Introduction

Most Americans spend decades building wealth—growing businesses, accumulating real estate, funding retirement accounts—without a coordinated plan for what happens to it. The result: taxes erode more than intended, probate delays asset transfers for months or years, and distributions land nowhere near what the owner envisioned.

The stakes are real. With the federal estate tax sitting at 40% on amounts above the exemption threshold, a poorly structured estate can lose a substantial portion of wealth before heirs receive a dollar.

This guide covers the advanced strategies that change that outcome: trust structures like GRATs, ILITs, and QPRTs; strategic gifting programs; business succession tools; and life insurance strategies designed to solve the liquidity problems estates often face.

Whether you're near the federal threshold or well above it, these techniques work best when integrated across legal, tax, insurance, and investment planning. That coordination is what separates a solid estate plan from one that actually executes as intended.

Key Takeaways

- The 2025 federal estate tax exemption is $13,990,000 per individual; the One Big Beautiful Bill Act raises it to $15,000,000 for 2026

- Advanced trusts—GRATs, ILITs, QPRTs, CRTs—permanently remove assets from a taxable estate, transferring wealth tax-free to heirs or charities

- Systematic gifting at $19,000 per recipient (2025) compounds into significant estate reduction across multiple years and recipients

- State-level estate or inheritance taxes apply in 12 states plus DC, often at much lower thresholds than the federal exemption

- Full planning effectiveness requires integrating estate strategies with retirement, insurance, and business succession

What Are Estate and Tax Planning?

Estate planning is the legal and financial process of deciding how assets will be managed, protected, and transferred—during life and at death. It encompasses wills, revocable and irrevocable trusts, powers of attorney, beneficiary designations, and titling decisions.

Tax planning, in this context, means proactively applying legal strategies to reduce estate taxes, gift taxes, generation-skipping transfer (GST) taxes, and the income taxes beneficiaries may face when inheriting assets.

Every estate distribution decision carries tax consequences—and every tax strategy affects how assets ultimately transfer. Treating the two as separate disciplines creates predictable gaps:

- A trust structured purely for probate avoidance may miss significant estate tax savings

- A gifting strategy designed to reduce estate size may create unexpected capital gains exposure for heirs

Coordinating both from the start prevents those gaps.

The Federal Estate Tax in 2025 and Beyond

Current Exemption and Rate

Per IRS Form 706 instructions, the 2025 basic exclusion amount is $13,990,000 per individual, with a top estate tax rate of 40%. A married couple can effectively shelter up to $27,980,000 through proper planning.

The One Big Beautiful Bill Act amended IRC Section 2010(c)(3) to increase the exclusion to $15,000,000 for 2026, eliminating the TCJA sunset that would have reduced the exemption to approximately $5,000,000 (indexed). That's a significant reprieve, but future legislation can shift the landscape again — treating today's environment as permanent is a planning risk worth accounting for now.

Portability: Don't Miss the Deadline

Portability allows a surviving spouse to use the deceased spouse's unused exemption (DSUE). To preserve this benefit, the executor must file Form 706 within 9 months of death (or by the end of a valid 6-month extension)—even when no estate tax is owed.

If that window is missed, Rev. Proc. 2022-32 provides late portability relief for estates not otherwise required to file, allowing the election up to 5 years after the date of death.

State-Level Exposure

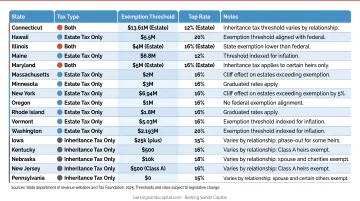

Federal planning alone isn't enough. According to the Tax Foundation's 2025 data, 12 states plus DC levy estate taxes, and 5 states levy inheritance taxes—Maryland has both.

Key examples with low exemption thresholds:

| State | Tax Type | 2025 Exemption |

|---|---|---|

| Oregon | Estate tax | $1,000,000 |

| Massachusetts | Estate tax | $2,000,000 |

| Minnesota | Estate tax | $3,000,000 |

| Illinois | Estate tax | $4,000,000 |

| Maryland | Estate + Inheritance | $5,000,000 / $1,000 |

Clients in Minnesota and Michigan—Barking Sands Capital's core markets—need to account for Minnesota's $3,000,000 estate tax threshold alongside federal planning.

Advanced Trust Strategies to Protect and Transfer Wealth

Grantor Retained Annuity Trust (GRAT)

A GRAT works by transferring appreciated assets into an irrevocable trust. The grantor receives a fixed annuity payment for a set term. If the assets grow faster than the IRS Section 7520 rate—currently 5.0% for June 2026 per Rev. Rul. 2026-11—the excess passes to heirs gift-tax free.

The zeroed-out GRAT sets the annuity payment so that its actuarial value equals the assets transferred, reducing the taxable gift to near zero at funding. Walton v. Commissioner, 115 T.C. 589 (2000) established this structure as IRS-compliant. The catch: if the grantor dies during the trust term, the strategy fails—which makes term length a critical planning variable. Shorter terms reduce mortality risk but require faster asset appreciation to beat the hurdle rate.

Irrevocable Life Insurance Trust (ILIT)

Under IRC Section 2042, life insurance death benefits are included in the taxable estate if the decedent held incidents of ownership over the policy. An ILIT removes the policy from the estate—but with conditions:

- The grantor must not retain incidents of ownership

- Under IRC Section 2035, transfers made within 3 years of death can be pulled back into the estate

- Annual contributions to fund premiums must follow Crummey notice requirements—beneficiaries receive written notice of their right to withdraw contributions, creating a present interest that qualifies for the annual gift tax exclusion

For estates with significant illiquid assets—a family business, farmland, investment real estate—an ILIT provides estate-tax-free liquidity when it's most needed.

Residence and Charitable Giving Strategies

Qualified Personal Residence Trust (QPRT): The homeowner transfers a primary or vacation home into a trust for a fixed term, retaining the right to live there. Under eCFR Section 25.2702-5, the gift tax value is based on the actuarial present value of the remainder interest—typically a fraction of fair market value, creating a meaningful estate tax discount.

The same mortality risk applies as with a GRAT: the grantor must survive the trust term, or the residence is pulled back into the estate.

Charitable Remainder Trust (CRT): Assets transfer to the trust; the grantor (or another named beneficiary) receives an income stream for life or a term of up to 20 years. The remainder passes to a designated charity. Key benefits:

- An immediate partial income tax charitable deduction based on the present value of the charitable remainder

- IRC Section 664(c) generally exempts the CRT from income tax, allowing appreciated assets to be sold inside the trust without immediate capital gains recognition

- Distributions to beneficiaries are taxable (governed by the four-tier ordering rules), but the deferral advantage is substantial for high-appreciation assets

Strategic Gifting and Business Succession Techniques

Annual Exclusion and Lifetime Gifting

Per IRS Form 709 instructions, the 2025 annual gift tax exclusion is $19,000 per recipient. Married couples can split gifts to double the exclusion to $38,000 per recipient without touching the lifetime exemption.

A systematic gifting program across multiple family members compounds over time. Gifting $38,000 annually to five family members removes $190,000 from the taxable estate each year—and removes future appreciation on those assets as well.

The basis trade-off matters when choosing between gifting now or transferring at death:

- Lifetime gifts carry the donor's original cost basis (IRC §1015) — heirs owe capital gains tax when they sell

- Death transfers receive a stepped-up basis to fair market value (IRC §1014), wiping out embedded capital gains entirely

Gifting highly appreciated assets during life generally works better when the estate tax savings outweigh the capital gains cost to heirs—a calculation that depends on asset type, holding period, and the heir's tax bracket.

Generation-Skipping Transfer (GST) Strategies

GST tax applies when assets transfer to grandchildren or others at least 37.5 years younger than the donor—on top of estate or gift taxes, also at a 40% rate. The 2025 GST exemption is $13,990,000 (matching the estate tax exemption).

Dynasty trusts apply this exemption to trusts designed to pass wealth across multiple generations, with assets growing inside the trust structure and bypassing estate tax at each generational transfer. The strategy requires careful drafting and state law selection—some states have eliminated the rule against perpetuities, making multi-generational trust terms possible.

Business Succession Techniques

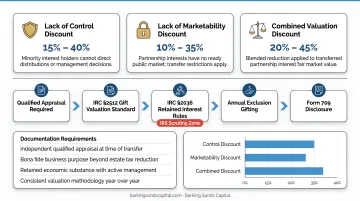

Family Limited Partnerships (FLPs) and Family LLCs transfer business or investment assets into an entity, then allow parents to gift non-voting or limited partner interests to heirs at valuation discounts. Three discounts drive the tax benefit:

- Minority interest discount (recipient holds no control over the entity)

- Lack of marketability discount (interests are illiquid and non-tradeable)

- Combined, these discounts typically reduce the taxable transfer value by 20–40%

IRS examiners scrutinize FLP structures under Section 2036, and courts have denied discounts when entities lack a legitimate business purpose beyond tax savings.

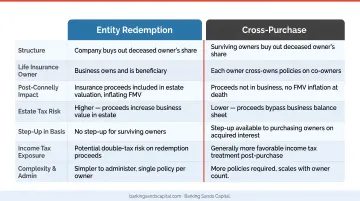

Buy-sell agreements control what happens to a business interest at an owner's death or departure. They establish a valuation mechanism and are typically funded with life insurance to provide liquidity for the buyout. One ruling changed the math here: in Connelly v. United States (2024), the Supreme Court held that life insurance proceeds owned by a company to fund a buy-sell agreement must be included in the business's estate tax valuation—potentially increasing the taxable estate. Business owners with existing buy-sell agreements should review their structures in light of this decision.

Using Life Insurance as an Estate Tax Planning Tool

The Liquidity Problem

Estate taxes are generally due 9 months from the date of death. Estates heavy in illiquid assets—real estate, business interests, farmland—face a difficult choice: sell assets under pressure or pay taxes with funds that weren't set aside. Life insurance held inside an ILIT is the most common solution, providing tax-free cash precisely when needed.

Second-to-Die (Survivorship) Policies

For married couples, the unlimited marital deduction defers estate tax until the surviving spouse's death. A survivorship life insurance policy pays at that second death—when the tax is actually due. This structure typically costs less in premiums than two individual policies and works most efficiently when held inside an ILIT to keep the death benefit out of both estates.

The Wealth Replacement Strategy

When a client transfers appreciated assets to a Charitable Remainder Trust (CRT), two benefits follow: an income tax charitable deduction and increased income yield from selling appreciated assets inside the CRT without triggering immediate capital gains. That extra income can fund premiums on a life insurance policy held inside an ILIT.

The outcome: the charity receives the CRT remainder, and the family receives the ILIT death benefit. Both parties benefit from a single coordinated strategy.

Connelly and the Buy-Sell Warning

In Connelly v. United States (June 6, 2024), the Supreme Court held that company-owned life insurance proceeds used in a redemption agreement increased the corporation's fair market value for estate tax purposes—the contractual obligation to redeem shares did not offset that value. The practical impact: business owners using entity-redemption buy-sell agreements funded with company-owned life insurance may now face higher estate tax valuations than anticipated.

The two main buy-sell structures now carry meaningfully different tax outcomes:

- Entity-redemption agreements (company holds the insurance): proceeds increase the corporation's FMV, raising potential estate tax exposure after Connelly

- Cross-purchase arrangements (owners hold insurance on each other): proceeds go directly to the purchasing owners, bypassing the corporation and avoiding the valuation problem

Business owners should review existing buy-sell structures in light of Connelly with qualified advisors.

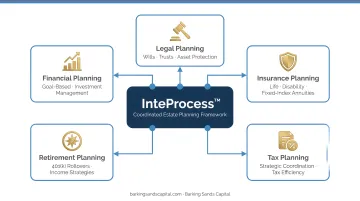

Building a Coordinated Estate and Tax Plan

The most common planning mistake is treating estate planning as a standalone legal task—signing documents and filing them away. The reality is that wills and trusts only work as intended when they're coordinated with:

- Retirement account beneficiary designations (which override trust provisions)

- Life insurance ownership and beneficiary structure

- Investment portfolio titling and asset location

- Business ownership agreements

- Tax planning strategies (Roth conversions, harvesting, charitable giving)

Barking Sands Capital's proprietary InteProcess™ addresses this coordination gap directly. Rather than sending clients to separate attorneys, insurance agents, and CPAs who never speak to each other, the InteProcess™ integrates legal, insurance, tax, retirement, and financial planning into one unified process.

That means a Roth conversion decision, for example, is evaluated for its impact on estate tax exposure, Medicare IRMAA thresholds, and investment positioning at the same time.

When to Review Your Estate Plan

Estate plans require periodic review — life changes faster than most documents do. Any of these events should prompt a reassessment:

- Marriage, divorce, or death of a spouse or beneficiary

- Birth or adoption of a child or grandchild

- Sale of a business or significant asset

- Receiving a large inheritance

- Major change in asset values or estate size

- Moving to a new state (especially one with estate or inheritance taxes)

- Significant tax law changes—like the OBBBA's 2026 exemption increase

Frequently Asked Questions

What is tax and estate planning?

Estate planning is the legal and financial process of managing and transferring assets during life and at death—through wills, trusts, powers of attorney, and beneficiary designations. Tax planning minimizes estate, gift, and income taxes along the way, ensuring more wealth reaches intended beneficiaries rather than being lost to avoidable taxes or administrative costs.

What are the 7 steps in the estate planning process?

The seven core steps are:

- Inventory assets and liabilities

- Define goals and beneficiaries

- Select legal tools—will, trust, powers of attorney

- Designate beneficiaries on accounts and insurance

- Implement tax minimization strategies

- Coordinate with financial and insurance plans

- Schedule regular reviews

What is the 5 and 5 rule in estate planning?

Under IRC Section 2514(e), a trust beneficiary may withdraw the greater of $5,000 or 5% of the trust's value annually without triggering gift tax consequences. This "5 and 5 power" gives beneficiaries limited access to trust funds while preserving the trust's tax advantages.

What is the difference between a revocable and irrevocable trust?

A revocable trust can be changed or dissolved by the grantor at any time—but assets remain in the taxable estate. An irrevocable trust permanently transfers assets out of the estate, making it an effective tax-reduction tool, but one that sacrifices the grantor's direct control over those assets.

When should I start estate and tax planning?

The best time is before you need it—especially before major life events like marriage, business ownership, or significant asset accumulation. With the federal exemption at $13,990,000 in 2025 and rising to $15,000,000 in 2026, acting now provides maximum planning flexibility.

Can life insurance proceeds be subject to estate taxes?

Yes—if the policy owner is the insured, the death benefit is included in the taxable estate under IRC Section 2042. Transferring the policy to an ILIT removes it from the estate, provided the insured survives at least 3 years after the transfer under IRC Section 2035. When structured properly, the ILIT delivers tax-free death benefits directly to heirs.