Introduction

Running a business demands everything — your time, your capital, and most of your mental bandwidth. What often gets pushed to the back burner is your own retirement. Unlike employees who benefit from automatic payroll deductions and an HR department nudging them toward the company 401(k), small business owners carry the entire weight of retirement planning themselves.

That creates a dangerous gap. The mistakes that fill it aren't just about saving too little. They include structural errors, missed tax advantages, and assumptions that can unravel decades of hard work — even for financially savvy owners.

This article covers five of the most common retirement planning mistakes small business owners make, why each one compounds over time, and what to do instead. Each mistake is correctable — and addressing them now, rather than later, is what separates a secure retirement from a stressful one.

Key Takeaways:

- Relying on a future business sale to fund retirement is the single riskiest assumption an owner can make

- Small business owners have access to more powerful retirement vehicles than most employees — but most underuse them

- Starting modest contributions at 35 consistently outperforms waiting until 45 to save aggressively

- The right retirement plan structure can significantly reduce your tax burden — most owners never run the comparison

- Outdated beneficiary designations can override your will and redirect assets against your wishes

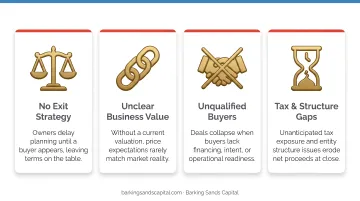

Mistake #1: Treating the Sale of Your Business as Your Entire Retirement Plan

This is the most common — and most dangerous — assumption in small business retirement planning.

The logic feels reasonable: you've spent decades building something valuable, so when the time comes, you'll sell it and live off the proceeds. The problem? According to the Exit Planning Institute, only 20% to 30% of businesses that go to market actually sell. The majority never close a deal.

It gets worse. The Exit Planning Institute's 2025 State of Owner Readiness report found that as of their 2023 survey, only 13% of business owners had a formal exit plan — meaning the vast majority are counting on an outcome they haven't prepared for and that statistically won't happen on their terms.

Why the Numbers Don't Work in Your Favor

Even when a sale does happen, it rarely unfolds as expected:

- Timelines slip — IBBA data shows median time to close runs 12 months for businesses valued between $5M and $50M, and deals under $500K carry far weaker seller-market conditions

- Valuations are disputed — subjective multiples, economic conditions, and interest rate environments all compress what buyers will pay

- Buyers don't appear on schedule — health issues, family emergencies, or market downturns can force an earlier exit at a worse valuation

- Deal structures add uncertainty — earnouts and seller financing shift risk back to you even after a deal closes

Many owners respond to this risk with key-man insurance, written buy-sell agreements, and professional business valuations. Those are smart protections — but they safeguard the business, not your personal income in retirement. A SEP-IRA, Solo 401(k), or defined benefit plan funded independently of the company is what actually fills that gap. The business and your retirement savings need to be two separate things, built in parallel.

Mistake #2: Not Knowing — or Underusing — Retirement Plan Options Available to You

Here's something most owners don't realize: you likely have access to more powerful tax-advantaged retirement vehicles than the average employee. Yet SCORE found in 2019 that 34% of entrepreneurs had no retirement savings plan for themselves, and 18% planned to rely on a business sale instead.

These vehicles offer higher contribution limits and meaningful tax advantages — but most owners either default to a basic IRA or do nothing at all.

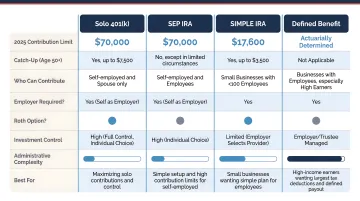

Overview of Retirement Plans for Small Business Owners

| Plan Type | 2025 Contribution Limit | Best For |

|---|---|---|

| Solo 401(k) | Up to $70,000 total; $23,500 employee deferral + employer contributions | Self-employed with no employees |

| SEP IRA | Lesser of 25% of compensation or $70,000 | Sole proprietors, flexible income |

| SIMPLE IRA | $16,500 employee deferral; up to $5,250 catch-up for ages 60–63 | Small businesses with employees |

| Defined Benefit / Cash-Balance Plan | Up to $280,000 annual benefit | High-earning owners, catch-up savings |

The right plan depends on your business structure, number of employees, and income level. A sole proprietor earning $200,000 annually has different optimal strategies than an S-corp owner with three part-time employees.

Two plans in particular, the Solo 401(k) and SEP IRA, allow employer contributions on top of employee deferrals. That means you can reduce taxable business income while dramatically increasing total annual savings. Cash-balance plans go further still, permitting substantially higher annual contributions than standard defined contribution plans — a practical option for owners who started saving late. Barking Sands Capital works with business owners to evaluate whether these plans fit their income level and timeline.

Even owners who have a plan often fail to maximize contributions in strong income years. Missing those contributions means missing compounding growth you can never recover.

Mistake #3: Waiting Until the Business "Stabilizes" to Start Saving

Every business owner has said some version of this: "Once things calm down, I'll focus on retirement." The problem is that things rarely calm down. There's always a next phase, a new hire, a product launch, or an economic headwind. Waiting becomes permanent.

The math on this mistake is severe. Consider two owners, both targeting a 7% annual return:

- Person A contributes $500/month starting at age 35 for 30 years — total invested: $180,000 — ending balance: ~$610,000

- Person B waits until 45, contributes $1,000/month for 20 years — total invested: $240,000 — ending balance: ~$521,000

Person A contributed $60,000 less and ended up with nearly $90,000 more. That's the cost of a decade's delay.

The Irregular Income Problem — and Why It's Not an Excuse

Variable or seasonal revenue is real. It's not a reason to avoid retirement accounts. It's an argument for choosing the right ones.

Both the SEP IRA and Solo 401(k) allow contributions to flex with income. There's no fixed monthly requirement. In a strong year, you contribute heavily. In a lean year, you contribute less. The structure accommodates irregular cash flow.

The compounding math above reinforces two additional realities:

- Small contributions made early grow longer and outperform large contributions made late — as the numbers above show

- Contributions in high-income years deliver the biggest tax deductions, meaning the IRS is essentially subsidizing your retirement savings when your margins are strongest

The right account structure removes the "irregular income" objection. What remains is simply the decision to start.

Mistake #4: Ignoring the Tax Strategy Inside Your Retirement Plan

The structure of your retirement plan determines when — and how much — you pay in taxes. Most small business owners pick a plan based on contribution limits and call it done. That's a costly oversight.

Pre-Tax vs. Roth: Which One Actually Benefits You

The decision between traditional pre-tax contributions and Roth contributions should be driven by one question: will your tax rate in retirement be higher or lower than it is today?

- Pre-tax contributions reduce taxable income now. You pay taxes on withdrawals in retirement.

- Roth contributions are made with after-tax dollars. Qualified withdrawals are tax-free.

For business owners in high-earning years, pre-tax deferrals often make the most sense — the upfront deduction is worth more when your marginal rate is higher. But this isn't universal, and getting it wrong means paying taxes at the wrong time.

The RMD Trap Most Owners Don't See Coming

Owners who spend decades maximizing pre-tax contributions without a withdrawal strategy can face a painful surprise. The IRS requires minimum distributions from traditional IRAs, SEP IRAs, SIMPLE IRAs, and 401(k)s beginning at age 73— and every dollar withdrawn counts as taxable income.

Large pre-tax balances can:

- Push you into a higher federal tax bracket in retirement

- Trigger Medicare IRMAA surcharges — the 2026 thresholds start at individual income above $109,000, with Part B premiums jumping from $202.90 to $284.10 or higher

- Create a chain of compounding tax hits that proper planning could have avoided

The fix isn't avoiding pre-tax accounts. It's to plan withdrawals deliberately — potentially using Roth conversions in lower-income years to reduce future RMD exposure.

Mistake #5: Skipping the Annual Retirement Plan Review

A retirement plan isn't a document you file and forget. Tax laws change. Contribution limits adjust annually. Business structures evolve. And personal circumstances — marriage, divorce, new children, deaths — shift in ways that demand updates.

The Beneficiary Designation Trap

Few things catch people off guard quite like this one. FINRA is explicit on the point: beneficiary designations on retirement accounts legally override instructions in your will. Full stop.

That means if you named an ex-spouse as beneficiary on your IRA ten years ago and never updated it, they may still receive those assets — regardless of what your will says. Any of the following warrant an immediate review of every beneficiary designation across every account and life insurance policy:

- A divorce or remarriage

- A death in the family

- The birth or adoption of a child

Other Elements That Belong in Every Annual Review

- Social Security filing strategy — delaying past 62 permanently increases monthly benefits, but owners with irregular income histories need real analysis to find the optimal filing age.

- HSA and Medicare coordination — the IRS is clear that HSA contributions must stop once Medicare enrollment begins, including retroactive coverage. Missing this creates contribution violations.

- Business debt exposure — if personal assets are pledged as collateral for business loans, a worst-case scenario could reach retirement assets. This connection deserves a hard look every year.

How Working with a Financial Advisor Changes the Outcome

Without an HR department or in-house financial team, small business owners make retirement decisions in isolation. The cost of those decisions — in missed contributions, wrong plan structures, poor tax timing, and unreviewed beneficiary forms — compounds over decades, not just years.

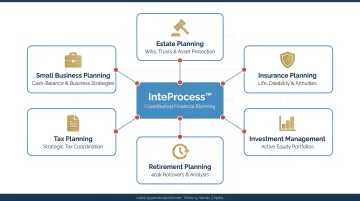

An independent, fee-based advisor coordinates all of these pieces rather than treating each as a separate silo. Barking Sands Capital's proprietary InteProcess™ does exactly this: it brings your CPA, insurance agent, and investment advisor into a single coordinated framework — legal, insurance, tax, retirement, and financial planning working together as one team.

As an independent RIA, Barking Sands Capital is compensated by clients — not through product commissions. That structure matters when evaluating decisions like:

- Plan selection and contribution strategy

- Roth conversions and cash-balance plan timing

- Business succession and ownership transitions

With no commission incentive, the only recommendation is the one that's genuinely optimal for your situation.

The right time to engage isn't when retirement is close. It's during the growth phase of your business, when decisions about structure, compensation, and reinvestment can be made with retirement in mind.

Frequently Asked Questions

What is the most common mistake small business owners make with retirement planning?

Over-relying on a future business sale is the single most prevalent mistake. Only 20% to 30% of businesses listed for sale actually sell, which means owners counting on that outcome are building their retirement on an uncertain foundation. A separate retirement portfolio is essential, regardless of what the business is worth.

What is the best retirement plan for a small business owner?

The right plan depends on business structure, number of employees, and income level. Solo 401(k)s and SEP IRAs are common starting points for self-employed owners, while cash-balance plans suit high-earning owners who need to catch up quickly.

When should a small business owner start saving for retirement?

As early as possible — ideally in the first profitable years of operation. Compounding growth over 30 years consistently outperforms larger contributions made over 20 years, even when the total dollars contributed are higher in the later scenario.

Can I rely on selling my business to fund my retirement?

No. Most businesses don't sell on the owner's expected timeline or at their expected valuation — market conditions, buyer availability, and deal structure all introduce risk. Retirement savings should always be held separately from any planned sale.

How much should a small business owner save for retirement each year?

A common benchmark is saving enough to replace 70–80% of pre-retirement income. A practical ceiling is the IRS contribution maximum for your plan type — for 2025, that's up to $70,000 for Solo 401(k) and SEP IRA participants.

What happens to my retirement plan if my business structure changes?

Moving from a sole proprietorship to an S-corp, or adding employees, may disqualify you from a Solo 401(k) or require you to include employees in a SEP IRA. Any structural change should trigger an immediate review of your plan type with a qualified advisor.