Early retirement isn't just regular retirement with better timing. It introduces a set of financial challenges that standard retirement planning simply doesn't address: a 30–40 year drawdown period, no Medicare until 65, limited access to tax-advantaged accounts before 59½, and a total nest egg requirement that dwarfs what a traditional retiree needs.

This guide walks through a six-step framework for making early retirement viable — covering your savings strategy, the right account types, healthcare coverage, tax-efficient withdrawals, and how to work with an advisor who actually specializes in this. The earlier you start, the more tools you have available.

Key Takeaways

- Early retirement demands saving 25–50%+ of income — far above the national average of 2.6%

- Taxable brokerage accounts are essential because they carry no age-based withdrawal restrictions

- Bridging healthcare coverage before Medicare kicks in at 65 is one of the most expensive gaps early retirees face

- Roth conversions and strategic account sequencing form the backbone of a tax-efficient withdrawal plan that extends how long your portfolio lasts

- Plans need annual reviews; early retirement is dynamic, not a one-time decision

Step 1: Define Your Early Retirement Vision and Set a Target Number

What "Early Retirement" Actually Means

Early retirement looks different for everyone. Age 50, 55, and 62 each require dramatically different savings strategies — and so do different retirement styles. A full stop is not the same as part-time consulting or an encore career that generates modest income. Being specific about what you're planning for changes every variable that follows.

Consider the range of what "retired" might look like for you:

- Full stop: No income, full draw on portfolio from day one

- Part-time or consulting: Modest earned income reduces early withdrawal pressure

- Encore career: Structured work with purpose, potentially delaying Social Security and portfolio draws

Calculating Your Number

The widely cited 4% rule — withdrawing 4% of your portfolio annually — was originally based on Bengen's 1994 historical research covering a roughly 33-year retirement window. That's already at the edge of what early retirees need.

Vanguard notes the 4% framework is designed around a 30-year horizon. For retirements starting before 60, you're likely looking at 35–40 years.

Morningstar's 2026 research estimates a safe starting rate of just 3.3% for a 40-year retirement. Fidelity suggests retiring before 62 may require saving 33x annual expenses, not 25x.

In practice: model multiple scenarios rather than locking into one number. Run projections at 25x, 30x, and 33x your expected annual expenses to see the range and what savings rate each requires.

What to Include in Your Projections

- Lifestyle inflation over time (spending often rises in early retirement, not falls)

- One-time large expenses — home renovations, family support, travel goals

- Healthcare costs as a separate budget line item before Medicare

- A retirement that may span four decades

Step 2: Build an Aggressive and Diversified Savings Strategy

Increase Your Savings Rate Significantly

Conventional guidance suggests saving 10–20% of income for a traditional retirement. Early retirement typically requires 25–50% or more. For context, the U.S. personal saving rate was 2.6% as of April 2026. A 30% savings rate isn't just ambitious — it's in a completely different category from what most Americans are doing.

Getting there usually requires working two levers simultaneously:

- Cut discretionary spending — identify fixed versus flexible expenses and systematically reduce the flexible ones

- Grow income — raises, side income, and entrepreneurship accelerate the timeline more than cost-cutting alone

Most people who hit aggressive savings targets do both — and that combination is also what makes the income diversification in the next step viable sooner.

Diversify Your Income Streams Now

Early retirees face a coverage gap that traditional retirees don't: no Social Security, no Medicare, and no penalty-free retirement account access for potentially a decade or more. That makes building multiple income streams during your working years essential.

Build these income streams during the accumulation phase:

- Dividend-paying stocks and equity income funds

- Bonds and fixed-income instruments (bond index funds currently yield around 4.5%)

- Real estate rental income

- Fixed-index annuities for guaranteed income floors

Multiple income streams also reduce sequence-of-returns risk — the danger that a market downturn in your first few retirement years permanently damages your portfolio before it can recover.

Step 3: Use the Right Investment Accounts for Early Retirement

The Early Retirement Account Problem

The core challenge: 401(k)s and traditional IRAs impose a 10% early withdrawal penalty on distributions before age 59½. Most retirement planning assumes you won't need those funds until then. Early retirees can't make that assumption.

This is why account "location" matters as much as total accumulation. Where your money sits determines when you can access it without penalty.

Strategies to Access Funds Before 59½

Three IRS-sanctioned strategies let you tap retirement accounts before 59½ without triggering the penalty:

Rule of 55 — If you leave your job in or after the calendar year you turn 55, you can take penalty-free distributions from that employer's 401(k). The funds must stay in the employer plan; rolling them into an IRA first eliminates this option.

Section 72(t) SEPP — The IRS permits penalty-free IRA withdrawals through Substantially Equal Periodic Payments. Payments must continue for at least five years or until age 59½, whichever is longer. Modifying the schedule early triggers recapture of the full penalty plus interest — this commitment is binding.

Roth conversion ladder — Convert traditional IRA or 401(k) funds to a Roth IRA each year in early retirement. After five years, those converted amounts can be withdrawn tax- and penalty-free. It requires advance planning, but it's the most flexible of the three options.

The Critical Role of Taxable Brokerage Accounts

Taxable brokerage accounts are the most flexible asset in an early retiree's toolkit:

- No contribution limits

- No age-based withdrawal restrictions

- No penalties

The trade-off is tax treatment — gains are taxable. That's manageable. For 2025, long-term capital gains are taxed at 0% for single filers with taxable income up to $48,350 and married filers up to $96,700.

Early retirees who control their taxable income can harvest gains at the 0% rate. Index funds and tax-loss harvesting reduce the drag further.

Barking Sands Capital works with clients to coordinate account placement across taxable accounts, traditional IRAs, and Roth IRAs — including building Roth conversion ladders as part of a broader early retirement income plan.

Step 4: Bridge the Healthcare and Income Gap Before Age 65

Planning for Healthcare Without Medicare

Medicare eligibility starts at 65. Retire at 55, and you're responsible for your own health coverage for a decade. This is often the most expensive and least anticipated part of early retirement planning.

Fidelity estimates that a single 65-year-old retiree will spend $172,500 on healthcare and medical expenses throughout retirement. For early retirees, those costs start earlier — before Medicare's coverage even begins.

KFF estimates the 2026 national average unsubsidized premium for a 60-year-old at $15,914 per year for benchmark silver coverage — and that's just premiums, not out-of-pocket costs.

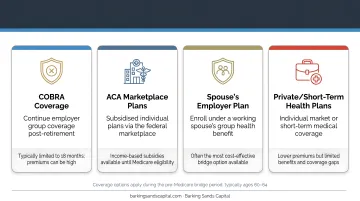

Your four main options for coverage:

- COBRA — extends employer coverage for up to 18 months post-employment (some qualifying events extend this to 36 months). Premiums can reach up to 102% of the plan's full cost. Useful as a bridge, rarely a long-term solution.

- Spouse's employer plan — if applicable, often the most cost-effective option

- ACA marketplace plan — premiums are subsidized based on modified adjusted gross income. Early retirees with low withdrawal income may qualify for significant subsidies. Capital gains, interest income, and taxable IRA distributions all count toward MAGI.

- Part-time work with benefits — some early retirees carry part-time employment specifically for healthcare

The ACA subsidy angle deserves dedicated planning. Managing which accounts you draw from — and how much — directly affects your subsidy eligibility. That same withdrawal sequencing also determines how much income you need to generate before Social Security kicks in.

Bridging the Income Gap Until Social Security

For those born in 1960 or later, full Social Security retirement age is 67. Claiming at 62 permanently reduces benefits to 70% of the full amount. Waiting until 70 earns an additional 8% per year beyond full retirement age — a meaningful difference over a 20–30 year benefit period.

Early retirees with other income sources generally benefit from delaying Social Security. Strategies to bridge the gap:

- Draw from taxable accounts first (preserving tax-advantaged accounts for growth)

- Execute the Roth conversion ladder over several years

- Keep 1–2 years of expenses in cash or short-term reserves to avoid forced selling in a down market

- Use part-time or consulting income in early retirement years to reduce portfolio draw rates

Step 5: Build a Tax-Efficient Withdrawal Strategy

Withdrawal Rate and Portfolio Longevity

The 4% rule was built for 30-year retirements. For 35–40 year horizons, targeting 3–3.5% in year one provides materially better odds of portfolio survival. Starting lower gives the portfolio more room to absorb bad early years — when sequence-of-returns risk is highest — without permanently impairing the long-term balance.

The Three-Bucket Tax Framework

Tax diversification in retirement means holding assets across three account types simultaneously:

| Account Type | Tax Treatment | Example |

|---|---|---|

| Pre-tax (traditional IRA, 401k) | Taxable on withdrawal | Traditional 401(k) |

| After-tax (taxable brokerage) | Capital gains rates | Brokerage account |

| Tax-free (Roth IRA) | Tax-free on qualified withdrawal | Roth IRA |

Having all three gives you annual flexibility to manage taxable income — staying in lower brackets, preserving ACA subsidies, and avoiding Medicare IRMAA surcharges that kick in above $109,000 for single filers and $218,000 for married filers.

Roth Conversions During Low-Income Years

If you stop working before drawing Social Security, your taxable income may be lower than at any point in your career. That's the ideal window to convert traditional IRA funds to Roth — paying tax now at a lower rate to avoid larger bills later.

This strategy requires careful coordination because the conversion amount affects several interconnected variables:

- MAGI levels — higher conversions can push you into a higher tax bracket

- ACA subsidy eligibility — excess income reduces or eliminates premium tax credits

- IRMAA thresholds — Medicare surcharges trigger above $103,000 (single) and $206,000 (married) in 2024

Getting the math wrong in either direction (converting too little or too much) has real consequences. Barking Sands Capital's InteProcess™ coordinates Roth conversion planning with tax and Medicare planning together, so these decisions don't get made in isolation.

Step 6: Review, Adjust, and Work With an Advisor Who Specializes in Retirement Planning

Early Retirement Is Not Set-and-Forget

Markets change. Inflation surprises. Spending habits don't match projections. Annual plan reviews aren't optional — they're what keeps an early retirement strategy functional over decades.

One practical test before fully retiring: live on your planned retirement budget for three to six months while still employed. This "trial retirement" approach reveals spending gaps and lifestyle mismatches before they become permanent problems. It's far easier to adjust a plan before you've left the workforce than after.

What to Look for in an Advisor

Not every financial advisor is equipped for early retirement planning. Look for:

- Fee-based compensation — advisors who charge fees rather than earning commissions have no financial incentive to push products that don't fit your plan

- Credentials like CFP® or ChFC — these require rigorous education, exams, experience, and ongoing ethics requirements

- Cross-domain capability — tax planning, investment management, insurance, and estate planning need to work together, not in silos

- Experience with long retirement horizons — a 30–40 year plan requires different thinking than a 15-year one

If those criteria match what you're looking for, Barking Sands Capital's team of CFP® and ChFC professionals checks each box. Their fee-based InteProcess™ coordinates investment management, tax planning, insurance, legal, and estate planning into a single integrated strategy — with offices serving clients across Minnesota, Michigan, and the broader Midwest.

Frequently Asked Questions

Frequently Asked Questions

Is $600,000 enough to retire at 62?

It depends on your expenses and other income sources. At a conservative 3.5% withdrawal rate, $600,000 generates roughly $21,000 per year. For most people, that would need to be supplemented by Social Security, part-time income, or additional savings — Medicare doesn't start until 65, and healthcare costs alone can consume a significant portion of that income.

Can an early retirement financial planner help you retire early?

Yes. A planner specializing in early retirement can identify the right savings rate, account sequencing strategy, tax plan, and healthcare bridge for your specific situation. They can also stress-test your plan against market downturns and inflation scenarios to confirm it can hold up over a 30–40 year horizon.

What is the $1,000-a-month rule for retirement planning?

It's a rough guideline: for every $1,000 per month of desired retirement income, you need approximately $240,000 saved (based on a 5% withdrawal rate). Early retirees should use a more conservative rate, pushing that target closer to $340,000 per $1,000 per month at 3.5%.

What is the 4% rule and does it apply to early retirees?

The 4% rule suggests withdrawing 4% of your portfolio in year one and adjusting for inflation each year. Because early retirees face 35–40 year retirements rather than 30, many planners recommend starting at 3–3.5% to reduce the risk of outliving your savings.

How do I get health insurance if I retire before 65?

Your main options are COBRA (up to 18 months, though costly), a spouse's employer plan, an ACA marketplace plan with potential income-based subsidies, or part-time work with benefits. Budget for healthcare explicitly — it's one of the most expensive gaps in any early retirement plan.