA exposure into broader retirement income strategies. The firm's proprietary InteProcess™ coordinates these decisions alongside tax planning, Social Security timing, and account drawdown — treating Medicare as one piece of a connected financial plan, not a separate checkbox.

Frequently Asked Questions

What should I do about Medicare when I turn 65?

Most people should enroll during their 7-month Initial Enrollment Period centered on their birthday month. Assess whether active employer coverage at a company with 20+ employees allows a delay, and decide between Original Medicare plus Medigap or a Medicare Advantage plan. Enrolling before your birthday month avoids coverage gaps and penalties.

What is the biggest mistake seniors make when enrolling in Medicare?

Missing the Initial Enrollment Period — most often by assuming COBRA or marketplace coverage extends the enrollment window. It does not. The resulting Part B and Part D late penalties are permanent and add to your premium for as long as you're enrolled in Medicare.

Can I delay Medicare if I'm still working at 65?

Yes, if you're covered under active employer group health coverage at a company with 20 or more employees. You'll have an 8-month Special Enrollment Period when that coverage ends. COBRA does not count, and if your employer has fewer than 20 employees, Medicare becomes primary at 65 regardless.

What's the difference between Medicare Advantage and Medicare Supplement (Medigap)?

Medicare Advantage replaces Original Medicare through a private insurer — often with lower premiums but network restrictions, variable out-of-pocket costs, and bundled dental, vision, and drug coverage. Medigap supplements Original Medicare by covering your cost-sharing, giving you access to any Medicare-accepting provider nationwide with no network limitations.

Does heart failure qualify for Medicare before 65?

Heart failure alone does not qualify someone for Medicare before 65. Early eligibility is limited to those receiving SSDI for 24 months, those with End-Stage Renal Disease (ESRD), or those with ALS — but at 65, anyone with heart failure who meets standard age and work-history requirements qualifies like any other beneficiary.

Who is the best person to talk to about Medicare for seniors?

A licensed Medicare planning specialist or independent advisor — one not tied to a single carrier — can compare available plan options, explain enrollment rules, and coordinate Medicare with your retirement income plan. At Barking Sands Capital, Curtis Hewitt specializes in Medicare Planning and Long-Term Care across Minnesota, Michigan, and the Midwest.