The fiduciary standard exists to close this gap. It legally obligates an advisor to prioritize your goals over their own compensation, and that single structural difference has compounding consequences for retirement security, tax efficiency, estate outcomes, and wealth preservation.

This article explains what a fiduciary wealth manager actually is, why the distinction matters, and the specific practical advantages that make fiduciary guidance critical for anyone pursuing serious long-term financial goals.

Key Takeaways

- A fiduciary wealth manager is legally required to act in your best interest — not just offer "suitable" advice

- Fee-based fiduciary advisors eliminate commission conflicts, so every recommendation is driven by your goals

- Fiduciary guidance covers taxes, estate planning, retirement income, and risk — not just portfolio management

- Behavioral discipline is one of the most underrated advantages: staying invested during volatility is where real long-term wealth is protected

- The value compounds over time: each well-aligned decision builds on the last, and misaligned advice can erode wealth across decades without you noticing

What Is a Fiduciary Wealth Manager?

A fiduciary is legally bound to place your financial interests above their own. In wealth management, this means every recommendation — investment selection, tax strategy, estate planning — must serve your goals, not the advisor's compensation.

The legal source of this obligation matters. The SEC's interpretation of the Investment Advisers Act establishes that Registered Investment Advisors (RIAs) owe clients both a duty of care (advice must be in the client's best interest, with appropriate monitoring) and a duty of loyalty (conflicts must be eliminated or fully disclosed).

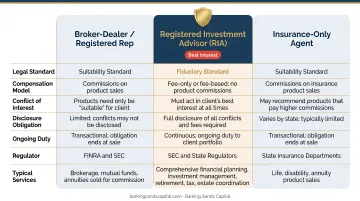

The Fiduciary vs. Suitability Distinction

Not every financial professional is a fiduciary. The two main standards are:

| Standard | Applies To | What It Requires |

|---|---|---|

| Fiduciary Standard | RIAs (Registered Investment Advisors) | Act in the client's best interest across the relationship |

| Suitability Standard | Broker-dealers | Recommend products that are "suitable" — not necessarily optimal |

| Regulation Best Interest | Broker-dealers (updated) | Act in best interest at the time of a recommendation only |

The RIA fiduciary duty governs the entire advisory relationship. Regulation Best Interest, by contrast, attaches only to individual recommendations. A non-fiduciary advisor can legally recommend a higher-cost product that is merely acceptable for your situation, even when a better option exists.

This plays out in concrete ways: a broker steered toward a fund with a 1% higher expense ratio isn't breaking any rules — they're just not operating under the same obligation. Over a 20-year retirement horizon, that difference in fees and alignment can meaningfully erode returns.

Key Advantages of Working with a Fiduciary Wealth Manager

The three advantages below are not abstract. They show up in the real-world quality and consistency of financial decisions made across years and decades.

Conflict-Free Advice That Protects Your Long-Term Wealth

Fee-based RIAs — like Barking Sands Capital — are compensated directly by clients, typically as a percentage of assets under management or a flat fee. They cannot receive commissions for recommending specific products. That structural fact changes everything about the advice you receive.

When an advisor earns nothing extra from recommending one product over another, their only financial incentive is to recommend what actually serves your goals.

The cost of the alternative is well-documented. A 2015 White House Council of Economic Advisers report estimated that conflicted retirement advice reduces investor returns by roughly 1 percentage point per year — costing IRA investors approximately $17 billion annually — and can reduce a 30-year rollover balance by 12%.

Where this matters most:

- Choosing between annuity products with varying surrender charges and mortality fees

- Selecting retirement account allocation strategies with different fee structures

- Purchasing life or disability insurance where commission structures vary significantly

For context on what product costs look like in practice: FINRA reports that mutual fund front-end loads typically range from 2% to 5%, with Class B and C shares often carrying 1% annual 12b-1 fees. ICI data shows the 2024 average expense ratio for actively managed equity funds was 0.64% versus 0.05% for index equity funds. These differences, compounded over decades, are not trivial.

The founding story of Barking Sands Capital illustrates this directly. J.B. and Kelly L'Esperance left larger financial organizations specifically because they observed a culture of pushing products that didn't match their clients' actual needs. Their decision to build a fee-based RIA was a deliberate rejection of that model.

Holistic Planning That Integrates Every Dimension of Your Financial Life

A fiduciary wealth manager's obligation to act in your best interest naturally extends beyond portfolio returns. To truly serve long-term goals, advice must account for taxes, estate structure, risk protection, retirement income, and healthcare costs — not just investment allocation.

This matters more than most clients realize:

- Only 46% of U.S. adults had a will as of 2021, according to Gallup — meaning the majority have no estate plan at all

- The median loss from non-optimized Social Security claiming is estimated at $182,370 in present value lifetime spending, per NBER research

- 36% of retirees report unexpected spending needs since retirement, according to EBRI — and healthcare costs are higher than expected for 35% of retirees

Integrated planning addresses these gaps proactively. An advisor who sees your full financial picture can identify:

- Roth conversion windows that reduce lifetime tax burden

- Asset location strategies that improve after-tax returns by 5–30 basis points (Vanguard research)

- Estate planning gaps that could result in probate delays or unintended asset distribution

- Long-term care exposures that threaten retirement income durability

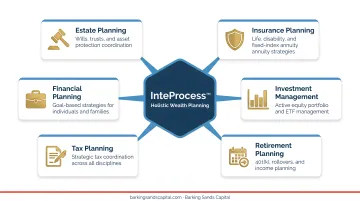

Barking Sands Capital formalizes this integration through their proprietary InteProcess™ — a structured planning methodology that coordinates legal, insurance, tax, retirement, and financial planning under one client-first framework.

Rather than requiring clients to manage multiple disconnected advisors, the process brings designated professionals in each discipline together as a coordinated team. A Roth conversion recommendation, for instance, is evaluated against the client's full tax picture, Medicare planning needs, and long-term care considerations — not in isolation.

That distinction — between investment management and wealth management — is the difference between optimizing a single account and optimizing an entire financial life.

Long-Term Discipline and Protection from Costly Behavioral Mistakes

Market risk gets most of the attention. Investor behavior is often the greater threat.

Panic-selling in downturns, chasing short-term performance, and abandoning diversified strategies during volatility are among the most expensive financial mistakes a person can make. The data is consistent:

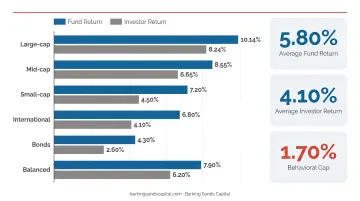

- Morningstar's 2025 Mind the Gap study found the average dollar invested in U.S. mutual funds and ETFs earned 7.0% annually over the 10 years ended December 31, 2024 — versus 8.2% for the funds themselves, a 1.2 percentage point annual gap driven primarily by poor timing decisions

- DALBAR's 2026 QAIB report found the Average Equity Investor earned 17.16% in 2025 versus 17.88% for the S&P 500. In 2024, the gap was far wider: 16.54% for the average equity investor versus 25.02% for the index

- During the COVID-19 collapse in early 2020, Vanguard research found that investors who moved to all cash and stayed out were worse off than those who stayed invested — by May 2020, more than 80% of those who had moved to cash were behind where they would have been had they remained invested

Fiduciary advisors function as a behavioral anchor during these moments. Because their compensation is not tied to transaction volume, they are incentivized to keep clients on a well-constructed plan rather than to encourage changes. They provide objective, evidence-based counsel when emotional reactions are most likely to cause lasting damage.

Vanguard estimates advisor value at up to or exceeding 3% in net returns, with behavioral coaching cited around 150 basis points annually during volatile periods. That's not a guaranteed annual premium — it's episodic value delivered when it matters most.

Barking Sands Capital's documented philosophy during major downturns reflects this directly. During the 2020 COVID market collapse, the firm consistently counseled clients to stay invested and stay the course. By July 2020, the market had fully recovered from its March lows — a recovery that rewarded clients who remained disciplined and penalized those who sold into the panic.

Pre-retirees and retirement-age clients benefit most from this function. They cannot afford to recover from large, emotionally-driven portfolio disruptions the way a 35-year-old investor can.

What Happens When Fiduciary Guidance Is Missing

The costs of working with a non-fiduciary or commission-driven advisor over a long-term horizon rarely appear as a single obvious mistake. They build up across years, often invisible until it's too late to recover them:

- Higher-cost products — variable annuities with mortality and expense charges around 1.25% annually, or mutual fund share classes with 12b-1 fees of 1% per year, selected when lower-cost alternatives were available

- Tax drag — missed tax-loss harvesting opportunities, inefficient asset location, and uncoordinated Roth conversion timing that compound year after year without any visible warning sign

- Estate planning gaps — documents not updated after marriages, divorces, deaths, or business changes — often only discovered during a crisis

- Planning vacuum — without a fiduciary coordinating all aspects of financial life, clients self-navigate the intersection of tax law, investment strategy, estate documents, and retirement income planning, exposing themselves to blind spots no single dimension would reveal

The "higher-cost products" problem above is not hypothetical. The SEC's Share Class Selection Disclosure Initiative documented exactly this failure at scale: in 2019, 79 advisers agreed to return more than $125 million to clients for selecting higher-cost mutual fund share classes when lower-cost alternatives were available — a breach of duty most clients never detected.

Unlike a single bad trade, this kind of erosion leaves no obvious footprint. A fiduciary advisor's role is to close exactly these gaps — coordinating tax strategy, product selection, and estate planning so the compounding works for you, not against you.

How to Get the Most Value from a Fiduciary Wealth Manager

A fiduciary relationship produces better outcomes when the client engages fully:

- Complete disclosure matters — share income, liabilities, business interests, inheritance expectations, and insurance policies. A fiduciary can only build an optimal plan with the full picture.

- Reviews keep the plan current — tax laws shift, life circumstances evolve, and a plan calibrated five years ago may no longer fit. Quarterly or annual check-ins maintain alignment.

- Continuity drives better decisions — an advisor who knows your full history, priorities, and risk tolerance is best positioned to flag opportunities and catch risks before they become problems.

The value of fiduciary advice compounds over time. Each well-aligned decision builds on the last. Across investments, taxes, estate structure, and retirement income, that accumulated alignment is where lasting financial progress is built.

Conclusion

The fiduciary standard is ultimately about alignment. When your advisor is legally required to prioritize your goals, every planning decision across investments, taxes, estate structure, and retirement is oriented toward where you want to go.

That alignment, consistently maintained and regularly reviewed, produces better outcomes over time. It's a direct contrast to well-intentioned but conflicted advice from someone whose compensation depends on what they sell you.

For those seeking a fiduciary partner who integrates all dimensions of financial planning under a transparent, client-first structure, Barking Sands Capital offers that structure as an independent, fee-based RIA. Schedule a consultation to discuss how comprehensive fiduciary planning can be applied to your specific goals.

Frequently Asked Questions

How much does a fiduciary financial planner cost?

Fee-only fiduciary advisors are typically compensated through AUM fees (commonly 0.8%–1.2% annually for portfolios under $1M, declining for larger accounts), flat retainer fees, or hourly rates. Because they do not earn commissions, the stated fee represents the complete cost. There are no hidden product incentives built into the advice.

What is the difference between a fiduciary and a non-fiduciary financial advisor?

A fiduciary is legally required to act in the client's best interest across the entire advisory relationship. A non-fiduciary advisor operating under a suitability standard can recommend products that are acceptable for your situation even when better options exist, which can have measurable consequences over long time horizons.

How do fiduciary wealth managers help with retirement planning?

Fiduciary advisors build retirement strategies aligned with your income needs, tax situation, and timeline. This includes coordinating Social Security timing, withdrawal sequencing, and Roth conversion strategies without the conflict of interest that comes with high-commission retirement products.

Are fee-only fiduciary advisors worth the cost?

Research consistently shows advisor-guided investors achieve better long-term outcomes. Vanguard found that advice materially improved portfolio construction for nearly 90% of investors, and behavioral coaching alone can add up to 150 basis points during periods of volatility. That value typically exceeds the advisory fee.

How do I know if my financial advisor is a fiduciary?

Ask directly and request a written confirmation. You can also verify RIA registration through the SEC's Investment Adviser Public Disclosure (IAPD) database. Advisors who are not registered as RIAs may not be held to fiduciary standards at all times, even if they use similar titles.

Can a fiduciary wealth manager help with estate planning?

Comprehensive fiduciary advisors coordinate estate planning as part of a holistic financial plan — including beneficiary alignment, trust structuring, and tax-efficient wealth transfer. Firms like Barking Sands Capital integrate legal coordination directly into their planning process through the InteProcess™, rather than treating it as an afterthought.