Introduction

You have a tax preparer who sees you once a year in April. An estate attorney who drafted your will five years ago and hasn't called since. A financial advisor managing your investments without any real visibility into your tax picture. Each professional is competent in isolation—but none of them are talking to each other.

This is the "financial silo" problem, and it costs people more than they realize. Not just in taxes paid unnecessarily, but in estate plans that never get implemented, beneficiary designations that contradict legal documents, and investment decisions that trigger surprises at filing time.

Integrated tax and estate planning is the coordinated alternative. It brings financial decisions, tax strategy, and estate considerations into a single, unified review—so changes in one area don't blindside the others. This article covers what that looks like in practice and how to find an advisor built for that kind of coordination.

Key Takeaways

- Fragmented financial advice creates gaps that often surface only during major life events—retirement, inheritance, or death

- Integrated planning reduces lifetime taxes, not just this year's tax bill

- Estate plans most often fail due to poor implementation and outdated beneficiary designations, not flawed documents

- Fiduciary, fee-based advisors are legally required to act in your interest; commission-based advisors face no such obligation

- The best time to integrate your planning is before a major transition, not after

The Problem with Fragmented Financial Advice

Here's a scenario that plays out regularly: a financial advisor recommends a large portfolio rebalance in October. It's a sound investment decision—but it triggers $40,000 in capital gains. The tax advisor doesn't find out until February when the 1099s arrive. By then, there's nothing left to do.

That's the "left hand, right hand" problem in a single example.

When Estate Plans Contradict Themselves

Beneficiary designations on IRAs and 401(k)s override whatever a will says, period. This creates real problems when designations haven't been updated after a divorce, remarriage, or the death of a named beneficiary. A well-known case cited by the Financial Planning Association illustrates this directly: an ex-spouse received $402,000 from an ERISA retirement plan because the beneficiary designation controlled—despite other divorce-related documents suggesting otherwise.

According to Gallup, only 46% of U.S. adults have a will, and AARP recommends reviewing estate plans every five years even without major life changes. Most people don't.

The Tax Opportunity Cost

Several strategies only deliver results when tax and investment decisions are coordinated in advance:

- Roth conversions timed to low-income years

- Tax-loss harvesting executed before year-end

- Charitable giving vehicles structured for maximum deductibility

- Asset location optimized across taxable and tax-deferred accounts

Vanguard's Advisor's Alpha research estimates that coordinated practices—including asset location and withdrawal sequencing—can add up to 3% or more in net returns annually. Over a 20-year retirement, that's the difference between running out of money and leaving something behind.

The deeper problem is that fragmentation persists quietly. Different professionals rarely flag conflicts they can't see. Those gaps tend to surface during a business sale, an inheritance, or a spouse's death—exactly when the cost of fixing them is highest.

Key Components of an Integrated Plan

Tax Planning vs. Tax Preparation

Tax preparation is reactive: you file what already happened. Tax planning is proactive: you model future scenarios, time income and deductions, manage capital gains, and optimize Roth conversions before year-end.

The difference matters. A 2025 CFP Board survey found 95% of CFP professionals consider tax implications when making planning recommendations—and nearly 9 in 10 collaborate with tax experts at least once a year. Proactive tax planning isn't a niche service. It's a baseline expectation of comprehensive advice.

Year-round planning looks like this:

- Monitoring income levels to manage tax bracket exposure

- Timing Roth conversions during low-income years

- Harvesting investment losses to offset gains

- Structuring charitable giving to maximize deduction eligibility

- Reviewing withholding and estimated payments to avoid surprises

Estate Planning and Implementation

Drafting estate documents is only the first step. Documents that sit in a drawer—trusts that were never funded, accounts titled in the wrong name, beneficiary designations that were never updated—accomplish nothing.

Integrated planning closes that gap. An advisor working within a coordinated framework doesn't just know your estate documents exist — they help ensure the account structure reflects what those documents intend. That means verifying that retirement accounts, brokerage accounts, and insurance policies are aligned with the estate plan rather than working against it.

Investment Strategy and Asset Location

Where you hold an asset matters as much as which asset you hold. Placing tax-inefficient investments (like bonds or REITs) in tax-advantaged accounts, and keeping tax-efficient assets (like index funds) in taxable accounts, can meaningfully reduce the drag of annual taxation. Vanguard estimates asset location alone can add 0 to 60 basis points in after-tax value—modest in isolation, but compounding over decades.

Beyond location, how distributions are structured in retirement—which accounts you draw from first, how you manage RMDs, how you sequence withdrawals to control taxable income—are decisions that should be made with full visibility into the tax picture.

Insurance, Risk Management, and Retirement Income

Integrated planning assesses actual risk exposure rather than recommending products in isolation. Life insurance, disability coverage, and long-term care planning should reflect your full financial picture, not a sales quota.

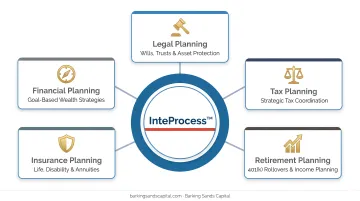

That coordination is the foundation of Barking Sands Capital's proprietary InteProcess™. The framework brings legal, insurance, tax, retirement, and financial planning together under one team-based process, so decisions in each area support the others rather than conflicting. In practice, that means:

- The team evaluates insurance coverage alongside estate transfer goals

- Retirement income planning accounts for Social Security timing and RMD management

- Withdrawal sequencing is structured to control taxable income — not just optimize portfolio performance

The Real Benefits of Integration

When your tax, estate, and investment planning work together, the results go beyond saving money on a single return. Here's what coordinated planning actually delivers:

- Lower lifetime taxes — Roth conversion ladders, bracket management in retirement, strategic charitable giving — these strategies only work with a coordinated view across tax, investment, and income planning.

- Estate goals that get executed — Documents are only as useful as their implementation. Coordinated planning ensures your intentions are reflected in account titling and beneficiary designations, not just in a trust document.

- Fewer expensive surprises — When advisors share the same financial picture, problems surface before they become costly. A capital gains miscommunication doesn't happen if the investment decision and the tax strategy happen in the same conversation.

- Better decisions at life transitions — Selling a business, receiving an inheritance, retiring, losing a spouse — these events demand simultaneous action across tax, legal, and financial dimensions. Integration means you're not scrambling to assemble a team after the fact.

The anxiety angle is worth taking seriously. The FINRA Foundation's 2024 National Financial Capability Study found 63% of U.S. adults say thinking about personal finances makes them anxious, and 53% say discussing finances is stressful. Yet a 2024 Schwab Modern Wealth Survey found only 36% of Americans have a written financial plan — but among those who do, three in four say it makes them feel more in control. A plan that connects all the pieces gives you something to stand on.

Who Benefits Most from This Approach?

Individuals Approaching or in Retirement

This group faces decisions that interact in ways that catch people off guard:

This group faces decisions that interact in ways that catch people off guard:

- Social Security timing affects taxable income

- Roth conversions affect Medicare premium surcharges

- RMDs can push bracket thresholds

- Estate transfer strategies depend on account structure

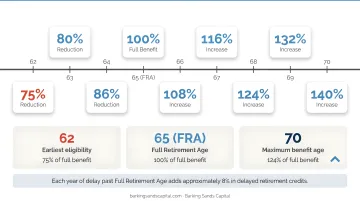

Claiming Social Security at 62 versus waiting until 70 isn't just an income decision—it's a tax and estate decision. For those born in 1960 or later, claiming at 62 means receiving only 70% of the full retirement benefit, while delaying past full retirement age earns 8% per year in delayed credits up to age 70. An integrated advisor models the after-tax, after-healthcare-cost breakeven—not just the nominal benefit comparison.

Small Business Owners

Business owners face the most complex intersection of planning needs: succession, retirement plan selection, personal tax strategy, estate transfer, and insurance. Each piece affects the others, and most require coordination across disciplines at the same time.

Gallup found only 52.3% of employer-business owners have a succession plan. EBRI reported that 72% of small business owners not offering a retirement plan were unaware of tax credits up to $5,000 for starting one. The data points to a coordination problem, not a knowledge problem.

Barking Sands Capital specifically serves small business owners navigating these decisions, including cash-balance plans that allow significantly higher contributions than traditional 401(k)s while reducing current taxable income.

Anyone Whose Financial Life Feels Like It's Running Them

Multiple income streams, real estate holdings, stock compensation, a pending retirement, or significant life transitions ahead—these create complexity that uncoordinated advice handles poorly. Integrated planning isn't about asset size. It's about getting all the pieces to work together.

What to Look for in an Integrated Planning Partner

Credentials and Scope

Look for advisors holding designations like CFP® or ChFC — both require demonstrated competency across comprehensive planning, not just investment management. Ask how tax and estate considerations are incorporated into ongoing planning conversations, not just at onboarding.

Fee-Based and Fiduciary Structure

The fee model matters. As an independent RIA, Barking Sands Capital cannot be paid commissions on managed accounts — a structural distinction that removes product incentives from the equation. Fiduciary advisors are legally required to act in the client's best interest. Commission-based advisors operate under a lower suitability standard, meaning recommendations need only be appropriate — not necessarily optimal.

Cerulli reports that more than 72% of financial advisors are now compensated through fee-based models, and that figure is projected to reach 77.6% by 2026. Fee-based doesn't automatically mean fiduciary. Ask directly before assuming it does.

Questions Worth Asking Any Prospective Advisor

Understanding credentials and fee structure gives you a framework — but how an advisor actually works is revealed in conversation. Before engaging any advisory team, ask:

- How do you coordinate with my tax professional or estate attorney? Vague answers — or no established process — signal siloed planning.

- How often are my beneficiary designations and estate documents reviewed? The answer should be tied to life events and annual reviews, not left to you to initiate.

- How are tax implications factored into investment decisions? If the answer describes a year-end review rather than year-round coordination, the planning is fragmented regardless of what it's called.

Frequently Asked Questions

How do integrated tax, estate, and investment planning services work?

Integrated services bring tax strategy, estate planning, and investment management into a single coordinated framework. Advisors make decisions with visibility into the full financial picture—so an investment move, a charitable gift, or a Roth conversion is evaluated for its tax and estate implications before it happens, not after.

What are the benefits of integrated tax, estate, and investment planning services?

The core benefits are reduced lifetime taxes, estate plans that are properly implemented rather than just drafted, fewer costly financial surprises, and a more coherent financial life managed by professionals who communicate with each other.

Is $500,000 enough to work with a financial advisor?

Many independent, fee-based advisors work with clients at various asset levels. The value of integrated planning comes from coordination and strategy—particularly tax management and estate alignment—not from portfolio size alone. At Barking Sands Capital, the right fit depends on complexity, goals, and life stage.

What is the difference between tax planning and tax preparation?

Tax preparation is filing what already happened. Tax planning is modeling what's about to happen—timing income, structuring deductions, optimizing conversions, and managing gains before year-end while there's still time to act. The difference is the ability to act before the outcome is fixed.

When is the right time to start integrated estate and tax planning?

Before a major life event—retirement, a business sale, an inheritance—when coordinated decisions can still be made proactively. After the fact, options narrow considerably.