According to BLS data, nearly 50% of private-sector businesses fail within five years and 65% within ten years. While failure has many causes, the Federal Reserve's 2025 Small Business Credit Survey found that 56% of employer firms struggled to pay operating expenses and 51% cited uneven cash flows as significant financial challenges — problems that proactive financial planning directly addresses.

This guide covers the core pillars every entrepreneur needs: separating finances, budgeting, tax strategy, risk management, retirement planning, and knowing when to bring in professional help. Most business owners are experts in what they do — not in financial planning. Treating financial management as seriously as your business model is what separates those who build lasting wealth from those who don't.

Key Takeaways

- Keeping personal and business finances separate protects your legal standing and simplifies taxes

- A 3–6 month emergency fund for both business and personal expenses cushions income volatility

- Quarterly estimated taxes, smart deductions, and retirement contributions lower your overall tax burden

- Disability, liability, and life insurance protect both your business operations and personal assets

- Fee-only advisors with fiduciary duty give guidance aligned with your interests, not product sales

Separate Your Personal and Business Finances

Mixing personal and business funds is one of the most common — and costly — mistakes entrepreneurs make. It creates accounting confusion, complicates tax filing, and can expose your personal assets to business liabilities.

Why Separation Matters for Tax and Legal Protection

Separate accounts create clean documentation of deductible business expenses, which reduces audit risk and simplifies year-end filing. IRS Publication 583 explicitly instructs business owners to open a dedicated business checking account, keep it separate from personal accounts, and use it exclusively for business purposes.

There's also a legal dimension many entrepreneurs overlook. If you commingle funds — paying personal bills from a business account or depositing business revenue into a personal account — courts can "pierce the corporate veil."

That means a judge can disregard your LLC or corporation and hold you personally liable for business debts or lawsuits. The liability protection you paid to establish disappears.

How to Set Up a Clean Financial Separation

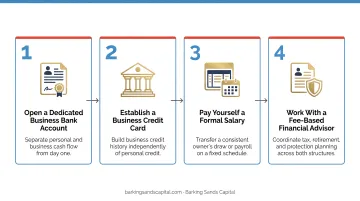

Four steps cover the essentials:

- Open a dedicated business checking account and business credit card — route all business income and expenses exclusively through these accounts

- Pay yourself a defined owner's draw or salary — don't dip into business funds ad hoc

- Use accounting software such as QuickBooks, FreshBooks, or Xero to track business transactions separately and monitor cash flow

- Never write checks payable to cash from your business account (per IRS guidance)

Beyond compliance, clean separation gives you an accurate read on whether your business is genuinely profitable — independent of your personal finances. That picture matters when you're weighing whether to reinvest earnings, bring on staff, or take on debt.

Build a Budget and Manage Cash Flow Effectively

Cash flow problems are among the leading causes of small business failure. A 2019 QuickBooks study found that 61% of small businesses struggle with cash flow, with nearly 32% unable to pay vendors, loans, or employees at some point. Budgeting isn't just bookkeeping — it's survival planning.

Creating a Realistic Business Budget

A solid business budget covers four components:

- Fixed costs: rent, payroll, software subscriptions, loan payments

- Variable costs: marketing, supplies, shipping, contractor fees

- Projected revenue: based on historical data or conservative forecasts

- Profit margin targets: the difference between what you earn and what you spend

Run a parallel personal budget alongside your business budget. Entrepreneurs with irregular income need to plan personal expenses independently so that a slow business month doesn't force an unexpected draw from operating funds.

The 70/20/10 framework allocates 70% of income to expenses, 20% to savings or debt repayment, and 10% to reinvestment or growth. Adjust the ratios during heavy growth periods, but the structure enforces one critical discipline: not spending everything that comes in. That same discipline is what funds your safety net.

Building and Maintaining an Emergency Fund

Standard advice suggests keeping three to six months of expenses in reserve. For entrepreneurs, that means two separate reserves:

- Business emergency fund — 3–6 months of operating costs

- Personal emergency fund — 3–6 months of living expenses

Keep both in a high-yield savings account where they earn interest but remain accessible.

Consider what happened to small businesses during COVID-19: a Federal Reserve study found that only one in five financially healthy firms had enough reserves to sustain two months of revenue loss — and less financially stable firms fared far worse. A contingency fund gives you the runway to adapt when conditions shift, rather than scrambling to stay open.

Tax Planning Strategies for Entrepreneurs

Entrepreneurs face a more complex tax picture than salaried employees. You're responsible for self-employment tax, quarterly estimated payments, and (depending on your structure and staff) payroll taxes, state obligations, and sales tax. The stakes of getting this wrong include penalties, interest, and an unexpectedly large April tax bill.

Understanding Your Tax Obligations

The primary categories most entrepreneurs face:

| Tax Type | Key Detail |

|---|---|

| Self-employment tax | 15.3% (12.4% Social Security + 2.9% Medicare) |

| Social Security wage cap | $176,100 for 2025 |

| Additional Medicare Tax | 0.9% above $200,000 (single) or $250,000 (MFJ) |

| Quarterly estimated payments | Due four times per year; underpayment triggers penalties at 7% annually (compounded daily, 2026 Q2) |

Tax obligations also vary by entity type. A sole proprietor pays self-employment tax on all net earnings. An S-Corp shareholder-employee pays employment taxes only on their reasonable salary, not on profit distributions, which can produce meaningful tax savings at higher income levels.

Strategies to Reduce Your Tax Burden Legally

Track and claim every legitimate deduction:

- Home office (regular and exclusive use required)

- Vehicle mileage — the 2026 IRS standard rate is 72.5 cents per mile

- Equipment and business-related software

- Self-employed health insurance premiums (via Form 7206)

- Professional development that maintains or improves skills

- Retirement contributions

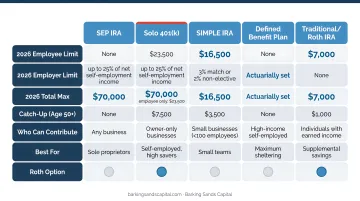

Retirement accounts double as a tax reduction tool. Contributions to a SEP IRA, Solo 401(k), or SIMPLE IRA reduce taxable income in the year you contribute while building long-term wealth. The 2026 IRS limits:

- SEP IRA — up to 25% of compensation, max $72,000

- Solo 401(k) — employee deferral $24,500; total defined contribution limit $72,000

- SIMPLE IRA — employee contributions up to $17,000

Entity structure deserves a yearly review. Electing S-Corp status at a certain income level can reduce self-employment tax exposure. Business conditions shift, and the tax math changes with them — what didn't make sense at $80,000 in net profit may make sense at $150,000.

Protect Your Business: Insurance and Estate Planning

A lawsuit, a disability, or the sudden death of a co-owner doesn't just disrupt operations — it can unravel years of work and leave employees, partners, and family with no clear path forward. For entrepreneurs, these aren't hypothetical scenarios. They're the risks that demand a specific, deliberate response.

Key Insurance Types Every Entrepreneur Needs

The right mix depends on your industry, size, and stage of growth, but these categories apply to most business owners:

- General liability — covers bodily injury, property damage, and basic lawsuit exposure

- Professional liability (E&O) — protects against claims of negligence or errors in your services

- Property insurance — covers equipment, inventory, and physical assets

- Business interruption insurance — replaces lost revenue when operations are disrupted

- Health insurance — critical once you leave employer-sponsored coverage

- Life insurance — protects business partners and family dependents

- Disability insurance — the most underutilized coverage among self-employed individuals

That last category matters more than most owners realize. LIMRA data shows only 18% of consumers carry disability insurance, while BLS data shows employer-sponsored short-term disability access ranges from 31% at small firms to 68% at large ones. Self-employed owners have no employer fallback. If you can't work, there's no income replacement unless you've arranged it yourself.

Estate Planning and Business Continuity

Every entrepreneur with a business partner needs a buy-sell agreement — a formal agreement that specifies what happens to ownership stakes if a partner dies, becomes disabled, retires, or departs. Without one, you could find yourself forced to accept an unwanted heir as a co-owner, or face a costly legal dispute at an already difficult moment. A 2022 MassMutual study found only 32% of business owners had a buy-sell agreement in place.

Beyond the business, a personal estate plan is equally critical. For most entrepreneurs, the business is their largest asset — and it needs to be addressed in any estate strategy, not treated as separate from personal financial planning. At minimum, that plan should include:

- A will that addresses business ownership and disposition

- A durable power of attorney for financial and healthcare decisions

- Up-to-date beneficiary designations on all accounts and policies

Retirement and Investment Planning for Business Owners

Unlike corporate employees with automatic 401(k) enrollment and employer matches, entrepreneurs build their retirement plan entirely from scratch. Pew Research found that only 13% of self-employed workers in single-person firms participated in a retirement plan at their current job, compared to nearly 75% of traditional employees. Starting early — even with modest contributions — closes that gap over time.

Retirement Account Options for the Self-Employed

| Account Type | Best For | 2026 Contribution Limit |

|---|---|---|

| SEP IRA | Simple to set up, minimal admin | Up to $72,000 (25% of compensation) |

| Solo 401(k) | Owner-only businesses, highest flexibility | $72,000 total; $24,500 employee deferral |

| SIMPLE IRA | Businesses with employees | $17,000 employee contributions |

| Cash Balance Plan | High earners accelerating savings | Up to $290,000 annual benefit |

As your business grows, employer-sponsored retirement plans become a recruiting tool as well as a personal savings vehicle. Designing a plan that covers employees while maximizing your own contributions turns a tax strategy into a meaningful business advantage.

Cash-balance plan design in particular requires careful coordination of business income, employee coverage rules, and contribution timing — the kind of integrated work that advisors like those at Barking Sands Capital do for business owner clients.

Build an Investment Portfolio Beyond the Business

Treating your business as your retirement plan is a concentration risk most entrepreneurs underestimate. A business can lose value, face legal issues, or become unsellable. Building a separate investment portfolio protects you when the business underperforms or exit terms fall short of expectations. A well-diversified mix might include:

- Publicly traded stocks and equity funds

- Bonds and fixed income instruments

- Real estate investment trusts (REITs) or direct real estate holdings

- Alternative assets that have no correlation to your industry

Each of these operates independently from your business, giving you financial stability regardless of what happens with the company.

Working with a Fee-Based Financial Advisor

Entrepreneurs need more than investment advice. They need someone who can address tax strategy, retirement planning, insurance gaps, estate planning, and business structure — not as separate conversations, but as a coordinated whole.

Fee-Only vs. Fee-Based: The Distinction That Matters

The terminology here creates real confusion. According to the CFP Board:

- Fee-only advisors are compensated exclusively by clients — no commissions, no product sales

- Fee-based advisors may charge fees and receive sales-related compensation

An independent Registered Investment Advisor (RIA) operating under the SEC's fiduciary standard is legally obligated to act in the client's best interest. That structural alignment matters when you're making high-stakes decisions about entity structure, retirement plan design, and asset protection.

Credentials signal depth. A CFP® (Certified Financial Planner) designation requires 6,000 hours of professional experience, rigorous examination, and ongoing ethics requirements. The ChFC (Chartered Financial Consultant) designation from The American College covers eight required courses spanning the full range of financial planning disciplines — from risk management to estate strategies.

What to Look for in an Advisor for Your Business

When evaluating advisors, prioritize:

- Acts as a fiduciary — legally obligated to put your interests first, not compensated through product commissions

- Has worked with business owners before — tax, retirement, and estate needs differ significantly from W-2 earners

- Coordinates across disciplines rather than treating tax, insurance, and investments as separate conversations

- Discloses compensation clearly upfront, so you always know how they're paid

Barking Sands Capital, an independent RIA with offices in Minnetonka, Minnesota and Troy, Michigan, works with small business owners across the Midwest as a core part of its practice. Their team includes both CFP® and ChFC credential holders, and their proprietary InteProcess™ brings legal, insurance, tax, retirement, and financial planning together as a unified strategy — not a disconnected series of one-off recommendations. For entrepreneurs who need all the pieces working in sync, that kind of coordination is difficult to achieve with single-discipline advisors.

A survey by Equitable and SCORE found that 83% of small business owners consider it important to work with a financial professional — and those who do expect to retire seven years earlier than those who don't.

Frequently Asked Questions

What is financial planning in entrepreneurship?

Financial planning for entrepreneurs is the ongoing process of managing both business and personal finances — including budgeting, tax strategy, risk management, investment, and retirement — to build stability alongside business growth. Unlike salaried employees, entrepreneurs must actively coordinate all of these areas themselves.

What is the 70/20/10 rule for money?

The 70/20/10 rule allocates 70% of income to living and operating expenses, 20% to savings or debt repayment, and 10% to investing or reinvestment. Entrepreneurs with irregular income often adjust these ratios seasonally, but the framework provides a useful starting point for managing variable cash flow.

Is $200,000 enough to work with a financial advisor?

For many fee-based advisors, $200,000 is a workable starting point — though minimums vary by firm. Many advisors weigh income potential and planning complexity alongside current assets. Engaging one early, before wealth accumulates, typically produces better long-term outcomes than waiting.

What retirement accounts are best for self-employed entrepreneurs?

SEP IRAs and Solo 401(k)s are the most popular options due to their high contribution limits and tax advantages. The right choice depends on your income level, business structure, and whether you have employees. Running both options through a financial advisor with your actual numbers will clarify which one saves you more.

When should a business owner hire a financial advisor?

Ideally at formation, when entity structure, tax strategy, and insurance decisions carry long-term consequences that compound over time. Adding partners, rapid revenue growth, and exit planning are also clear signals that professional guidance is overdue.