Long-term care is the expense most retirement plans never model. According to AARP's LTSS Choices research, 56% of people turning 65 between 2021 and 2025 will need some form of long-term services and supports — and 14% will face out-of-pocket costs exceeding $100,000. Medicare covers almost none of it.

This article covers what insurance agents and financial advisors actually do to address this gap, the funding options they help clients evaluate, how to tell whether a professional is genuinely qualified, and what to bring to your first conversation.

Key Takeaways

- Most Americans will need some form of long-term care, yet Medicare does not cover ongoing custodial care

- Private nursing home care averages $127,750/year — costs that can rapidly deplete retirement savings without a plan

- Financial advisors fit LTC into your retirement income plan; insurance specialists find and structure the right policy

- Hybrid life/LTC policies now outsell standalone policies by a wide margin, offering more flexibility

- The best time to apply is in your mid-50s to early 60s, before health changes narrow your options

Why Long-Term Care Is One of the Biggest Risks to Your Retirement Plan

What "Long-Term Care" Actually Means

Long-term care is not acute medical treatment. It's help with the activities of daily living — bathing, dressing, and eating — that a person can no longer perform independently due to aging, chronic illness, or cognitive decline. Care can be delivered at home by a paid aide, through adult day programs, in an assisted living facility, or in a skilled nursing home.

The distinction matters because Medicare is designed for medical treatment, not personal care. Medicare only covers skilled nursing facility stays for up to 100 days per benefit period — and only when a prior qualifying hospital stay of at least three consecutive days has occurred.

After day 20, a daily coinsurance of $217 applies. After day 100, the individual pays everything.

Medicaid does cover long-term care — but only after most assets are depleted. Most states cap countable assets at roughly $2,000 for an individual before eligibility kicks in. For many families, qualifying for Medicaid means spending down a lifetime of savings first.

The Real Cost Numbers

The 2024 Genworth/CareScout Cost of Care Survey puts national median annual costs at:

- $127,750 for a private nursing home room

- $77,792 for a home health aide (44 hours/week)

- $70,800 for assisted living

From 2023 to 2024, nursing home costs rose 9% and assisted living rose 10% — both outpacing general inflation. This trend has held for more than two decades, making delayed planning increasingly expensive.

The Family Caregiver Assumption

When faced with those cost figures, many households assume a spouse or adult child will step in instead. That assumption carries real financial weight. According to the Bureau of Labor Statistics, 38.2 million Americans — about 14% of the civilian population — currently provide unpaid eldercare.

The personal cost is steep. AARP research shows family caregivers spent an average of $7,242 out of pocket annually — roughly 26% of their income. For those reporting significant work strain, that number climbed to $10,525 per year.

The downstream effects compound quickly:

- About 1 in 5 caregivers reduced their own retirement savings or healthcare spending as a result

- Many reduce work hours or leave jobs entirely, creating their own income gap

Relying entirely on family caregiving transfers one retirement risk onto someone else's financial plan. The risk doesn't disappear — it just changes hands.

What Insurance Agents and Financial Advisors Actually Do for Long-Term Care Planning

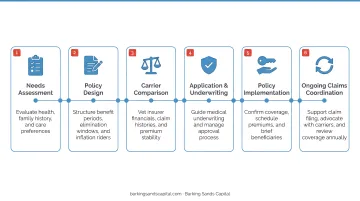

From Product Pitch to Needs Assessment

A good advisor doesn't open the LTC conversation with a policy brochure. They start with questions that most clients have never formally answered:

- Who would actually care for you if you couldn't care for yourself?

- How would your household absorb a $6,000–$10,000/month care expense?

- What does your family health history suggest about your own care risk?

These aren't rhetorical. The answers determine whether insurance makes sense, what benefit level is appropriate, and whether certain products are even worth exploring.

Integrating LTC Into the Full Retirement Plan

A financial advisor's core contribution is modeling — mapping how different care scenarios affect retirement income, investment drawdown rates, tax liability, and the estate. A $90,000/year care cost that runs three years looks very different depending on whether a client draws from a taxable account, a Roth IRA, or a pension.

This broader view is what separates genuine LTC planning from simply purchasing a policy. Coverage that looks adequate on paper can still leave gaps — triggering Medicare surcharges, accelerating asset depletion in a tax-inefficient order, or disrupting a spouse's income.

At Barking Sands Capital, this integration happens through the proprietary InteProcess™ framework — a team-based approach that coordinates legal, insurance, tax, retirement, and financial planning disciplines together. Curtis Hewitt specializes in Long-Term Care and Medicare planning, while CFP® Andrea Cervena and ChFC JB L'Esperance handle retirement income modeling and estate planning, ensuring LTC decisions connect to the full financial picture.

Product-Level Expertise From Insurance Specialists

Insurance agents who specialize in LTC bring a different kind of value: carrier-level knowledge. They know which carriers' underwriting guidelines are most favorable for a client's specific health profile — which matters enormously, since an advisor who doesn't know this landscape might send a client through a full underwriting process only to receive a decline.

LTC specialists also understand the mechanics of policy design:

- Benefit periods — how long the policy will pay (2 years, 5 years, unlimited)

- Inflation protection — how benefits grow over time, critical given LTC cost trends

- Elimination periods — the waiting period before benefits begin (typically 30–90 days)

After the Policy Is In Place

The advisor's role doesn't end at policy issuance. Ongoing responsibilities include:

- Reviewing coverage after major life changes — marriage, divorce, health changes, or significant asset growth

- Coordinating LTC benefits with Medicare to avoid unnecessary surcharges (IRMAA)

- Adjusting retirement income distributions if care is actually needed

- Guiding families through the claims process when benefits are triggered

Long-Term Care Funding Options a Professional Will Help You Evaluate

Standalone Long-Term Care Insurance

Traditional LTC policies pay a daily or monthly benefit once the policyholder meets the trigger — typically inability to perform at least two activities of daily living for 90 days, or a severe cognitive impairment diagnosis.

Advantages:

- Dedicated benefit pool specifically for care expenses

- Inflation protection options to keep pace with rising costs

- Lower initial premiums than hybrid products

Primary drawback: Premiums can increase over time, and if care is never needed, no benefit is paid out — the "use it or lose it" problem.

Premium timing matters. According to 2025 AALTCI data, a 55-year-old male pays roughly $2,200/year for a $165,000 initial benefit pool with 3% annual growth. Wait until 65, and that same coverage costs $3,280/year — a 49% increase.

Hybrid Life/LTC Policies

Hybrid policies combine life insurance with a long-term care rider. The death benefit can be accelerated to pay for care — solving the "use it or lose it" objection. If care is never needed, the death benefit transfers to heirs.

These products now dominate the market. LIMRA data shows hybrid/combo products represented 85% of the LTC insurance market in 2022 — up from a traditional standalone market that sold 732,000 policies in 2001 but only ~27,000 in 2022.

Key characteristics your advisor will walk through:

- Death benefit flexibility — accelerate for care costs or pass to heirs if care is never needed

- Premium stability — most hybrids use single-pay or limited-pay structures, avoiding future rate increases

- 1035 exchange eligibility — an existing life insurance policy can often be converted tax-free into a hybrid LTC policy, funding new coverage without additional out-of-pocket premiums

Annuities With LTC Riders

For clients who don't qualify for traditional or hybrid coverage due to health conditions, annuity-based LTC products offer an alternative path. Some carriers offer deferred annuities with a long-term care rider that multiplies the available benefit pool — certain products provide 2x or 3x the contract value for qualified LTC expenses.

The key difference: annuity-based products typically use simplified or guaranteed-issue underwriting, making them accessible when medical history has closed other doors. Carrier offerings vary significantly, so knowing which products apply to a specific health profile is where specialist knowledge pays off.

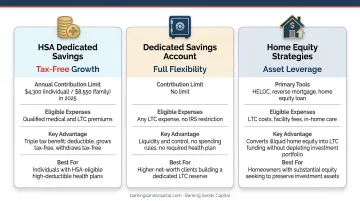

Self-Funding and Alternative Strategies

Not everyone needs or qualifies for insurance. High-net-worth clients sometimes self-fund through:

- Dedicated savings buckets within the investment portfolio, modeled separately from living expenses

- HSAs — distributions for qualified LTC insurance premiums are tax-free, up to IRS age-based limits ($1,800/year for ages 51–60; $4,810 for ages 61–70 in 2025)

- Home equity strategies — HELOCs or reverse mortgages as care-cost backstops

Self-funding requires careful modeling to account for LTC cost inflation and longevity risk. T. Rowe Price's planning analysis uses $80,000–$90,000/year as a 90th-percentile estimate for LTC costs, running those numbers over multiple years with a 5% LTC inflation assumption. Without modeling, it's easy to underestimate the exposure.

How to Know If a Professional Is Qualified to Help With LTC Planning

Not every licensed professional is equally equipped to guide LTC planning decisions. Knowing what to look for — and what questions to ask — can save you from poor coverage choices down the road.

Credentials to Verify

Any professional selling LTC insurance must hold a Life and Health insurance license in your state. Under NAIC model guidelines, they must also complete an initial 8-hour LTC-specific training course and 4 hours of continuing education every 24 months — some states require more.

For financial advisors, relevant designations include:

- CFP® — CFP exam topics explicitly include long-term care insurance and LTC planning

- ChFC — curriculum covers LTC principles alongside broader planning competence

Both credentials cover LTC planning fundamentals, but neither substitutes for hands-on LTC product training. Credentials open the door; experience with actual LTC carriers and claims is what counts.

Questions Worth Asking

Before working with any professional on LTC planning:

- How many clients have you helped obtain LTC coverage in the past two years?

- Have you helped clients navigate the actual claims process?

- Which carriers do you represent — and how many?

An advisor who works with multiple top-rated carriers can compare options and match coverage to your specific health profile — something a single-carrier agent simply can't do. Those answers also reveal how much real-world LTC experience the professional has, not just classroom training.

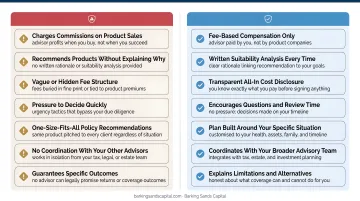

Red Flags vs. Green Flags

| Red Flag | Green Flag |

|---|---|

| Quick conversation, skips health history | Detailed review of health, family history, and finances |

| Only represents one carrier | Works with multiple carriers |

| Recommends a product before assessing needs | Starts with needs assessment, then models options |

| No LTC-specific continuing education | Maintains LTC training requirements |

Starting the Long-Term Care Conversation With Your Advisor

Before a first LTC planning meeting, gather:

- Current assets and retirement income sources (Social Security, pensions, investment accounts)

- Existing life, health, or disability insurance policies

- Family health history — including parents and siblings

- Your own care preferences (home-based care vs. facility-based)

That last point shapes everything. A client committed to aging in place needs a different benefit structure than one open to assisted living.

Those preferences also make timing matter more than most people expect. Most advisors recommend applying in your mid-50s to early 60s — when premiums are still affordable and health underwriting is easier to pass. Waiting significantly narrows both options and affordability. AALTCI data shows declination rates climb from about 14% for applicants in their 50s to nearly 45% for those in their 70s.

For clients in Minnesota or Michigan, Barking Sands Capital coordinates LTC planning alongside Medicare, retirement income, and estate planning in a single process. Curtis Hewitt, the firm's LTC and Medicare specialist, works alongside CFP® and ChFC advisors using the InteProcess™ framework — so your long-term care coverage fits into a retirement plan that accounts for all the moving parts.

Frequently Asked Questions

How much does a financial advisor make from selling a long-term care policy?

Insurance agents and advisors typically earn a commission when a traditional LTC or hybrid policy is issued — usually a percentage of the first-year premium, which varies by carrier and product. Fee-only advisors may charge a planning fee instead of earning commissions. Always ask about compensation structure upfront.

Can you get long-term care insurance with Parkinson's disease?

A Parkinson's diagnosis typically results in a decline for standalone LTC insurance under standard underwriting guidelines. However, some hybrid life/LTC products or annuity-based LTC riders may have more flexible underwriting. Working with a specialist who knows which carriers and products remain accessible is the best path forward.

Does Medicare cover long-term care?

Medicare does not pay for ongoing custodial or personal care — help with bathing, dressing, or eating. It only covers short-term skilled nursing facility stays of up to 100 days per benefit period, and only under specific conditions following a qualifying hospital stay.

When is the best time to buy long-term care insurance?

Most advisors recommend applying in your mid-50s to early 60s, when premiums are more affordable and health underwriting is easier to pass. Waiting until your late 60s or 70s significantly increases costs and the likelihood of being declined entirely.

What is the difference between a standalone LTC policy and a hybrid life/LTC policy?

A standalone policy dedicates all benefits to long-term care with no death benefit — unused benefits are forfeited. A hybrid policy combines life insurance with a long-term care rider, so unused benefits transfer to heirs, addressing the "use it or lose it" concern at the cost of a higher premium.

How does long-term care planning fit into a retirement plan?

LTC is a retirement income risk — a prolonged care need can rapidly deplete savings, disrupt planned distributions, and erode an estate. A complete retirement plan should model LTC cost scenarios alongside Social Security timing, investment drawdown, and other healthcare costs to ensure it holds up even if care is needed.