The short answer: a parent-owned 529 plan reduces need-based aid eligibility by a maximum of 5.64% of the account's value. On a $20,000 balance, that's roughly $1,128 — a modest trade-off for years of tax-free growth. And in many cases, the impact is even smaller.

Two factors determine exactly how much a 529 affects aid: who owns the account and which financial aid form the college uses. This guide covers both, along with how withdrawals are treated, the significant rule changes for grandparent-owned plans, and practical strategies to protect aid eligibility while keeping your savings on track.

Key Takeaways

- A parent-owned 529 is assessed at a maximum 5.64% of its value on the FAFSA — far less than assets held in a student's name

- Grandparent-owned 529 plans are not reported on the FAFSA, and withdrawals no longer count as student income under 2024–25 rules

- Qualified 529 withdrawals are never counted as student income on the FAFSA, regardless of who owns the account

- 529 balances and distributions have zero effect on merit-based scholarships

- Tax-free compounding inside a 529 delivers far more value than any reduction in need-based aid

How Financial Aid Is Calculated: The FAFSA and Student Aid Index

The FAFSA (Free Application for Federal Student Aid) is the gateway to federal grants, subsidized loans, and work-study programs — and it's used by virtually every college in the country to determine need-based aid eligibility.

Filing the FAFSA produces a Student Aid Index (SAI), which replaced the old Expected Family Contribution (EFC) starting with the 2024–25 award year under the FAFSA Simplification Act. The SAI represents the amount a family is expected to contribute toward annual college costs. Higher SAI = less need-based aid.

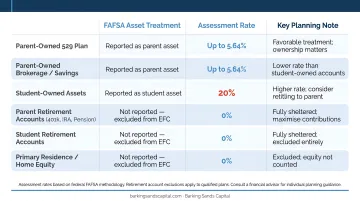

How Assets Are Weighted

The SAI formula treats parent and student assets very differently:

| Asset Type | Assessment Rate |

|---|---|

| Parent assets (including 529s) | Up to ~5.64% (derived maximum) |

| Student assets | Up to 20% |

| Retirement accounts (401(k), IRA) | Excluded entirely |

| Cash value of life insurance | Excluded entirely |

The 5.64% derived maximum for parent assets comes from the formula's two-step process: parent assets are converted at 12% of discretionary net worth, and the resulting parent contribution is assessed at up to 47%. The product of those two components (12% × 47%) yields the commonly cited 5.64% ceiling.

This is why keeping a 529 in a parent's name — rather than the student's — is one of the most direct ways to minimize its impact on aid calculations.

Income vs. Assets: Which Matters More?

Assets often get outsized attention in these conversations, but parental income drives the SAI far more than savings do. The FSA formula assesses parent income at rates up to 47%, while student available income is assessed at 50%.

Compare that to the 5.64% ceiling on parent assets — the difference is substantial. For most middle-income families, a modest pay raise will affect aid eligibility more than a $50,000 529 account. That context matters when weighing whether to save aggressively in a 529.

Roughly 268 selective colleges also require the CSS Profile, administered by the College Board, which may assess assets more broadly than the FAFSA. If your target schools are on that list, personalized guidance is worth seeking.

How 529 Plan Ownership Affects Financial Aid

The single biggest variable in how a 529 affects your aid package isn't the account balance — it's whose name is on the account.

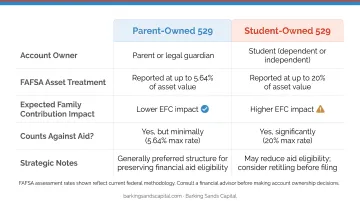

Parent-Owned 529 Plans

A 529 owned by a parent (and designated for a dependent student) is reported as a parent asset on the FAFSA. That means the derived maximum assessment rate of 5.64% applies.

Example: A $20,000 529 balance reduces need-based aid eligibility by a maximum of $1,128 per year. That's the same rate applied to a parent's regular savings or brokerage account — a 529 carries no special penalty compared to other parent savings vehicles.

Student-Owned 529 Plans

For independent students, a 529 owned by the student is reported as a student asset and assessed at up to 20%.

Example: That same $20,000 balance could reduce aid by up to $4,000 under student ownership — nearly four times the parent-owned impact.

For dependent students, the rules are slightly different: FSA guidance indicates that a qualifying education account owned by a dependent student must still be reported as a parent asset if the student reports parent information on the FAFSA. Even so, parents should own the account directly to avoid any ambiguity.

Non-Custodial Parent and Third-Party Owned 529 Plans

For divorced families, the FAFSA uses the parent who provided the greater share of financial support over the prior 12 months — not automatically the custodial parent. A 529 owned by the non-contributing parent (the parent not required to file the FAFSA) is not reported as an asset.

Accounts owned by grandparents, other relatives, or family friends are also not reported as assets on the FAFSA. Since they are neither parent nor student property, they carry no direct impact on the aid calculation.

Quick Comparison: 529 Ownership and FAFSA Impact

| Owner | FAFSA Treatment | Impact on $20,000 Account |

|---|---|---|

| Parent | Parent asset | Up to $1,128 reduction in aid |

| Independent student | Student asset | Up to $4,000 reduction in aid |

| Grandparent/relative | Not reported as asset | $0 impact |

| Non-contributing parent | Not reported | $0 impact |

How 529 Withdrawals Affect Financial Aid

Ownership determines how the account balance is counted. Withdrawals follow different rules, and most of them work in families' favor.

Qualified Withdrawals: Not Counted as Student Income

Qualified 529 withdrawals used for eligible education expenses are never reported as student income on the FAFSA, regardless of who owns the account. This is one of the clearest advantages 529 plans hold over taxable savings accounts, where investment gains could show up as reportable income.

Qualified 529 expenses include:

- Tuition and required fees

- Room and board (for at least half-time students, up to cost-of-attendance limits)

- Books, supplies, and required equipment

- Computers, software, and internet access used primarily for coursework

- Special needs services

Non-education expenses — travel, a car, personal living costs beyond allowable room and board — don't qualify.

Nonqualified Withdrawals

If you pull money out for non-education purposes, the earnings portion is subject to ordinary income tax plus a 10% federal penalty. The principal (your original contributions) is always returned tax-free.

Investment Growth Inside the Account

Unrealized investment gains inside a 529 are not separately reported on the FAFSA. The account is assessed at its current market value when you file — not on annual earnings or dividends.

Compare that to a taxable brokerage account, where dividends and capital gains appear on your tax return and could be assessed as income at significantly higher rates.

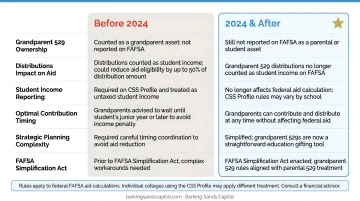

Grandparent-Owned 529 Plans: Key Rule Changes

Until recently, grandparent-owned 529s came with a significant catch. The account itself wasn't reported as an asset — but any distributions were another story.

The Old Rule (Prior to 2024–25 FAFSA)

Under the previous FAFSA, withdrawals from accounts owned by grandparents, aunts, uncles, or other relatives were reported as untaxed student income. With dependent student income assessed at 50% under the old EFC formula, a $10,000 grandparent distribution could reduce aid eligibility by as much as $5,000 the following year. This created an awkward planning problem: grandparents wanting to help were inadvertently penalizing their grandchildren's aid.

The New Rule (2024–25 FAFSA Onward)

The FAFSA Simplification Act eliminated the "money received by or paid on behalf of the student" category that previously captured these distributions. According to FSA Partner Connect guidance, beginning with the 2024–25 implementation, these cash-support categories were removed from need analysis entirely.

Under the updated rules, grandparent-owned 529s now offer a clean path to college funding:

- The account is not reported as a parental or student asset on FAFSA

- Withdrawals no longer count as untaxed student income

- Distributions have no effect on federal financial aid eligibility

For grandparents looking to reduce their taxable estate while funding a grandchild's education, this change removes the last meaningful obstacle. Contributions qualify for annual gift tax exclusion treatment, and the account balance stays out of the financial aid calculation entirely.

Strategies to Minimize the Impact on Financial Aid

A few straightforward planning decisions can meaningfully reduce the already-modest impact a 529 has on aid eligibility.

Own the Account Correctly

If you have a choice, a parent should own the 529 — not the student. This applies the 5.64% parent asset rate rather than the 20% student asset rate.

If multiple 529 accounts exist (for example, a parent-owned plan and a grandparent-owned plan), the recommended withdrawal sequence under current rules is:

- Use parent-owned 529 funds first (already reported as a parent asset, so spending it down reduces the reported balance)

- Draw from grandparent-owned funds freely — under the new FAFSA rules, there's no longer a strategic reason to save grandparent distributions for senior year

Time Contributions and Withdrawals Around the FAFSA Snapshot

The FAFSA captures a snapshot of your finances as of the date you sign it. The 2025–26 FAFSA, for example, asks for the current market value of investments "as of today." If you spend 529 funds on qualified education expenses before signing the FAFSA, those dollars no longer appear in the reported balance.

Paying a tuition bill from the 529 before your FAFSA signing date simply reflects an accurate financial picture — not a workaround, just proper timing.

Get Personalized Guidance for CSS Profile Schools

Families applying to selective schools that require the CSS Profile should not rely solely on FAFSA-based rules. The CSS Profile can treat assets more comprehensively, and the methodology varies by institution.

A fee-based financial advisor can map out your specific scenario across both systems. Barking Sands Capital includes education funding planning within its comprehensive financial planning services, working with families in Minnesota, Michigan, and across the Midwest on 529 ownership structures, withdrawal timing, and aid strategy. CFP® Andrea Cervena handles these multi-variable decisions directly with clients.

Frequently Asked Questions

How do 529 plans affect eligibility for college financial aid?

A parent-owned 529 reduces need-based aid eligibility by a maximum of 5.64% of the account's value — so a $20,000 balance affects aid by at most $1,128. Grandparent-owned plans are not reported as assets on the FAFSA, and qualified withdrawals are never counted as student income.

How does parental income affect eligibility for college financial aid?

Parental income has a significantly larger effect on the SAI than parental assets — assessed at rates up to 47%, compared to the 5.64% maximum for parent assets. High-earning families typically see a greater aid reduction from income than from any 529 balance.

Do 529 plan withdrawals count as student income on the FAFSA?

Qualified withdrawals used for eligible education expenses do not count as student income on the FAFSA, regardless of account ownership. Nonqualified withdrawals may carry tax and penalty implications, but they are generally not reported as FAFSA income either.

Will a 529 plan reduce my child's Pell Grant eligibility?

A parent-owned 529 may modestly reduce Pell Grant eligibility since it's counted as a parent asset at 5.64%. A grandparent-owned 529 will not affect Pell Grant eligibility at all under current FAFSA rules — neither the account balance nor any distributions count against the student.

Does a 529 plan affect merit scholarship eligibility?

No. Merit scholarships are awarded based on academic, athletic, or other achievements — not family income or savings. A 529 plan has no bearing on merit-based aid, regardless of its size.

What happens to 529 funds if my child doesn't go to college?

Unused 529 funds have several flexible options:

- Transfer to another eligible family member

- Use for K-12 tuition (up to $20,000 annually for years beginning after December 31, 2025, per IRS guidance)

- Apply toward student loan repayment (up to a $10,000 lifetime limit)

- Roll over into a Roth IRA for the beneficiary, subject to a 15-year account age requirement and a $35,000 lifetime cap