Personal and family financial planning replaces that reactive pattern with a coordinated roadmap. It connects budgeting, savings, debt management, insurance, retirement, college funding, and estate planning into one strategy where short-term decisions don't quietly undermine long-term goals.

This guide walks through each component, how to build a plan from scratch, and where professional guidance makes the biggest difference. Whether you're a young family just getting started or approaching retirement with complex needs, the structure here applies.

Key Takeaways

- A family financial plan coordinates every member's needs, from daily cash flow to long-term wealth transfer.

- Core pillars include budgeting, emergency savings, debt management, insurance, retirement, college savings, and estate planning.

- Planning is not a one-time event — it must evolve with life stages and major milestones.

- A qualified, independent financial advisor provides integrated, personalized strategy that generic tools can't replicate.

What Is Personal and Family Financial Planning?

Personal financial planning is the process of organizing income, expenses, savings, and investments around specific goals — not just keeping the lights on each month. The key distinction is its forward-looking nature: it asks where you want to be in 5, 10, or 30 years, then works backward to build a path.

Family financial planning adds real complexity to that process. Multiple earners, dependents, competing priorities, and different risk tolerances all have to fit into one coherent strategy. A couple with two kids might be pulling from the same pool of income to cover:

- Childcare or private school costs

- Mortgage payments and home maintenance

- Underfunded retirement accounts

- A looming college savings gap

The payoff for coordinating all of this is substantial. Families with a structured plan report lower financial stress, stronger emergency preparedness, and fewer short-term decisions that derail long-term goals. According to a 2025 CFP Board study, individuals working with CFP® professionals were more likely to have three-month emergency funds (78% vs. 53%) and a will (57% vs. 25%) than those without professional guidance.

Core Components Every Family Financial Plan Should Cover

These are the building blocks — the recurring areas every plan must address regardless of family size or income. Each one connects to the others: a decision in one area almost always ripples into the rest.

Budgeting and Cash Flow Management

A realistic budget is the foundation everything else rests on. It maps income against fixed expenses (mortgage, utilities, insurance premiums) and variable costs (groceries, childcare, healthcare) to reveal what's genuinely available for saving and investing.

The 50/30/20 rule — popularized by Elizabeth Warren and Amelia Warren Tyagi in All Your Worth — offers a practical starting framework:

- 50% of after-tax income to needs

- 30% to wants

- 20% to savings and debt repayment

In practice, many households can't cleanly fit this split. BLS 2024 Consumer Expenditure data show that housing and transportation alone consumed 50.4% of average household spending — before food, healthcare, or debt repayment. Treat 50/30/20 as a benchmark to compare against, not a rigid rule.

Emergency Fund and Debt Management

An emergency fund covering three to six months of living expenses should be established before aggressively investing. Without it, families raid retirement accounts or take on high-interest debt when unexpected costs hit — the exact situations that permanently damage long-term plans.

The Federal Reserve's 2025 SHED report found 37% of adults couldn't cover a $400 emergency with cash or equivalent — a reminder of how quickly an unplanned expense becomes a financial setback.

On debt, not all of it needs the same urgency:

- High-interest consumer debt (credit cards, personal loans): prioritize elimination

- Low-interest debt (mortgages, some student loans): can co-exist with investing

Two common repayment methods — the avalanche (highest interest rate first) and snowball (smallest balance first) — both work; the best one is whichever you'll actually stick with.

Insurance and Risk Protection

Insurance protects the entire plan from catastrophic disruption. The core coverage types families need:

- Life insurance — income replacement for dependents

- Disability insurance — protects earning power, which is your most valuable asset before retirement

- Health insurance — prevents medical costs from destroying savings

- Long-term care insurance — critical for pre-retirees managing future care costs

- Property and liability — homeowners, auto, umbrella

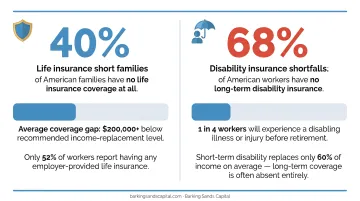

The coverage gaps are significant. LIMRA's 2024 Insurance Barometer found 42% of American adults — roughly 102 million people — say they need or need more life insurance. The Council for Disability Awareness reports at least 51 million working adults lack disability insurance beyond basic Social Security.

Risk management isn't only a pre-retirement concern. A young parent with dependents and a mortgage — where a single income loss can unravel everything — often has a more urgent need for life and disability coverage than someone with a paid-off home and grown children.

Retirement and College Savings

The "oxygen mask" rule applies here: secure your own financial future before funding someone else's. Children can borrow for college; parents cannot borrow for retirement.

At minimum, contribute enough to your 401(k) to capture any employer match — that's an immediate 50-100% return on that contribution. One in four workers misses out on their full 401(k) match, with workers under 30 most likely to leave that money behind.

Key savings vehicles for 2026:

| Account | 2026 Contribution Limit |

|---|---|

| 401(k) / 403(b) | $24,500 |

| Catch-up (age 50+) | Additional $8,000 |

| Enhanced catch-up (ages 60-63) | Additional $11,250 |

| Traditional / Roth IRA | $7,500 |

| 529 plan | No federal annual cap |

For college, the costs are significant. College Board's 2024-25 data put annual budgets at $29,910 for public in-state students and $62,990 for private nonprofit institutions. Fifty percent of recent bachelor's graduates borrowed, with average debt of $29,300 among borrowers.

Estate Planning and Legacy

Estate planning isn't only for wealthy families. Every household with dependents needs, at minimum:

- A will — for asset distribution and guardian designation

- Durable power of attorney — for financial decisions if incapacitated

- Healthcare directive — for medical decisions

- Updated beneficiary designations on every account and policy

That last point deserves emphasis. According to FINRA, a transfer-on-death designation or beneficiary form can supersede a will entirely. Outdated beneficiary designations are one of the most common ways assets pass to unintended recipients — former spouses, deceased relatives, or estranged family members.

Only 24% of adults have a will, according to Caring.com's 2025 study. Trusts add control, privacy, and tax advantages for larger estates, but a basic will at minimum ensures your assets go where you intend — and that someone you've chosen, not a court, makes decisions for your children.

How to Build Your Family Financial Plan: A Step-by-Step Approach

The previous section covered what belongs in a plan. Here's how to build one.

Step 1: Assess Your Current Financial Picture

Start with an honest inventory:

- Income sources: salaries, business income, rental income, side work

- Assets: savings accounts, retirement balances, home equity, investment accounts

- Liabilities: mortgage, car loans, student debt, credit cards

- Monthly cash flows: what actually comes in and goes out

This baseline is where planning begins. Without it, any goal you set is a guess.

Step 2: Define and Prioritize Goals

Separate goals by time horizon:

- Short-term (1–3 years): Build emergency fund, eliminate credit card debt

- Medium-term (3–10 years): Home purchase, children's education savings

- Long-term (10+ years): Retirement, legacy planning

For families, this step requires actual conversation. Competing priorities surface here — one partner may prioritize college savings while the other wants to accelerate mortgage payoff. Aligning on shared values before assigning dollar targets prevents ongoing friction.

Step 3: Build a Budget and Automate Savings

Translate goals into monthly dollar allocations, then automate them. Set up automatic transfers to savings and investment accounts on payday — before discretionary spending happens, not after.

Automation removes willpower from the equation. The money moves before you have a chance to spend it elsewhere. A simple setup might include:

- Direct deposit split between checking and savings

- Automatic 401(k) or IRA contributions on payday

- Scheduled transfers to goal-specific accounts (college fund, home down payment)

Step 4: Protect the Plan with Insurance and Legal Documents

Review coverage gaps at each life stage. Critical moments for reassessment:

- When children are born (life insurance, will with guardian designation)

- After significant income increases (coverage limits may need updating)

- As parents retire (Medicare planning, long-term care)

- After major asset growth (umbrella liability, estate planning)

Legal documents — wills, powers of attorney, healthcare directives — go stale. They need to be revisited after any major life change, not just created once and filed away.

Step 5: Monitor, Review, and Adjust Annually

A financial plan is a living document. Schedule a formal review at least once per year — and immediately after major life events:

- Marriage, divorce, or birth of a child

- Job change or significant income shift

- Inheritance or large asset purchase

At each review, track progress toward goals, rebalance investment allocations, and confirm insurance and legal documents still reflect your situation.

Common Mistakes in Family Financial Planning

These are the patterns that quietly derail otherwise well-intentioned families.

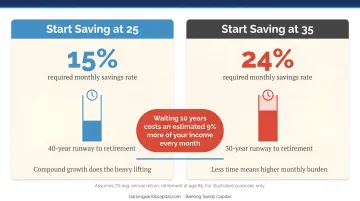

Ignoring Retirement Savings Until "Later"

The math on delayed saving is brutal. Fidelity estimates a 25-year-old needs to save 15% of income to retire comfortably; starting at 35 requires 23% to reach the same outcome. EBRI's Retirement Security Projection Model reports an average retirement savings shortfall of about $48,000 per individual.

Every year of delay shrinks your runway and increases the savings rate you'll need to compensate. Starting earlier — even with smaller amounts — consistently outperforms starting later with larger contributions.

Leaving Family Members Out of Financial Decisions

When one partner controls all household finances and the other is largely uninformed, the family is one health crisis or divorce away from serious vulnerability.

Federal Reserve research found that financial knowledge gaps widen in households with one dominant financial manager — particularly affecting the less-engaged partner's preparedness during widowhood or divorce. Both spouses need working familiarity with the household's financial picture.

Treating the Plan as a One-Time Event

Setting a plan in 2018 and never revisiting it means navigating 2025 with outdated assumptions about income, tax law, inflation, and goals. The plan has to keep up with your life.

This is why proactive plan monitoring matters — an advisor who schedules regular reviews catches drift before it becomes damage, rather than waiting for clients to raise the alarm.

How a Financial Advisor Can Strengthen Your Family's Plan

Generic financial information can only take you so far. A qualified advisor builds recommendations around your complete picture: income, assets, goals, tax situation, risk tolerance, and family structure — not rules of thumb that weren't designed with your life in mind.

The Fiduciary Distinction

Not all advisors operate under the same standard. A fee-based Registered Investment Advisor (RIA) owes clients a fiduciary duty under the SEC Advisers Act — a legal obligation to act in the client's best interest. Commission-based brokers operate under a suitability standard, meaning recommendations must be appropriate but not necessarily optimal for the client.

Barking Sands Capital operates as an independent RIA with a fee-based compensation structure. An independent RIA cannot be paid commissions on accounts they manage — a fundamentally different incentive structure than a commission-based model. Clients pay transparent fees (percentage of assets, flat fee, or hourly), so the advisor's financial interest aligns directly with the client's success.

Integrated Planning vs. Fragmented Advice

The most common planning failure isn't bad advice in any single area. It's advice that doesn't account for how each area affects the others.

A Roth conversion that looks excellent on paper can trigger Medicare surcharges (IRMAA) if it isn't coordinated with income planning. A life insurance purchase that seems appropriate in isolation may overlap with estate strategies the family already has in place.

Barking Sands Capital's proprietary InteProcess™ is built to address this. It integrates legal, insurance, tax, retirement, and financial planning into one coordinated strategy — with designated professionals across disciplines working as a team rather than in separate tracks. The result is planning that catches cross-functional implications that piecemeal advice misses.

When Professional Help Becomes Essential

Anyone can benefit from professional guidance, but certain situations make the cost of DIY mistakes high enough that professional help pays for itself:

- Stock option or equity compensation planning

- Business ownership and succession planning

- Blended family estate issues

- Approaching retirement income sequencing

- Medicare planning and long-term care decisions

Barking Sands Capital's advisor Curtis Hewitt specializes in Medicare and Long-Term Care for clients in Michigan and Minnesota — a niche that's increasingly critical as more families navigate healthcare decisions within retirement planning.

What to Look for in an Advisor

- Verify credentials: CFP® or ChFC designations indicate comprehensive planning training

- Confirm fiduciary status — ask directly: "Are you a fiduciary at all times?"

- Understand compensation: fee-only or fee-based structures minimize conflicts

- Ask about their planning process and how often they proactively communicate

- Confirm they take a holistic view, not just investment management

Frequently Asked Questions

What is the difference between personal financial planning and family financial planning?

Personal financial planning focuses on an individual's goals, income, and finances in isolation. Family financial planning adds complexity: multiple earners, dependents, shared goals, competing priorities, and intergenerational needs like college funding and estate transfer all have to be coordinated within one plan.

How often should a family review their financial plan?

At minimum, annually — and after any major life event. Marriage, divorce, a new child, a job change, a significant inheritance, or a major asset purchase all change the equation enough to warrant an immediate review, not just waiting for the next scheduled check-in.

Should I prioritize retirement savings or saving for my children's college education?

Prioritize retirement, particularly capturing any employer 401(k) match first. Children have access to loans, scholarships, grants, and work-study programs. Parents have no equivalent safety net for retirement — there's no "retirement loan" available when you run short at 68.

What is the 50/30/20 rule and how does it apply to family budgeting?

It allocates 50% of after-tax income to needs, 30% to wants, and 20% to savings and debt repayment. For most families it works as a starting benchmark. BLS data show housing and transportation alone often exceed 50% of spending, so expect to adjust based on your actual cost of living.

What documents does every family financial plan need?

At minimum: a will (or trust), durable power of attorney, healthcare directive, updated beneficiary designations on every account and policy, and a current inventory of all assets and liabilities. The inventory is easy to skip and critical to have.

When does it make sense to hire a financial advisor for family financial planning?

It becomes most valuable during major life transitions, when managing significant assets, coordinating complex tax situations, approaching retirement, or navigating estate planning. These are areas where an uncoordinated decision is costly and difficult to undo.