This guide covers both the foundational moves — retirement accounts, HSAs, FSAs, charitable giving — and the more advanced strategies: Roth conversions, real estate tax structures, income timing, and trust planning. The goal isn't to overwhelm you with every possible option. It's to help you identify which strategies apply to your situation and understand why an integrated approach — one that connects tax planning to investment management, estate planning, and retirement strategy — produces better outcomes than any single tactic in isolation.

Key Takeaways

- Maxing tax-advantaged accounts (401(k), HSA, IRA) is just the foundation — a layered strategy is what actually moves the needle for high earners

- Tax-efficient investing (asset location, tax-loss harvesting, holding periods) cuts annual tax drag without changing portfolio risk

- Advanced strategies — Roth conversions, short-term rental losses, charitable structures, income deferral — require proactive, year-round planning

- Small business owners have additional levers (SEP-IRA, Solo 401(k), Section 199A) that W-2 employees simply don't

- Coordinating tax, investment, and estate planning prevents costly gaps and conflicting strategies

Why High Income Earners Face a Steeper Tax Burden

The Surtax Layer Most People Overlook

The federal income tax brackets are visible and well-understood. What catches many high earners off guard are the surtaxes stacked on top.

According to IRS Rev. Proc. 2024-40, the 2025 brackets for ordinary income reach:

| Filing Status | 35% Bracket | 37% Bracket |

|---|---|---|

| Single | $250,525–$626,350 | Over $626,350 |

| Married Filing Jointly | $501,050–$751,600 | Over $751,600 |

But above those rates sit two surtaxes that apply regardless of bracket:

- Net Investment Income Tax (NIIT): 3.8% on investment income above $200,000 (single) or $250,000 (MFJ) — thresholds that are not inflation-indexed

- Additional Medicare Tax: 0.9% on wages and self-employment income above the same thresholds

Long-term capital gains can reach a 23.8% federal rate when both the 20% LTCG rate and NIIT apply. Factor in state income tax, and the effective rate on investment income approaches ordinary income territory for many high earners.

Phase-Outs and Lost Deductions

Those surtaxes are only part of the problem. Higher income also cuts off access to several common planning tools:

- Traditional IRA deductibility phases out for active plan participants at $79,000–$89,000 (single) and $126,000–$146,000 (MFJ)

- Direct Roth IRA contributions phase out at $150,000–$165,000 (single) and $236,000–$246,000 (MFJ)

- The SALT deduction — now raised to $40,000 for 2025 under H.R.1 — still caps what many high earners can deduct in high-tax states

Two households with similar gross incomes can end up with substantially different tax bills depending on how their income is structured, timed, and positioned.

Foundational Tax Reduction Strategies for High Earners

Maximize Retirement Account Contributions

Contributions to pre-tax retirement accounts reduce adjusted gross income (AGI) dollar-for-dollar — which matters not just for income tax, but for keeping MAGI below NIIT and other surtax thresholds.

2025 contribution limits per IRS Notice 2024-80:

| Account | Standard Limit | Age 50+ Catch-Up | Age 60–63 Catch-Up |

|---|---|---|---|

| 401(k) / 403(b) | $23,500 | $7,500 | $11,250 |

| Traditional / Roth IRA | $7,000 | +$1,000 | — |

| SEP-IRA | $70,000 | — | — |

| Total 401(k) additions (including employer) | $70,000 | — | — |

For high earners above the Roth IRA income limits, the Backdoor Roth strategy remains available: make a nondeductible traditional IRA contribution and convert it to Roth.

If your 401(k) plan allows after-tax contributions beyond the standard employee deferral limit, rolling those after-tax amounts to a Roth IRA — a strategy built on IRS Notice 2014-54 — can substantially expand tax-free savings capacity.

Leverage Health Savings Accounts (HSAs)

If you're enrolled in a qualifying high-deductible health plan (HDHP), an HSA offers three distinct tax advantages in one account: contributions reduce taxable income, growth compounds tax-free, and withdrawals for qualified medical expenses are never taxed.

2025 HSA limits per IRS Rev. Proc. 2024-25:

- Self-only: $4,300 (plus $1,000 catch-up if age 55+)

- Family: $8,550 (plus $1,000 catch-up if age 55+)

- HDHP minimum deductible: $1,650 (self-only) / $3,300 (family)

Those limits are a starting point — the real opportunity is in how you deploy the balance. Invest the HSA rather than spending it annually. At retirement, HSA funds can be withdrawn for any purpose (taxed as ordinary income, like a traditional IRA) or remain tax-free for medical costs. For high earners with predictable healthcare expenses, paying those costs out-of-pocket while the HSA compounds is a legitimate accumulation strategy.

Utilize Employer Benefits and FSAs

These are easy to overlook because the individual amounts seem small. But they reduce AGI using pre-tax dollars — and every dollar of AGI reduction can matter when you're close to a surtax threshold.

2025 limits:

- Health FSA: $3,300 salary reduction; $660 carryover maximum

- Dependent Care FSA: $5,000 per household ($2,500 if married filing separately)

- Commuter benefits (transit/parking): $325/month each

Dependent Care FSAs deliver meaningful savings for high-earning households with young children. At a 37% marginal rate, that $5,000 pre-tax contribution is worth roughly $1,850 in actual tax avoided — every year.

Bunch Charitable Deductions with a Donor-Advised Fund

The 2025 standard deduction is high enough that many high earners who donate annually never exceed it — meaning their charitable giving generates no incremental tax benefit.

The fix: contribution bunching via a Donor-Advised Fund (DAF). Instead of giving $15,000/year for three years, contribute $45,000 to a DAF in one high-income year. You claim the full deduction immediately, then distribute grants to your chosen charities over time at your own pace.

Two additional advantages:

- Donating appreciated assets held over one year (stock, mutual funds) to the DAF avoids capital gains tax entirely while the full fair market value is deductible

- The DAF itself is invested and can grow tax-free between distributions

Tax-Efficient Investing Strategies

Use Asset Location to Minimize Tax Drag

Asset location is the practice of placing investments in the account type that minimizes their tax cost, without changing the overall portfolio.

The basic framework:

- Tax-deferred accounts (IRA, 401(k)): Hold bonds, actively managed funds, REITs — assets that generate ordinary income annually

- Taxable accounts: Hold tax-efficient assets like broad index ETFs and stocks held for long-term capital gains

This reallocation reduces how much of a portfolio's return is lost to annual taxes each year, without altering risk exposure. For a high earner in the top bracket, the difference between holding a bond fund in a taxable account versus a tax-deferred account can represent several percentage points of after-tax return annually.

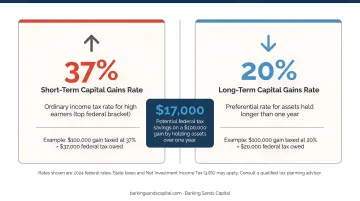

Prioritize Long-Term Capital Gains and Employ Tax-Loss Harvesting

Holding period matters significantly. Short-term gains (assets held one year or less) are taxed as ordinary income — potentially at 37% plus the 3.8% NIIT. Long-term gains use a separate rate schedule:

| Rate | Single (Taxable Income) | MFJ (Taxable Income) |

|---|---|---|

| 0% | Up to $48,350 | Up to $96,700 |

| 15% | $48,351–$533,400 | $96,701–$600,050 |

| 20% | Over $533,400 | Over $600,050 |

For a high earner facing both the 20% LTCG rate and NIIT, the difference between short-term and long-term treatment on a $200,000 gain is roughly $34,000 in federal tax — just from holding a position a few months longer.

Tax-loss harvesting extends this further. Selling positions at a loss offsets realized gains and reduces taxable income, with any excess losses offsetting up to $3,000 of ordinary income annually and carrying forward indefinitely. Per Vanguard's 2024 research using 10,000 simulations, optimally executed tax-loss harvesting can add 0.47%–1.27% annually in after-tax returns.

Two cautions: avoid the wash-sale rule (repurchasing substantially identical securities within 30 days before or after the sale disallows the loss), and focus this strategy on years when RSUs vest, bonuses are paid, or significant rebalancing occurs.

Consider Municipal Bonds for Tax-Free Income

Municipal bonds generate interest exempt from federal income tax, and often state tax when purchased in your home state. For high earners, the tax-equivalent yield (TEY) is the right comparison metric — not the stated rate.

Formula:

TEY = Tax-Exempt Yield ÷ (1 − Marginal Tax Rate)

For a top-bracket investor at 37%: a municipal bond yielding 4.00% has a tax-equivalent yield of 6.35% (4.00% ÷ 0.63). If comparable taxable bonds yield less than 6.35%, the municipal bond wins on an after-tax basis — before factoring in state tax savings.

Morningstar reported in late 2025 that the Morningstar US Municipal Bond Index yield was near 4%, making the TEY math compelling for high earners in top brackets.

Advanced Tax Strategies for High Income Earners

Execute Roth Conversions During Lower-Income Years

A Roth conversion moves pre-tax retirement funds into a Roth IRA, triggering income tax now in exchange for tax-free growth and withdrawals later — and eliminating required minimum distributions (RMDs) on those funds.

The math works best in lower-income years: early retirement, a career transition, a sabbatical, or a year with offsetting deductions. Converting at a 22% or 24% effective rate is very different from converting at 35%.

Key considerations:

- A separate 5-year holding period applies to each conversion for tax-free access to converted amounts

- Conversion income raises MAGI, which affects Medicare IRMAA premiums two years later

- Conversions can push income into higher brackets or across NIIT thresholds

Running the numbers before converting — not after — is essential. At Barking Sands Capital, CFP® Andrea Cervena models Roth conversion scenarios across retirement income, Medicare costs, and long-term estate outcomes as part of the firm's InteProcess™ — so clients see the full multi-year picture before pulling the trigger.

Use Real Estate to Generate Tax-Advantaged Losses

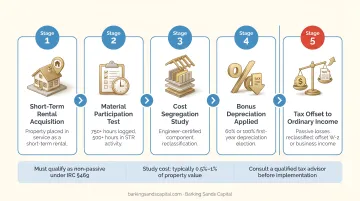

Short-Term Rental (STR) strategy: When the average guest stay is 7 days or fewer, the activity falls outside the passive rental classification under IRS Publication 925. If you also materially participate (one test requires 500+ hours annually), losses become nonpassive — meaning they can offset W-2 or business income directly.

Pairing an STR with a cost segregation study — which reclassifies components of the property into shorter depreciation categories — and the current 40% bonus depreciation (per IRS Pub. 946 for 2025) can generate substantial first-year deductions. For a high earner with significant W-2 income, this can materially reduce taxable income.

The IRS requires genuine material participation, and the activity must make financial sense independent of the tax benefits. Documentation — time logs, rental agreements, communication records — is what separates a defensible position from a disallowed deduction.

For households where the STR strategy applies, Real Estate Professional Status (REPS) goes one step further: if one spouse qualifies (750+ hours in real property trades/businesses, representing more than half their working time), all rental losses — including passive rentals — become nonpassive and can offset any income. For a couple where one spouse manages properties full-time, this can eliminate taxes on six figures of W-2 income in a strong depreciation year.

Leverage Trusts, Strategic Gifting, and Income Timing

Trusts for wealth transfer: The 2025 federal estate tax exemption is $13,990,000 per individual. Even at current exemption levels, irrevocable trusts and Spousal Lifetime Access Trusts (SLATs) serve a dual purpose: transferring wealth outside the taxable estate while potentially shifting income to lower-bracket beneficiaries during the grantor's lifetime.

Annual gifting: The 2025 annual gift tax exclusion is $19,000 per recipient. A married couple can gift $38,000 annually to each child or grandchild without filing a gift tax return. For larger transfers:

- 529 superfunding allows front-loading 5 years of exclusions — up to $95,000 per donor ($190,000 for a couple using gift splitting) — into a 529 plan in a single year, with a Form 709 election

- Gifting appreciated assets transfers the embedded gain to beneficiaries who may face lower capital gains rates

Income timing: In years with unusually high income — RSU cliff vest, large bonus, business sale — the highest-impact moves happen before December 31, not the following April. Year-end levers worth modeling include:

- Deploying an STR loss against ordinary income

- Accelerating charitable deductions into a DAF before year-end

- Deferring stock option exercises or appreciated asset sales into the following tax year to stay below NIIT thresholds or bracket ceilings

Common Tax Planning Mistakes High Earners Make

Most tax planning failures aren't about picking the wrong strategy. They're about timing, integration, and documentation.

Reactive planning is the most expensive mistake. By April, the most powerful levers are already locked: retirement contributions, Roth conversions, income timing, year-end charitable giving. Tax planning is a year-round discipline, not a once-a-year scramble.

Siloed advice creates gaps that cost real money. When an investment advisor, CPA, and estate attorney each work independently, strategies can conflict or miss available deductions. A Roth conversion that looks smart in isolation might inadvertently trigger IRMAA surcharges two years later, or create an estate planning problem.

This is why coordinated planning matters. Barking Sands Capital's InteProcess™ integrates legal, insurance, tax, retirement, and financial planning as a single team, so no strategy is evaluated in a vacuum.

Over-focusing on one strategy while ignoring higher-impact opportunities is common among high earners who feel satisfied after maxing a 401(k). That's a starting point, not a finish line.

Watch out for these compounding mistakes:

- Pursuing STR losses or cost segregation without genuine material participation documentation

- Chasing aggressive strategies in investments that aren't financially sound on their own

- Treating each tax move in isolation rather than stress-testing across retirement, estate, and income plans

Frequently Asked Questions

How can high income earners reduce taxes?

The most effective combination: maximize tax-deferred retirement accounts (401(k), SEP-IRA, HSA), use asset location and tax-loss harvesting to reduce investment tax drag, and time income and capital gains recognition strategically. Real estate structures and charitable giving vehicles add further reduction for more complex situations.

Can I give my kids $100,000 tax-free?

The 2025 annual gift tax exclusion is $19,000 per recipient — so a couple can gift $38,000 per child without filing. For $100,000, you'd use a combination: 529 superfunding allows up to $95,000 per donor (5-year election), or you can apply part of your lifetime exemption. Either way, a Form 709 will likely need to be filed.

What is the best retirement account for high income earners?

A 401(k) or SEP-IRA offers the highest contribution limits and the most immediate AGI reduction. For high earners above Roth income limits, the backdoor Roth strategy allows Roth IRA access regardless of income. Most high earners benefit from a mix — pre-tax contributions now, with some Roth positioning for future flexibility.

When does a Roth conversion make sense for a high income earner?

Roth conversions make the most sense in lower-income years when the conversion tax cost is well below your expected future rate on withdrawals. They're also worth considering to eliminate future RMDs or leave tax-free assets to heirs — but Medicare IRMAA implications require careful modeling.

What additional tax strategies are available to high-income small business owners?

Business owners access tools W-2 employees can't: SEP-IRA or Solo 401(k) contributions up to $70,000, the Section 199A pass-through deduction (below $394,600 MFJ for most), and salary-vs-distribution structuring to reduce self-employment taxes — plus standard deductible business expenses.

Is tax-loss harvesting worth it for high income earners?

Yes — particularly because high earners face both elevated capital gains rates and the NIIT surtax. Harvested losses offset gains dollar-for-dollar, and any unused losses carry forward indefinitely. The strategy is especially valuable in years with large RSU vests, equity sales, or significant portfolio rebalancing events.