: Complete Guide](https://file-host.link/website/barkingsandscapital-x5eet4/assets/refined-images/1784097186094000_ad2894ccdc3c488889aea76f0fc459a7/360.webp)

Here's the problem most families run into: the estate tax and gift tax aren't separate systems. They're interconnected through a single lifetime exemption, and failing to understand that connection — or acting on it too late — can quietly shrink the wealth your heirs actually receive.

This guide covers how both taxes work, how they connect through the unified credit, the most effective planning strategies (from annual gifting to advanced trusts), valuation rules, state-specific considerations for Minnesota and Michigan residents, and when to start taking action.

Key Takeaways

- Estate and gift taxes share one unified lifetime exemption — currently $15 million per person in 2026

- Annual gifts of up to $19,000 per recipient are excluded from that lifetime limit entirely

- Direct payments to educational institutions or medical providers are fully exempt — no annual limit, no lifetime impact

- Trusts (ILITs, SLATs, GRATs, IDGTs) are core vehicles for transferring wealth outside your taxable estate

- Minnesota imposes its own estate tax starting at $3 million, far below the federal threshold. State-level planning is essential for MN residents.

Estate Tax and Gift Tax Basics: What You Need to Know

The Federal Estate Tax

The federal estate tax applies to the transfer of a deceased person's assets when the total estate exceeds the applicable exclusion amount. For 2026, the IRS confirms the OBBBA raised that exemption to $15 million per individual — $30 million for married couples using both exemptions. Amounts above the threshold are taxed at rates up to 40%.

Unlike prior law, this exemption is now permanent and indexed for inflation after 2026 — a meaningful shift for long-term planning.

The Federal Gift Tax

The gift tax applies to transfers of assets during your lifetime when value exceeds the annual exclusion. In 2026, that exclusion is $19,000 per recipient. Married couples can combine their exclusions for $38,000 per recipient through gift-splitting, reported on Form 709.

Gifts within the annual limit require no filing and don't touch your lifetime exemption.

The Generation-Skipping Transfer (GST) Tax

Beyond the estate and gift tax, a third layer applies when wealth skips a generation. The GST tax applies when assets pass directly to grandchildren or beneficiaries at least 37.5 years younger than the donor. The 2026 GST exemption matches the estate tax exemption at $15 million, and fully taxable transfers face the same 40% rate. The tax closes a potential loophole — without it, families could avoid one round of estate tax by bypassing their children entirely.

Estate Tax vs. Inheritance Tax

These are different taxes, paid by different parties:

| Tax | Who Pays | Level |

|---|---|---|

| Estate Tax | The estate (before distribution) | Federal + some states |

| Inheritance Tax | The recipient | State only |

States with inheritance taxes include Kentucky, Maryland, Nebraska, New Jersey, and Pennsylvania. Minnesota has an estate tax but no inheritance tax. Michigan has neither — its inheritance tax applies only to estates from decedents who died on or before September 30, 1993.

Fair Market Value (FMV) Rules

The IRS values gifted and inherited assets at fair market value (FMV) — what a willing buyer would pay a willing seller, with neither under pressure and both having reasonable knowledge of the facts.

For non-cash assets, professional appraisals are typically required. Common examples include:

- Closely held business interests

- Real estate (commercial or residential)

- Fine art, collectibles, and jewelry

- Private equity or restricted stock positions

How Estate Tax and Gift Tax Work Together: The Unified Credit

The Shared Lifetime Exemption

The estate and gift taxes share one lifetime exemption through the "unified credit." Any taxable gift made above the annual exclusion reduces the exemption available at death, dollar-for-dollar.

Simple example: if you use $3 million of your exemption for lifetime gifts, only $12 million remains to shelter your estate.

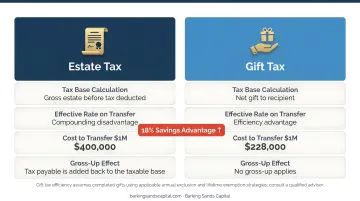

Why Gifting Now Can Save More Than Waiting

The estate tax is tax-inclusive — it applies to the full estate value, including the funds used to pay the tax itself. The gift tax is tax-exclusive — it's calculated only on the amount transferred.

At a 40% rate, $100 retained until death leaves heirs $60 after estate tax. A $71.43 lifetime gift triggers $28.57 in gift tax but delivers the full $71.43 to heirs — an 18% efficiency gain for the same net transfer. The Tax Adviser's post-OBBBA analysis walks through the math in detail.

The tax-exclusive benefit compounds when you factor in appreciation. Gift a $5 million asset today that grows to $8 million by the time you die, and that $3 million in growth occurs entirely outside your taxable estate. At 40%, that's $1.2 million in avoided estate tax on appreciation alone.

The Step-Up in Basis Trade-Off

This tax-exclusive advantage has a counterbalance. Assets passed at death receive a step-up in cost basis to fair market value on the date of death, which eliminates capital gains taxes for heirs who sell. Gifted assets carry the donor's original cost basis — which can create a capital gains problem for the recipient.

Practical rule of thumb:

- Highly appreciated assets (long-held real estate, appreciated stock) → generally better to hold and transfer at death for the step-up

- Cash, low-appreciation assets, or assets expected to grow rapidly → generally better for lifetime gifting to capture the tax-exclusive benefit

Portability for Married Couples

When one spouse dies, any unused portion of their lifetime exemption can be transferred to the surviving spouse — effectively doubling the available exemption. But this requires filing a federal estate tax return (Form 706) to elect portability, even if no estate tax is owed. Form 706 is due nine months after death, with a six-month extension available.

Many families miss this. Rev. Proc. 2022-32 does provide a simplified method to elect portability up to five years after death for estates not otherwise required to file — but acting proactively is far simpler than correcting the oversight later.

Essential Estate and Gift Tax Planning Strategies

Annual Exclusion Gifting

Consistently gifting up to $19,000 per recipient per year is one of the simplest ways to steadily reduce a taxable estate. The math compounds quickly.

A married couple with three adult children and six grandchildren — nine recipients total — can transfer $342,000 per year ($38,000 per recipient × 9) without touching their lifetime exemption. Over 10 years, that's $3.42 million removed from the estate, plus all the growth on those assets that occurs in the recipients' hands.

Direct Payments for Education and Medical Expenses

Under IRC Section 2503(e), unlimited payments made directly to an educational institution or medical provider are fully exempt from gift tax. They don't count against the annual exclusion or the lifetime exemption.

The key requirement: payment must go directly to the institution or provider, not to the individual. Paying a grandchild's $80,000 annual college tuition directly to the university costs you nothing from a gift tax perspective.

Charitable Giving Strategies

Charitable gifts reduce the taxable estate through a full estate tax deduction. Beyond direct giving, two trust-based tools offer flexibility:

- Charitable Remainder Trusts (CRTs): Donor transfers assets, receives income during life, and the charity receives the remainder

- Charitable Lead Trusts (CLTs): Charity receives income for a set term; heirs receive the remainder

For IRA owners age 70½ or older, Qualified Charitable Distributions (QCDs) allow direct transfers to charity — up to $111,000 in 2026 — without the amount appearing as taxable income.

Using the Lifetime Exemption Strategically

Charitable tools help reduce the taxable estate, but for families with significant appreciating assets, the lifetime exemption is where the real leverage lives.

Transferring appreciating assets out of the estate early is the highest-leverage use of the lifetime exemption. Every dollar of future appreciation that occurs in the recipient's hands — rather than the donor's estate — escapes estate taxation entirely.

Families and business owners with growing assets have a real incentive to act while the current ~$13.99 million individual exemption is in place. Congress can change exemption levels — and has before — so acting sooner rather than later protects against future legislative shifts.

Family Limited Partnerships (FLPs)

FLPs allow families to pool assets and create different ownership classes. Interests can then be transferred at valuation discounts for lack of control or marketability — discounts that enable more wealth to move out of the estate than the face value of the transferred interest alone would suggest.

FLPs require careful legal structuring. The IRS scrutinizes them closely under IRC Section 2036, particularly whether a legitimate, non-tax business purpose exists. Blanket discount percentages without qualified appraisal support won't survive scrutiny.

Advanced Trust Strategies for Larger Estates

Irrevocable Life Insurance Trusts (ILITs)

Life insurance death benefits are included in the taxable estate if the decedent owned the policy or held incidents of ownership. Placing the policy inside an ILIT removes the death benefit from the estate entirely, provided the grantor holds no incidents of ownership and the policy wasn't transferred within three years of death.

Premium payments are funded through annual exclusion gifts to the trust. The grantor also pays income taxes on trust earnings, which further reduces the estate without triggering a gift — an often-overlooked efficiency.

SLATs and GRATs

Spousal Lifetime Access Trusts (SLATs): One spouse creates an irrevocable trust for the other's benefit, removing assets from the taxable estate while preserving the beneficiary spouse's access to income and principal.

Two risks deserve attention. If the beneficiary spouse dies or the couple divorces, that access disappears. Reciprocal SLATs (where each spouse creates one for the other) can also be "uncrossed" by the IRS under the reciprocal trust doctrine established in United States v. Estate of Grace.

Grantor Retained Annuity Trusts (GRATs): The donor transfers assets into the trust and receives an annuity for a fixed term. If the assets grow faster than the IRS Section 7520 hurdle rate (currently 5.0% for June 2026), the excess passes to beneficiaries free of estate and gift tax. GRATs work particularly well for publicly traded stock or assets with strong near-term appreciation potential.

Intentionally Defective Grantor Trusts (IDGTs)

An IDGT is "defective" on purpose. Selling appreciating assets to the trust in exchange for a promissory note is a non-taxable transaction for income tax purposes, because the grantor and the grantor trust are treated as the same entity under Rev. Rul. 85-13.

Future appreciation on those assets passes to beneficiaries outside the estate. The grantor's payment of income taxes on trust earnings also functions as an additional tax-free gift to beneficiaries under Rev. Rul. 2004-64.

Valuation, Filing Requirements, and State Estate Taxes

Filing Requirements

- Form 709 (Gift Tax Return): Required for any gift exceeding the $19,000 annual exclusion per recipient, gifts of future interests, or gift-splitting elections. Due April 15 of the year following the gift. Filing doesn't automatically mean tax is owed — the unified credit may offset it entirely.

- Form 706 (Estate Tax Return): Required when a decedent's gross estate exceeds $15 million in 2026. Due nine months after death, with a six-month extension available via Form 4768.

Both forms are separate from income tax returns with their own deadlines — and both depend on accurate asset valuation to be filed correctly.

Valuation of Non-Cash Assets

The IRS requires fair market value (FMV) at the time of the gift or date of death. For complex assets, defensible appraisals by qualified professionals are essential — weak valuations invite IRS disputes, penalties, and underpayment assessments.

Common asset types requiring formal appraisal include:

- Closely held business interests

- Real estate (especially commercial or income-producing property)

- Intellectual property and royalty interests

- Art, collectibles, and other non-liquid assets

One planning option: the alternate valuation date under IRC Section 2032 allows estates to value assets six months after death if doing so reduces both the gross estate value and the estate tax owed. The election applies to all estate assets, not selected ones.

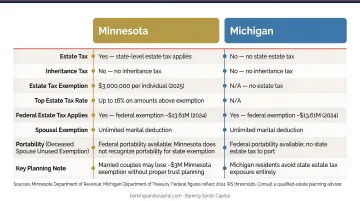

Minnesota vs. Michigan: A Critical Distinction

For Barking Sands Capital's clients across both states, this difference matters:

| Minnesota | Michigan | |

|---|---|---|

| Estate Tax | Yes — filing threshold: $3 million | No |

| Estate Tax Rates | 13% to 16% | N/A |

| Inheritance Tax | No | No (applies only to deaths before Oct. 1, 1993) |

| Gift Tax | Repealed (gifts within 3 years of death may be added back) | N/A |

Minnesota's $3 million estate tax threshold means many families who face no federal estate tax exposure still owe Minnesota estate tax. This creates a strong additional incentive for lifetime gifting among Minnesota residents — particularly since Minnesota repealed its own gift tax, making lifetime transfers more tax-efficient than waiting until death.

When and How to Start Your Estate and Gift Tax Plan

The best time to start is well before your estate approaches any threshold. Early gifting removes future appreciation from the taxable estate — and that compounding effect is substantial over a decade or more. Waiting until the estate is large enough to "need" planning means losing years of tax-free growth in recipients' hands.

Building Your Plan: Key Steps

- Inventory all assets — real estate, investments, retirement accounts, business interests, life insurance, and personal property

- Project estate growth — estimate how assets are likely to appreciate over 10–20 years

- Define legacy goals — identify beneficiaries, charitable intentions, and family priorities

- Select appropriate tools — annual gifting, direct payments, trusts, charitable vehicles, or a combination

- Coordinate professionals — tax advisors, estate attorneys, and financial planners need to work from the same plan

Integration Is the Key Variable

Estate and gift tax planning doesn't live in isolation. Decisions about retirement distributions, investment structure, insurance coverage, and business succession all affect the taxable estate — and each affects the others.

Barking Sands Capital's proprietary InteProcess™ connects these disciplines directly. CFP® and ChFC credentialed advisors coordinate estate planning alongside tax strategy, retirement planning, insurance, and investment management — all within one cohesive approach.

For small business owners, families with growing assets, and clients navigating both federal and Minnesota or Michigan state-level considerations, that coordination means fewer gaps, fewer surprises, and a plan that holds up as circumstances change.

Frequently Asked Questions

How do the gift tax and estate tax work together?

Both taxes share a unified lifetime exemption — currently $15 million per individual in 2026. Any gift above the $19,000 annual exclusion reduces your remaining estate tax exemption dollar-for-dollar. Miss that linkage and a gifting strategy that looks tax-free today can quietly erode the exemption you're counting on at death.

What is the 5 by 5 rule in estate planning?

The 5 by 5 rule is a trust provision allowing a beneficiary to withdraw the greater of $5,000 or 5% of trust assets each year without adverse gift or estate tax consequences. It's commonly included in irrevocable trusts to preserve some beneficiary access while maintaining favorable tax treatment.

How much of your estate can you gift tax free?

You can give up to $19,000 per recipient per year without any gift tax or lifetime exemption impact, plus a $15 million lifetime exemption per person. Direct payments made to educational institutions or medical providers are also fully exempt — no dollar cap applies to those.

What assets are subject to estate tax?

The gross estate includes virtually everything owned or controlled at death — real estate, investment accounts, retirement accounts, life insurance (if the decedent owned the policy), and business interests. Deductions like the unlimited marital deduction and charitable deduction reduce the taxable amount.

What is the difference between an estate tax and an inheritance tax?

The estate tax is paid by the estate itself before assets are distributed — it's a federal tax that also applies in over a dozen states. Inheritance tax is paid by the recipient based on what they receive and exists only at the state level in a handful of states, including Kentucky, Maryland, Nebraska, New Jersey, and Pennsylvania.

When should I start estate and gift tax planning?

Start before you think you need to. Early action removes future appreciation from the taxable estate, preserves planning flexibility, and hedges against future law changes. Every year of delay is a year of compounding that could have passed to heirs tax-free instead.