Introduction

Competing for talent against larger employers is one of the quieter frustrations of running a small business. A regional manufacturer or a 10-person tech firm can't match the benefits budgets of Fortune 500 companies — but that doesn't mean benefits are optional. According to MetLife's 2024 Employee Benefit Trends Study, 59% of employees said the benefits offered to them were an important reason they came to work for their organization.

For small businesses operating on tighter margins, that's a direct signal: benefits aren't just a compliance checkbox — they're a hiring and retention tool. A well-structured package lets you compete for skilled people without outspending larger employers on salary alone.

This guide covers what every small business owner needs to know:

- Which benefits are legally required

- Which optional benefits move the needle on hiring and retention

- How to structure a retirement plan for your team

- How to manage costs without gutting your package

Key Takeaways

- Businesses with fewer than 50 employees aren't required to offer health insurance under the ACA, but FICA contributions, workers' compensation, and unemployment insurance are mandatory from day one

- Health insurance, retirement plans, and paid time off have the strongest influence on employee retention decisions

- SEP-IRAs, SIMPLE IRAs, and 401(k)s each reduce taxable income for both the business owner and employees — the right choice depends on headcount and contribution goals

- Optional benefits — dental, vision, FSAs, disability coverage, flexible work — can differentiate a small employer without a large budget

- Start by surveying what employees actually value, then build your benefits package around those priorities

Legally Required Employee Benefits for Small Businesses

Federal law sets a baseline that applies to all employers regardless of size. State laws can add to those requirements — and in Michigan and Minnesota, several obligations kick in well below the federal thresholds most owners think of first.

Mandatory Federal Benefits

FICA contributions are non-negotiable. Employers must withhold Social Security and Medicare taxes from employee wages and match those contributions dollar for dollar. The employer FICA rate is 7.65% total — 6.2% for Social Security and 1.45% for Medicare — applied to every paycheck.

Workers' compensation insurance is state-mandated in nearly every state, and the thresholds are lower than many owners expect:

- Michigan: Coverage is required if you regularly employ 3 or more employees, or 1 employee working 35+ hours per week for 13 or more consecutive weeks. Noncompliance can result in fines, imprisonment from 30 days to 6 months, or a court order barring you from employing workers until you obtain coverage.

- Minnesota: Employers with employees must carry coverage or be approved as self-insured. Penalties can reach up to $1,000 per employee per week during uninsured periods.

Federal unemployment insurance (FUTA) applies at a rate of 6.0% on the first $7,000 of each employee's wages annually. Most employers qualify for a credit of up to 5.4% when they pay state unemployment taxes on time, bringing the effective federal rate down to just 0.6%.

ACA Requirements and State Leave Laws

Payroll tax obligations are just one layer of compliance. Coverage and leave requirements add another — and the thresholds here may be lower than you expect.

The ACA's employer mandate only applies to businesses with 50 or more full-time equivalent (FTE) employees. For ACA purposes, a full-time employee averages at least 30 hours per week or 130 hours per month. Businesses under this threshold are not subject to shared responsibility penalties.

FMLA sets a similar bar: it covers private employers with 50 or more employees within 75 miles of a worksite, entitling eligible employees to 12 weeks of unpaid, job-protected leave for qualifying events.

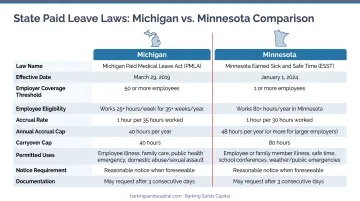

State law, however, reaches much further. Michigan and Minnesota both have paid leave requirements that apply far below the FMLA threshold:

| Law | Applies To | Accrual |

|---|---|---|

| Michigan Earned Sick Time Act (eff. Feb. 21, 2025) | All employers with 1+ employees | 1 hour per 30 hours worked; small businesses (≤10 employees) must allow use of up to 40 paid hours/year |

| Minnesota Earned Sick and Safe Time (eff. Jan. 1, 2024) | Employees expected to work 80+ hours/year in MN | 1 hour per 30 hours worked, up to 48 hours/year |

| Minnesota Paid Leave (eff. Jan. 1, 2026) | Nearly all MN employers, regardless of size | Up to 12 weeks family leave + 12 weeks medical leave, capped at 20 weeks combined |

These state-level obligations exist independently of the ACA and FMLA — meaning even a one-person shop in Michigan or Minnesota carries real compliance responsibilities. Understanding this baseline is the starting point for building a benefits strategy that works for your business.

Optional Benefits That Help Small Businesses Compete

Mandatory benefits set the floor. The benefits that actually win candidates and keep existing employees from looking elsewhere are the ones you choose to offer.

Health and Wellness Benefits

Health insurance is the most valued optional benefit for most workers, even though businesses with fewer than 50 employees aren't required to provide it. The main plan types to understand:

- PPO/HMO group plans: Traditional group coverage with predictable premiums; employees can see a wider network (PPO) or work within a defined provider network at lower cost (HMO)

- High-Deductible Health Plans (HDHPs): Lower premiums paired with higher deductibles; best paired with an HSA to help employees offset out-of-pocket costs

- Health Reimbursement Arrangements (HRAs): The employer reimburses employees for individual insurance premiums and qualified medical expenses instead of offering a group plan, making them a practical option for very small businesses that want to offer health benefits without managing a group policy

Dental and vision are typically structured as add-ons to a primary health plan or standalone supplemental policies. They carry relatively low premiums and are a consistent priority for employees. The CDC notes that routine dental visits allow for preventive care and early detection of oral disease — a meaningful health outcome, not just a perk.

Disability insurance fills an income gap if an employee can't work due to illness or injury:

- Short-term: Covers 2–6 months, typically replacing near-full income

- Long-term: Replaces 50–70% of income for extended periods

Neither Michigan nor Minnesota mandates employer-provided disability coverage (state-mandated short-term disability programs apply only in California, Hawaii, New Jersey, New York, Rhode Island, and Puerto Rico). Offering it voluntarily, particularly long-term disability, sets a smaller employer apart from most competitors in the market.

Beyond health coverage, tax-advantaged accounts give employees another layer of financial protection worth understanding.

Financial and Tax-Advantaged Benefits

Flexible Spending Accounts (FSAs) let employees set aside pre-tax dollars for eligible medical or dependent care expenses. The 2025 health FSA contribution limit is $3,300, with a carryover option of up to $660 if the plan permits it. The "use it or lose it" rule applies to amounts above any allowed carryover.

Health Savings Accounts (HSAs) are available to employees enrolled in an HDHP. Unlike FSAs, HSA balances roll over year to year and are fully portable. The 2025 contribution limits are $4,300 for self-only and $8,550 for family coverage. HSAs carry a triple tax advantage: contributions are tax-deductible, account growth is tax-free, and withdrawals for qualified medical expenses are tax-free.

Lifestyle and Supplemental Benefits

Some of the most effective differentiation for small employers doesn't require large dollar outlays:

- Flexible or remote work: Small businesses often have a structural advantage here. Less bureaucracy translates to more genuine flexibility than most large employers can offer

- PTO policies: Even a modest paid time off policy signals that you're invested in employee wellbeing

- Group term life insurance: Low-cost for the employer and reliably valued by employees, especially those with families

- Professional development and tuition reimbursement: Signals that the company is invested in employees' long-term growth, which matters particularly to younger workers

Retirement Plans: A High-Value Benefit for Small Business Employees

Pew Research reported in 2024 that more than 40% of small business employers do not offer retirement benefits. That gap is a real opportunity: offering a retirement plan creates an immediate differentiator while generating tax advantages for the owner as well.

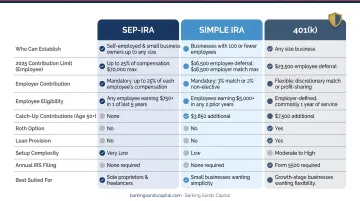

SEP-IRA, SIMPLE IRA, and 401(k): What's the Difference?

SEP-IRA

- Employer contributions only (employees cannot contribute)

- 2025 limit: up to 25% of compensation, capped at $70,000

- Contributions are deductible as a business expense

- Minimal administration; ideal for sole proprietors or businesses with few employees and variable income

SIMPLE IRA

- Both employee and employer contributions allowed

- 2025 employee deferral limit: $16,500; catch-up for age 50+: $3,500; SECURE 2.0 added a higher catch-up of $5,250 for ages 60–63

- Employer must either match employee contributions up to 3% of compensation, or make a 2% non-elective contribution for all eligible employees

- Lower administrative burden than a 401(k); suited for businesses with up to 100 employees

401(k)

- Highest contribution limits: employees can defer $23,500 in 2025, with a combined employer/employee total of up to $70,000

- Can include profit-sharing features

- More complex to administer, but the SECURE 2.0 Act significantly improved the economics for new plan sponsors: eligible employers with 50 or fewer employees can claim a startup cost tax credit covering 100% of qualified startup costs, up to $5,000 per year for three years

The right structure depends on three factors: your workforce size, how much cash flow you can commit to employer contributions, and whether you want employees deferring their own money. Barking Sands Capital works with small business owners across Minnesota and Michigan to align retirement plan selection with their broader tax and financial planning picture — so the plan serves both the owner and the team.

How to Build Your Small Business Benefits Package

Step 1: Survey Your Employees First

Before committing budget, find out what your team actually values. A short anonymous questionnaire — covering health coverage, retirement savings, flexibility, and professional development — often reveals a gap between what owners assume employees want and what employees actually prioritize. Tailoring to real preferences produces better retention outcomes per dollar spent.

Step 2: Start With Essentials, Then Layer

A practical sequencing approach:

- Cover mandatory benefits first (FICA, workers' comp, state leave laws) — compliance is non-negotiable

- Add health coverage. Even an HRA or HDHP option signals meaningful investment in your team

- Establish a retirement plan. A SIMPLE IRA with a modest employer match communicates long-term commitment to employees' financial future

- Layer in supplemental benefits (dental, vision, FSA, flexible work) as budget allows

Even one well-executed voluntary benefit, properly communicated, outperforms a longer list of poorly understood options.

Step 3: Communicate Benefits Consistently

Well-designed packages go underutilized when employees don't understand what's available. Regular communication matters:

- Cover all benefits thoroughly during onboarding

- Review benefit options annually (not just during open enrollment)

- Send reminders before FSA deadlines and open enrollment windows

- Make it easy to ask questions

The return on a benefits investment depends partly on employees actually using what you've built.

A fee-based financial advisor like Barking Sands Capital, an independent RIA serving small business owners across the Midwest since 2004, can help map out a benefits strategy that fits your budget while staying competitive in your local market.

Managing the Cost of Employee Benefits

According to the latest BLS Employer Costs for Employee Compensation report, private-industry employer compensation averaged $46.60 per hour worked, with benefits accounting for $14.01 per hour — roughly 30.1% of total compensation. Benefits are a material cost, and managing them strategically matters.

Practical cost-control strategies:

- Bundle insurance lines with a single carrier to access multi-line discounts

- Offer voluntary benefits that employees purchase at group rates — the employer enables access without absorbing the full cost

- Maximize existing plans before adding new coverage — employees may not be fully utilizing what's already available

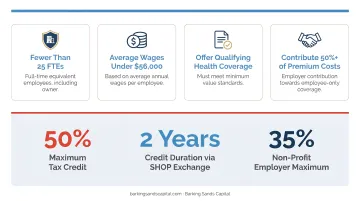

The Small Business Health Care Tax Credit is worth evaluating if you're offering or considering health coverage. Businesses that qualify can receive a federal tax credit worth up to 50% of employee premium costs (35% for tax-exempt employers). Eligibility requirements:

- Fewer than 25 FTEs

- Average employee wages of approximately $65,000 or less (inflation-adjusted)

- Pay at least 50% of full-time employee premium costs

- Offer coverage through the SHOP Marketplace

Retirement plan costs have their own offset as well. SECURE 2.0 startup credits cover up to $5,000/year for three years, with 100% coverage for employers with 50 or fewer employees — effectively eliminating the launch cost barrier for most small businesses starting a new 401(k).

Frequently Asked Questions

What is a small employee benefit plan?

A small employee benefit plan is any employer-sponsored benefit beyond base wages — from legally required coverages like workers' compensation and FICA contributions to voluntary offerings like health insurance, retirement savings plans, and paid leave. These programs support employees' health, financial security, and overall wellbeing.

What are the best health insurance plans for small businesses?

The most practical options are group health plans (PPO or HMO), high-deductible health plans paired with HSAs, and Health Reimbursement Arrangements for businesses not offering group coverage. The best fit depends on your workforce size, budget, and employee demographics.

How much do small businesses pay for employee health insurance?

According to KFF's 2024 Employer Health Benefits Survey, average employer contributions were $7,584 for single coverage and $19,276 for family coverage annually. Small firms (3–199 workers) had average single premiums of $9,131, with employees contributing about $1,204 of that cost.

Are small businesses required to offer benefits to employees?

Only certain benefits are federally mandated — FICA contributions, workers' compensation (state-mandated), and unemployment insurance apply regardless of size. Health insurance is only required under the ACA for businesses with 50+ FTEs. Most other benefits are voluntary, though strategically important for recruiting and retention.

What retirement plan options are available for small businesses?

Three options cover most small business situations, each with tax advantages for both employer and employees:

- SEP-IRA: Employer contributions only; high limits, minimal administration

- SIMPLE IRA: Employee and employer contributions; suited to companies with up to 100 employees

- 401(k): Highest contribution limits and most flexibility, with more administrative complexity

How can small businesses afford competitive employee benefits?

Start with high-impact, lower-cost benefits — flexible work arrangements and a retirement plan with a modest employer match can meaningfully close the gap with larger employers. Take advantage of available tax credits, including the SHOP marketplace health care credit and SECURE 2.0 retirement plan startup credits. A licensed financial advisor can identify cost-effective options suited to your specific budget.