The stakes are real. Without an integrated plan, seniors risk avoidable estate taxes, unintended asset distribution, depleted savings from long-term care costs, and family disputes that could have been prevented by a single updated document. The decisions made — or deferred — in the years surrounding retirement can shape an entire generation's financial future.

This guide covers what seniors 60+ in Minnesota, Michigan, and the broader Midwest need to know: essential estate planning documents, senior-specific tax rules, asset protection strategies, long-term care considerations, and the planning mistakes that silently erode retirement security.

Key Takeaways

- Estate planning goes well beyond a will — it includes trusts, powers of attorney, and healthcare directives that work together

- Seniors face unique tax rules (RMDs, Social Security taxation, IRMAA) that require proactive, coordinated planning

- Long-term care costs represent one of the largest unplanned threats to retirement assets — nursing home care in Minnesota now averages $166,440 per year

- Coordinating legal, tax, and financial planning together — not separately — prevents costly gaps and missed opportunities

- Many legal and financial tools become unavailable once health declines, making early action critical

Why Integrated Planning Matters for Seniors

Tax, estate, and financial planning are deeply interdependent. A Roth conversion decision affects income taxes today and the size of a taxable estate tomorrow. A trust structure affects both estate tax exposure and how retirement accounts should be distributed. Treat them separately and you get contradictory strategies — and missed opportunities.

Here's what that looks like in practice: a senior executes a large Roth conversion to reduce future RMDs, without realizing it pushes their MAGI above the Medicare IRMAA threshold. Their Part B premium jumps from $202.90 to $284.10 per month — a cost that could have been avoided with coordinated planning.

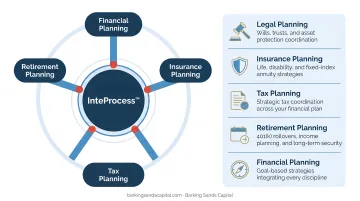

Barking Sands Capital's proprietary InteProcess™ directly addresses this coordination gap. Rather than managing advice from multiple unconnected professionals, clients work with a single coordinated team spanning five disciplines:

- Tax planning — income tax positioning, Roth conversions, RMD timing

- Estate planning — trust structures, beneficiary coordination, asset protection

- Insurance & Medicare — IRMAA thresholds, long-term care coverage

- Retirement distribution — withdrawal sequencing, Social Security optimization

- Investment management — portfolio alignment with income and tax goals

Decisions in one area are always evaluated against the others — so a Roth conversion strategy is assessed alongside Medicare planning and long-term care needs, not in isolation.

Essential Estate Planning Documents Every Senior Needs

The Foundation: Wills

A will directs asset distribution, names an executor, and can name guardians for dependents. Without one, state intestacy laws decide who gets what, and that outcome rarely matches what the deceased actually wanted.

According to Gallup's most recent age-specific data, 24% of Americans 65 and older do not have a will. That's a significant portion of seniors leaving asset distribution to state default rules.

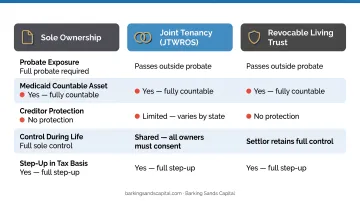

Trusts: When and Why They Matter

A will alone often can't accomplish what a well-structured trust can, especially for seniors with property in multiple states, significant assets, or blended families.

Two core trust types:

- Revocable living trust: maintains control during your lifetime, avoids probate, and allows smooth asset transfer at death without court involvement

- Irrevocable trust: provides stronger asset protection and potential estate tax reduction, but cannot easily be changed once established

Specialized trust types relevant to seniors:

- Special needs trust: protects a disabled dependent's eligibility for government benefits while providing supplemental support

- Testamentary trust: created through a will to manage inheritances for minor or financially inexperienced beneficiaries

- Charitable remainder trust: generates income during lifetime, reduces the taxable estate, and fulfills philanthropic goals

Powers of Attorney and Healthcare Directives

A durable power of attorney (financial POA) authorizes a trusted person to manage financial and legal affairs if you become incapacitated. The word "durable" matters: it means the authority survives incapacity, unlike a standard POA that terminates the moment it's most needed.

Execute this document while you're still legally capable of doing so. Healthcare directives serve two distinct functions:

- A living will specifies medical treatment preferences, including end-of-life care decisions

- A healthcare proxy (medical POA) designates someone to make medical decisions when you cannot

Together, these documents prevent family conflict and court intervention during medical emergencies.

One final piece that often gets missed: beneficiary designations on IRAs, 401(k)s, life insurance policies, and payable-on-death accounts. These designations supersede your will — an outdated designation naming an ex-spouse or a deceased relative can unravel an otherwise carefully drafted estate plan entirely.

Tax Planning Strategies Seniors Should Know

Required Minimum Distributions (RMDs)

Under SECURE 2.0, the RMD starting age is now 73 for most current retirees (rising to 75 for those who turn 73 after 2032). Failing to take RMDs triggers an excise tax of 25% of the shortfall — reduced to 10% if corrected within two years, down from the prior 50% penalty.

Two strategies worth knowing:

- Front-loading withdrawals in lower-income years — drawing down tax-deferred accounts before RMDs are required can reduce future mandatory distributions and keep income in lower brackets

- Qualified Charitable Distributions (QCDs) — seniors 70½ and older can donate directly from an IRA to charity (up to $111,000 in 2026), satisfying RMD requirements without the withdrawal counting as taxable income

Social Security Taxation and IRMAA

Social Security benefits become taxable based on "combined income" (AGI + tax-exempt interest + half of Social Security). Per IRS Publication 915, the thresholds are:

| Filing Status | 50% Taxable | 85% Taxable |

|---|---|---|

| Single | $25,000–$34,000 | Above $34,000 |

| Married Filing Jointly | $32,000–$44,000 | Above $44,000 |

These thresholds are not indexed for inflation — they've remained fixed since 1993. Proactive management of other income sources (Roth conversions, timing of asset sales) can reduce or eliminate taxation on benefits.

IRMAA is the Medicare surcharge applied when income exceeds certain thresholds. For 2026, Part B IRMAA begins at $109,000 MAGI for individuals and $218,000 for married couples. At the highest income tier, the total Part B premium reaches $689.90/month — versus the base rate of $202.90. Strategic income timing can keep seniors below these brackets.

Gifting and Estate Tax Planning

Income management strategies like Roth conversions and IRMAA planning connect directly to longer-term wealth transfer goals. Two numbers anchor that planning for 2026:

- Annual gift tax exclusion: $19,000 per recipient — gifts at or below this amount require no gift tax filing and reduce the taxable estate over time

- Federal estate tax exemption: $15,000,000 per person — established by the One Big Beautiful Bill Act (P.L. 119-21), replacing the prior scheduled TCJA sunset reduction, and indexed for inflation going forward

Estates below the exemption threshold generally owe no federal estate tax, though state-level estate taxes may still apply depending on where you live.

Capital Gains and the Home Sale Exclusion

Long-term capital gains rates depend on taxable income — and some seniors in lower brackets qualify for the 0% rate (applicable through $48,350 for single filers and $96,700 for married joint filers in 2025).

Seniors selling a primary residence may exclude up to $250,000 of gain ($500,000 married filing jointly), provided they've lived in the home as a primary residence for at least 2 of the 5 years before the sale.

Partial exclusions are available if the sale was driven by a change in health, employment, or unforeseen circumstances — worth confirming with an advisor before assuming full eligibility.

Asset Protection and Long-Term Care Planning

The Financial Reality of Long-Term Care

According to CareScout's 2025 Cost of Care Survey, long-term care costs in the Midwest are substantial:

| Care Type | National Median | Minnesota | Michigan |

|---|---|---|---|

| Nursing Home (Private Room) | $129,575/yr | $166,440/yr | $143,628/yr |

| Assisted Living | $74,400/yr | $78,870/yr | $69,816/yr |

| In-Home Care | $80,080/yr | $100,672/yr | $79,508/yr |

A two-to-three-year nursing home stay in Minnesota could easily exceed $400,000. Without a plan, these costs come directly out of retirement assets — often depleting savings intended for a surviving spouse or the next generation.

Long-Term Care Insurance and Hybrid Policies

Long-term care insurance transfers LTC risk away from personal assets. The best time to purchase it is before health issues arise — when premiums are lowest and coverage is easiest to obtain.

Two main policy structures are worth evaluating:

- Standalone LTC policies — dedicated coverage for care costs; premiums may be partially deductible when medical expenses exceed the AGI threshold (deductible limits increase with age)

- Hybrid life/LTC policies — combine a death benefit with long-term care coverage; if care is never needed, the policy still pays out to beneficiaries

Curtis Hewitt, Barking Sands Capital's advisor specializing in Medicare Planning and Long Term Care, works with clients across Michigan and Minnesota to evaluate these options within the context of their broader financial plan — ensuring LTC decisions account for IRMAA implications and retirement income needs.

Medicaid Planning and Asset Protection Trusts

For seniors who cannot afford private LTC insurance, Medicaid may eventually cover long-term care costs — but eligibility rules are strict. Federal law applies a 60-month (5-year) look-back period, during which asset transfers are scrutinized. Both Minnesota and Michigan apply this same 60-month standard.

An irrevocable Medicaid Asset Protection Trust (MAPT) can shield assets from Medicaid spend-down requirements while allowing Medicaid to cover care costs — but only if established well before the look-back window. Most advisors recommend establishing a MAPT at least five to seven years before anticipated care needs.

Strategic ownership structures also matter:

- Joint tenancy with right of survivorship — assets pass directly to the survivor outside probate

- Tenancy by the entirety — protects jointly held spousal assets from individual creditors (available in applicable states)

- Transfer-on-death (TOD) designations — investment accounts pass directly to named beneficiaries without probate

Each of these structures carries different implications for Medicaid eligibility, estate taxes, and creditor protection — making coordination between your financial advisor and estate planning attorney essential.

Retirement Income and Financial Planning Essentials

The Distribution Phase Requires a Different Strategy

Accumulating assets is fundamentally different from distributing them. Retirement requires sequencing withdrawals from taxable, tax-deferred, and tax-free accounts in a way that minimizes lifetime tax burden and sustains the portfolio.

William Bengen's foundational research established the 4% starting withdrawal rate as a historical baseline for a 30-year retirement. Morningstar's 2026 research updates this to 3.9% as the highest safe starting rate under current assumptions — reflecting the impact of lower expected returns and sequence-of-returns risk.

Sequence-of-returns risk is most dangerous early in retirement: a significant market decline in years one through three can permanently impair a portfolio's longevity, even if long-term average returns are solid. A portfolio structured with appropriate allocation between growth assets and near-term income reserves helps manage this risk.

Social Security Timing

For those born in 1960 or later, full retirement age is 67. Delaying benefits past full retirement age increases the monthly benefit by 8% per year, up to age 70 — a total potential increase of 24% for those who wait the full period.

Key timing considerations for couples include:

- Coordinating spousal benefits with delayed credits can significantly increase lifetime household income

- Larger Social Security benefits may push more of those benefits into the taxable range

- The claiming decision interacts directly with income tax planning — timing matters beyond just the monthly check

Investment Management in Retirement

Seniors need portfolios that balance two competing needs: growth sufficient to combat longevity risk and inflation, and preservation sufficient to cover near-term income without being forced to sell at a loss. Navigating that tension is harder without advice that's genuinely free of product incentives.

Barking Sands Capital operates as a fee-based independent RIA — advisors aren't paid commissions on managed accounts, which keeps recommendations on portfolio structure and income products genuinely unbiased. The firm's active management approach allows for tactical positioning during market volatility, directly addressing sequence-of-returns risk in the early years of retirement.

Common Mistakes Seniors Make in Estate and Financial Planning

Estate Planning Mistakes

- Not updating documents after major life events — divorce, a beneficiary's death, new grandchildren, or significant asset changes all require document review

- Misaligned beneficiary designations — naming an estate rather than an individual on a retirement account forces it through probate and may trigger accelerated distributions; naming a minor directly without a trust creates its own complications

- Waiting too long for a durable POA — once someone lacks legal capacity, a durable POA cannot be executed; the only alternative is a court-supervised guardianship proceeding

Tax and Financial Planning Mistakes

- Missing RMD deadlines — the 25% excise tax is avoidable with basic planning; there's no good reason to miss an RMD

- Ignoring IRMAA when executing large asset transactions — a Roth conversion or capital gain event that pushes income above an IRMAA threshold can cost thousands in additional Medicare premiums

- Treating the home as a tax-free estate planning tool — heirs who inherit appreciated property receive a step-up in basis to fair market value at death (largely tax-free); heirs who receive it as a lifetime gift inherit the donor's original cost basis instead, creating a potentially large taxable gain

- Delaying LTC planning until health issues arise — by that point, coverage may be unavailable or unaffordable

The Biggest Mistake: Siloed Planning

The most consequential mistake is treating tax, estate, and financial planning as three separate conversations with three professionals who never coordinate. Contradictory strategies across these disciplines silently erode retirement plans, often until it's too late to correct.

Working with a team that takes an integrated approach — one that views investment management, retirement analysis, tax planning, and estate coordination as interconnected — is the most effective way to avoid these gaps.

Frequently Asked Questions

What are the important tax rules for seniors that affect estate and financial planning?

The key rules include RMDs from tax-deferred accounts starting at age 73, Social Security taxation beginning at $25,000 combined income for single filers, the $19,000 annual gift tax exclusion for estate reduction, and the $15,000,000 federal estate tax exemption for 2026. These rules interact directly: RMD income can trigger Social Security taxation and IRMAA surcharges at the same time, so coordinated planning across all three is essential.

How can I protect an elderly parent's assets through estate and financial planning?

The four primary tools are a durable power of attorney, irrevocable trusts to shield assets from Medicaid spend-down, long-term care insurance to cover care costs without depleting savings, and updated beneficiary designations to keep assets out of probate.

What is the 5-by-5 rule in estate planning?

The 5-by-5 rule is a trust provision allowing a beneficiary to withdraw the greater of $5,000 or 5% of the trust's value per year without triggering gift tax consequences. It's commonly used in irrevocable trusts to give beneficiaries limited access to funds while preserving the trust's asset protection and tax benefits.

What are common estate and financial planning mistakes to avoid for the elderly?

The most consequential mistakes are failing to update beneficiary designations after life changes, not establishing a durable POA before incapacity makes it impossible, delaying long-term care planning until health conditions prevent coverage, and missing RMD deadlines. All of these compound when tax, estate, and investment decisions aren't coordinated together.

When should seniors start estate and financial planning?

The best time is while the individual is healthy and mentally capable — ideally well before retirement. Many legal documents (like a durable POA) cannot be executed once someone is incapacitated, and many tax strategies (like Roth conversions or LTC insurance purchase) become less effective or completely unavailable as health declines.

Do seniors need both a will and a trust?

Most seniors benefit from both. A will handles assets outside a trust and names an executor, while a revocable living trust avoids probate and allows more nuanced distribution. Whether both are needed depends on asset complexity, family structure, and state law.